STT, a hiked LTCG and a sliding rupee have turned the world's most-watched emerging market into one of the least attractive markets for foreign investors. The effect is now coming through in record FII outflows. Since April 2024, FIIs have pulled out Rs 4,23,633 crore from Indian markets.

Foreign investors are re-evaluating India

Post-Covid, India was an easy trade. A demographic story, a digital story, a manufacturing story - pick your narrative and there were multiple stocks to watch. That window has been closing through 2025 and into 2026, and not for any of the reasons we keep telling ourselves. It isn't only the stretched valuations. It isn't only the war in West Asia. It is also the taxation on FIIs that's leading to their outflows.

Foreign investors began pulling out at a meaningful pace from late 2024, accelerated through the second half of 2025, and by mid-2026 the cumulative outflow have reached levels that domestic mutual funds have so far papered over.

The Double Toll: STT and LTCG

The Securities Transaction Tax (STT) was introduced in 2004 as a substitute for long-term capital gains tax. The political bargain was straightforward. Pay a tiny levy on every trade, and you will not be hounded for capital gains on equity held longer than a year. Fourteen years later that bargain was quietly broken.

STT survives at 0.1% on every delivery-based equity transaction, levied on both buy and sell legs, plus its own slabs on derivatives that were hiked in October 2024. And so does LTCG, raised in the July 2024 Union Budget from 10% to 12.5% beyond a threshold. Short-term gains were lifted at the same time from 15% to 20%.

The original quid-pro-quo from 2004 has been forgotten. The original tax came back, now at increased rates, with the STT not just holding up but also increased.

From a foreign investor's perspective, this stacks up quickly. An FII buying an Indian-listed stock in 2024 paid transaction costs on entry, watched the rupee slide from around Rs 83 to over Rs 95 against the dollar, and, on exit in 2026, paid LTCG tax on the rupee gain. That gain, however, may be illusory in the currency they actually report to investors in.

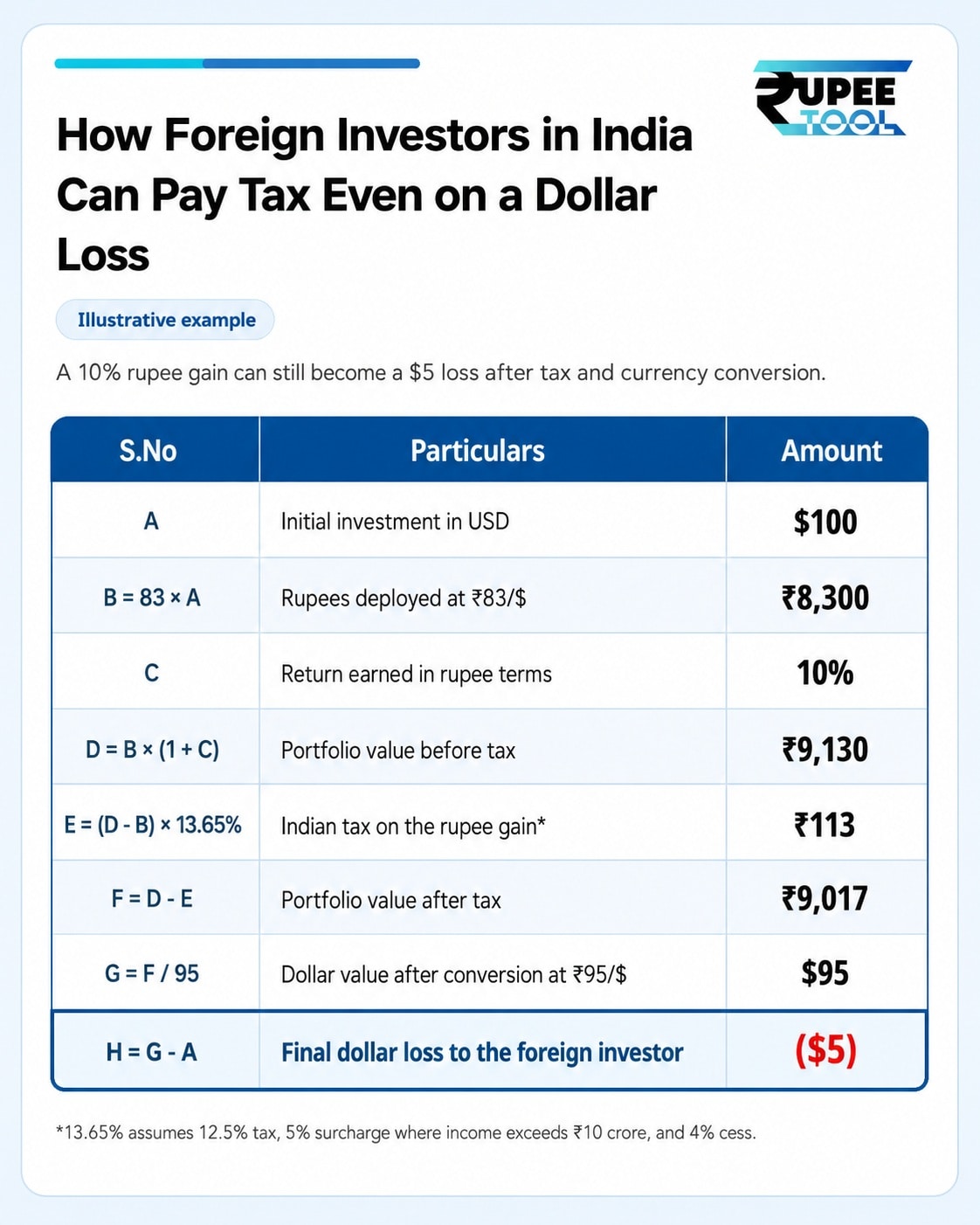

A simple illustration shows the problem:

In this example, the portfolio rises 10% in rupee terms, but after tax and currency depreciation, the foreign investor ends up with only $95 on an original $100 investment. In other words, the investor has suffered a $5 loss in dollar terms, even though India taxes the transaction as if a gain has been made.

Add stamp duty, GST on broking, exchange transaction charges and SEBI fees, and the all-in friction on a round trip becomes meaningful at any reasonable holding period. Together, they become exactly the kind of slow leak that compounds over time and shows up in the form FIIs notice most: weaker post-tax dollar returns.

The domestic story looks comforting on the surface, but it carries a deeper warning. As FIIs pull money out of India, domestic investors are increasingly becoming the exit liquidity. The steady rise in SIP flows, mutual fund participation and demat account openings has helped cushion the market against sharper corrections.

RBI data shows that household financial savings in mutual funds rose sharply from Rs 0.6 lakh crore in 2020-21 to Rs 4.7 lakh crore in 2024-25, while their share in gross household financial savings jumped from 2.1% to 13.1%. This means Indian households are absorbing a growing share of the supply that foreign investors are selling. In effect, domestic investors are being encouraged to keep buying equities at the same time global allocators are cutting exposure.

A Quick look at the neighbourhood: Where foreign investors pay nothing on gains

Foreign capital is extremely competitive. And India competition is extremely flattering.

Singapore and Hong Kong levy no capital gains tax on equities at all and have not for decades. Taiwan, despite being one of the world's hottest tech markets, does not subject most foreign equity gains to local capital gains taxes (CGT). The United States exempts non-resident foreigners from capital gains tax on most US stock holdings under long-standing IRS rules. The United Kingdom largely does the same.

India, in this peer set, is an outlier. It is the only major emerging market that combines a transaction tax on equities with a hiked capital gains tax and the only one of meaningful size that taxes foreign investors on rupee gains rather than dollar returns. For a Mumbai-based fund manager, this is a familiar fact. For a foreign allocator running a $2 billion EM portfolio in New York, Singapore or London, it is a line item in an Excel model that quietly weights India lower against Taiwan every quarter.

The July 2024 hike was, in this context, the worst possible signal. It came at the exact moment global capital was rotating toward AI-driven equity stories, a rotation India is structurally unable to win given its limited semiconductor and frontier-AI exposure. Telling a marginal allocator "we are raising your tax rate" when the relative story is already weakening invites the response that has, in fact, arrived.

As of late May 2026, South Korea has overtaken India to become the world's sixth-largest stock market, with Taiwan having edged ahead earlier in the year. That is not solely about tax policy, but tax policy is what is keeping the door open for the gap to widen.

ALSO READ | SEBI Set To Revive Buybacks, Fast-Track AIF Launches And Ease MF Norms At June 19 Meet

The Rupee Loop: Why a weaker currency compounds the damage

The rupee is not a passive variable in this story. It is the transmission belt that turns a tax irritation into a macro problem.

The chain works like this. FII outflows weaken the rupee. A weaker rupee makes dollar-priced imports, particularly crude oil, more expensive, puts pressure on the trade deficit and forces the RBI to intervene in the FX market to smooth currency volatility.

That pressure is already visible in the reserves data. From a record high of $728.49 billion in late February 2026, India's forex reserves fell to $681.38 billion as of May 22, 2026. That is a drawdown of around $47.1 billion, or roughly 6.5% from the peak, as the central bank leaned on its reserves to manage the rupee's slide. Each drawdown reduces the market's comfort around the rupee's perceived defensibility, which can further discourage foreign allocators already worried about currency risk.

A weaker rupee also raises the fiscal sensitivity of energy support. Since crude oil and LPG are dollar-linked while domestic consumers are partly insulated through subsidies, price controls or tax adjustments, currency weakness can increase pressure on government finances at exactly the wrong time.

The cruellest part of the loop, from a foreign investor's perspective, is the tax interaction. If the rupee falls from around 85 to 95 against the dollar over a holding period, an investor can lose money in dollar terms, the only thing that matters to them, and still owe capital gains tax in India if the rupee value of the position has risen. India is, in effect, taxing currency depreciation as if it were a gain. No serious global allocator models this favourably. Every quarter the rupee weakens, India's after-tax expected return falls twice: once through the FX loss and again through the tax on a phantom rupee gain.

A weaker rupee raises the cost of every Indian student studying abroad, every imported machine, every dollar-denominated corporate bond rollover and every pharmaceutical input. Exporters benefit, but not enough to fully offset the broad import drag, given that India remains structurally dependent on imported energy and capital goods.

The Valuation Premium India Can No Longer Defend

For years, the answer to all of this was that India is worth the friction. Markets traded at a premium because earnings growth was supposed to be exceptional and structural. That argument is now thinner than it has been in a decade.

The Nifty has spent most of 2025 and 2026 trading at forward earnings multiples meaningfully above the MSCI EM aggregate. A premium of that scale is justifiable only if delivered earnings growth materially outpaces the EM cohort. It has not, at least not at the rate the multiple implies. Mid- and small-cap valuations look more stretched still and broad market earnings revisions have been negative for several consecutive quarters since the second half of 2025. The simple truth is that India was being priced for a growth path that current numbers are not validating and global allocators noticed before retail did.

Layer the tax friction on top of an already expensive market and the maths becomes hard to defend. An allocator choosing between a tech-heavy index at 12 to 14x forward earnings with zero foreign CGT and an Indian index at 20 to 22x with STT plus 12.5% LTCG plus FX risk is no longer making a difficult call.

Domestic mutual funds, fed by monthly SIPs from middle-class households, have absorbed the gap. This is repeatedly described as "financial maturity". It is also, more honestly, household savings absorbing the risk that globally diversified capital decided to walk away from. If valuations correct meaningfully through the rest of 2026, the loss is concentrated on households who cannot diversify the way FIIs can.

Conclusion

None of this is irreversible, and none of it requires a particularly clever fix. STT and LTCG should not coexist. The original 2004 bargain should be honoured in one direction or the other. SLR should be reduced and corporate bond markets deepened so banks can actually lend the savings they hold. And the structural fiscal deficit, the real upstream cause of all of this, has to be addressed on the spending side, not by squeezing every available tax base until the most mobile one walks out.

Through most of 2024 and 2025, the state operated on the assumption that foreign capital, like domestic savers, had nowhere else to go. By mid-2026, foreign capital is patiently demonstrating that it does. The rupee, the banks and the valuation multiple are all telling the same story. It would be useful if policy heard it before the household SIP becomes the only thing left holding the market up.

Disclaimer: The views expressed in this article are solely those of the author and do not necessarily reflect the opinion of NDTV Profit or its affiliates. Readers are advised to conduct their own research or consult a qualified professional before making any investment or business decisions. NDTV Profit does not guarantee the accuracy, completeness, or reliability of the information presented in this article.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.