.png?downsize=773:435 "Jefferies Maintains 'Buy' On Bharat Electronics, Cites Robust Orderbook")

Jefferies has maintained a 'buy' rating on Bharat Electronics Ltd., citing growth in order flows and a promising outlook. The brokerage maintains a target price of Rs 325 per share, valuing the company at 35x PE FY27E and a premium to the 10-year average of 20x, as earnings visibility is good.

BEL announced a Rs 5.8-billion order flow and needs another Rs 113 billion in March-April 2025 to meet its fiscal 2025E guidance of Rs 250 billion.

Management in its Q3 call reiterated meeting its fiscal 2025 guidance which, combined with global news on rising defence spend, may be a near-term trigger for BEL. Government defence spend rose 87% year-on-year in January 2025.

BEL management in its Q3 fiscal 2025 commentary was confident of achieving fiscal 2025 guidance despite achieving only 39% in 9MFY25. It has a track record of delivering on its plans, the brokerage said.

BEL has met or beaten its result expectations, but subdued ordering has weighed on the stock, apart from sector de-rating. "We believe order announcements in March-April are a key near term trigger. Medium-term story of indigenisation remains in place," Jefferies noted.

Global defence stocks have surged as European leaders commit to significant increases in defence spending, a move prompted by US President Donald Trump's decision to suspend military aid to Ukraine.

According to the brokerage, India has been subdued between fears of higher defence imports from US and also lower defence spend year-to-date by the government- down 4% year-on-year versus planned rise of 3% year-on-year. "BEL is relatively insulated from higher imports in the nature of aircraft versus Hindustan Aeronautics, which has more potential impact," it added.

BEL is currently attractively priced within Indian industrial majors and is a niche area with high medium-term visibility on growth prospects in the investment cycle. As orders and earnings come through, the stock should move higher, the brokerage noted.

As per Jefferies, the downside risks include slowdown in defence indigenisation push and unsustainable cost control.

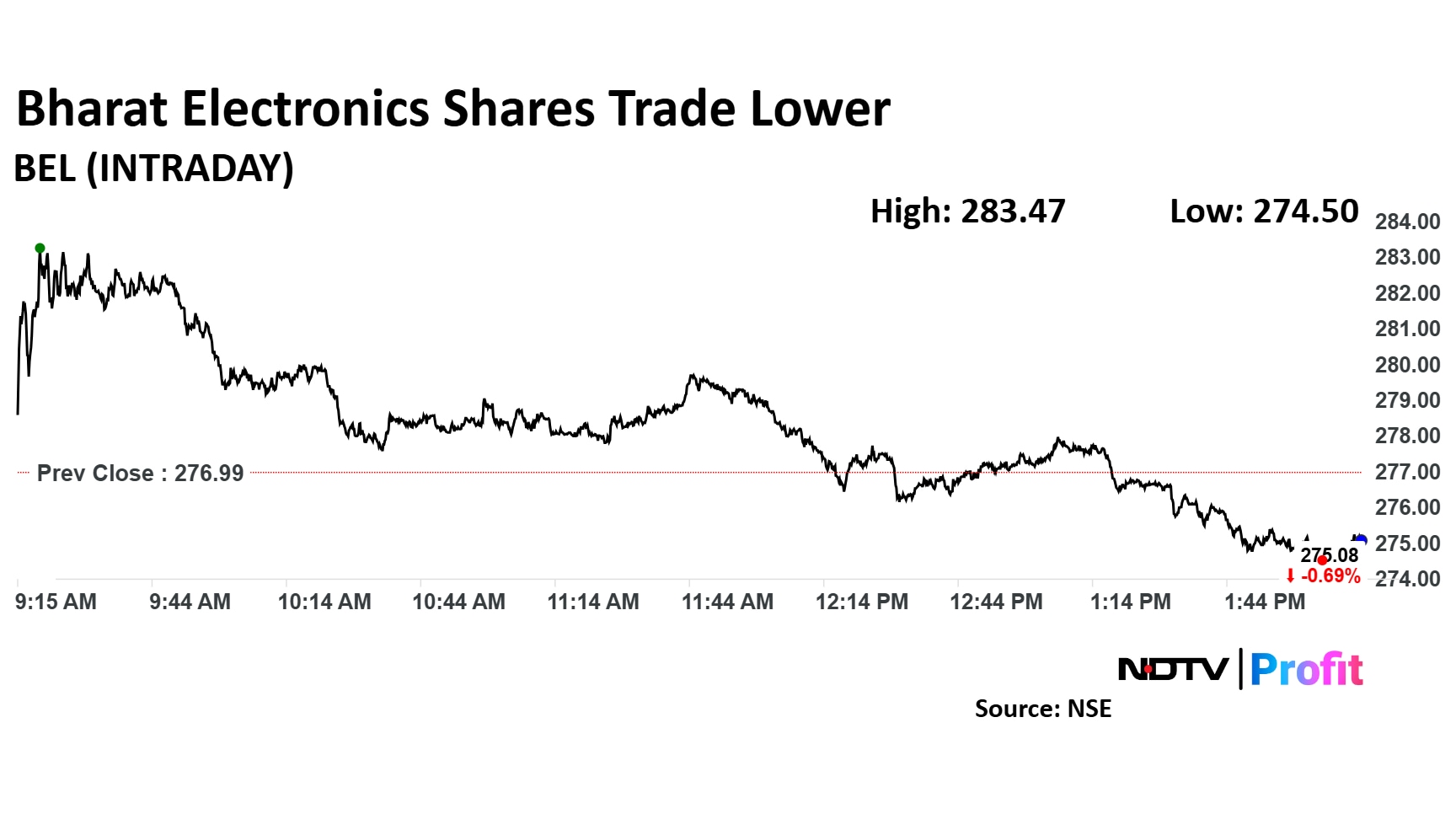

Shares of BEL rose as much as 2.34% to Rs 283.47 apiece. They pared gains to trade 0.68% lower at Rs 275.12 apiece, as of 2:15 p.m. This compares to a 0.01% decline in the NSE Nifty 50.

The stock has risen 27.66% in the last 12 months. The relative strength index was at 62.22.

Out of the 26 analysts tracking the company, 23 have a 'buy' rating on the stock, one recommends a 'hold,' and two suggest 'sell,' according to Bloomberg data. The average of 12-month analysts' price targets implies a potential upside of 24.2%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.