Asian equities nudged higher at the start of Monday trading, building on this year's strong start that's pushed the regional benchmark index to a record high as investors bet an expansion in corporate earnings won't falter any time soon.

The Singapore-traded SGX Nifty, an early indicator of NSE Nifty 50 Index's performance in India, rose 0.6 percent to 11,136 as of 7:05 a.m.

Here's a quick look at all that could influence equities on Monday.

Global Cues

- U.S. stocks rose the most since March on Friday as strong earnings outflanked concerns about trade spurred by Trump administration officials, whose comments helped push the dollar to its worst week in eight months.

- Ten-year U.S. bond yields headed toward the highest level in more than three years.

- The value of global equities has surpassed $60 trillion this year and government bond yields have rallied as investors assess the outlook for inflation alongside a gentle improvement in global economic growth.

Europe Check

- European stocks rebounded from the worst drop in a month as gains in health-care shares offset losses in oil and gas companies.

.png)

Asian Cues

- Japan's Topix index rose 0.1 percent.

- South Korea's Kospi index gained 0.6 percent.

- Australia's S&P/ASX 200 Index climbed 0.3 percent.

- Futures on Hong Kong's Hang Seng Index rose 0.3 percent.

- Futures on the S&P 500 Index were up 0.1 percent.

Here are some of the other key events scheduled for this week:

- Earnings season sees some technology giants report, including: Alibaba Group Holding Ltd., Apple Inc., Facebook Inc. and Amazon.com Inc.

- Federal Reserve policy makers gather for Chair Janet Yellen's final meeting on interest rates before her term ends.

- Bank of England Governor Mark Carney will speak before the U.K. Parliament's Economic Affairs Committee in London Tuesday.

- Gauges of Chinese manufacturing and services industries are due Wednesday.

- GDP reports including India and Taiwan are due Wednesday.

- U.S. employers probably added more jobs in January than a month earlier, while the jobless rate held at an almost 17-year low and the pace of wage growth picked up from a year ago, economists forecast the government report will show Friday.

- Donald Trump delivers his first State of the Union address on Tuesday.

Coincheck to repay users who lost money in $400 million hack. https://t.co/Lv4a3NDiwu

Commodity Cues

- West Texas Intermediate crude gained 0.1 percent to $66.19 a barrel, the highest in more than two years.

- Brent crude rose to $70.52 a barrel, its second highest settlement of the year.

- Spot Gold trades higher for second day at $1,351.1 an ounce; up 0.2 percent.

- Sugar ended higher for second day at 13.36 cents per pound; up 0.9 percent.

Shanghai Exchange

- Steel trades lower for second day; down 0.1 percent.

- Aluminium trades lower for second day; down 0.2 percent.

- Zinc trades higher; up 0.3 percent.

- Copper trades lower for second day; down 0.1 percent.

- Rubber trades higher; up 0.2 percent.

Why Gujarat's cotton spinning mills are struggling in the peak season. #Budget2018 https://t.co/tB72x2BK6y pic.twitter.com/a44lXxM5pf

Indian ADRs

Nifty Earnings To Watch

- HDFC

- Tech Mahindra

Other Earnings To Watch

- Astra Microwave Products

- Astron Paper

- Century Textiles

- Emami

- Emkay Global

- Himadri Speciality Chemical

- IDFC

- Inox Leisure

- Laurus Labs

- Nava Bharat Ventures

- Reliance Communications

- Sun Pharma Advanced Research

- Wockhardt

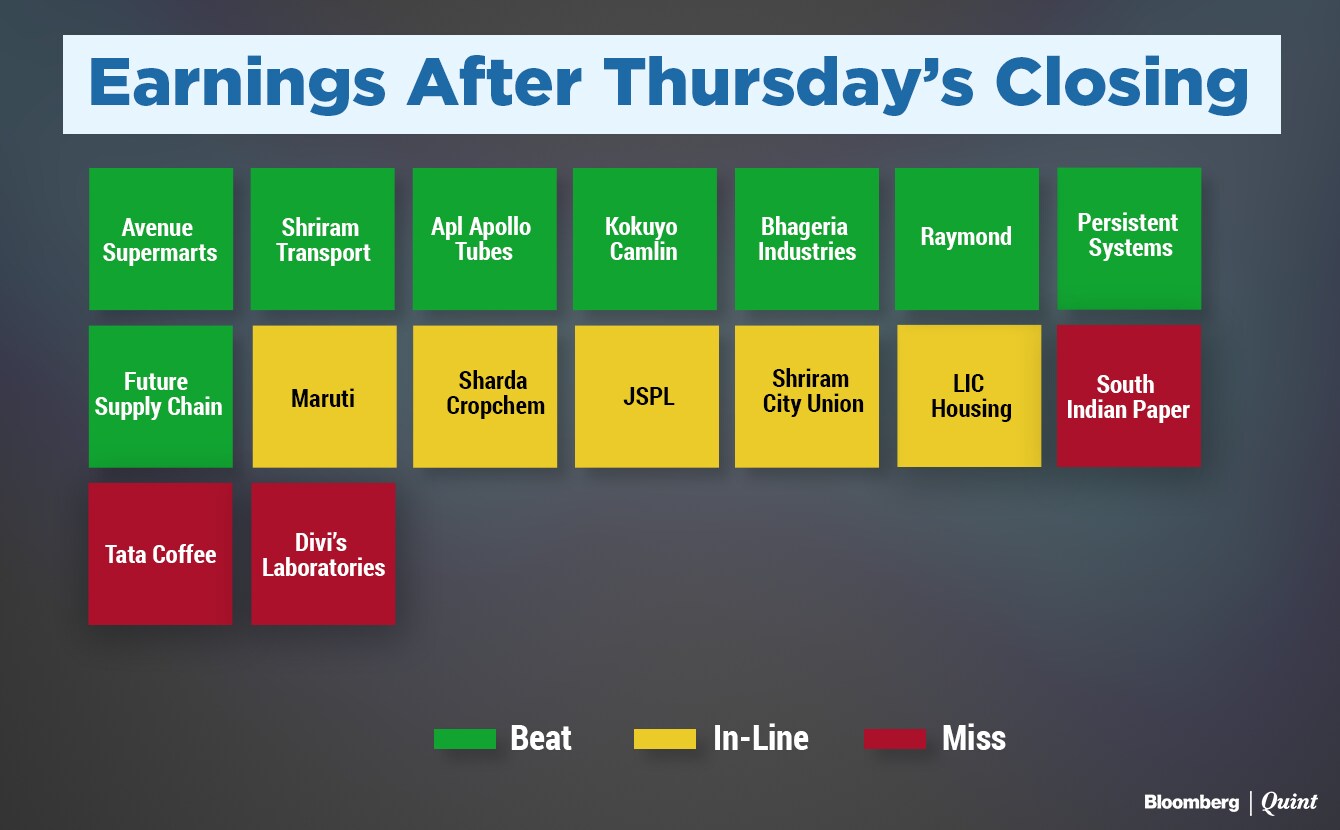

Earnings Reaction To Watch

Maruti Suzuki Q3 (YoY)

- Net sales up 14.2 percent at Rs 19,283 crore.

- Ebitda up 22.1 percent at Rs 3,038 crore.

- Profit up 3 percent at Rs 1,799 crore.

- Margins at 15.8 percent versus 14.7 percent.

Avenue Supermarts Q3 (YoY)

- Revenue up 23 percent at Rs 4,095 crore.

- Net profit up 66 percent at Rs 252 crore.

- Ebitda up 47 percent at Rs 422 crore.

- Margins at 10.3 percent versus 8.6 percent.

Shriram Transport Finance Q3 (YoY)

- NII up 21.1 percent at Rs 17,42.2 crore.

- Net profit up at Rs 495.6 crore.

APL Apollo Tubes Q3 (YoY)

- Revenue up 39 percent at Rs 1,314 crore.

- Net profit up 24 percent at Rs 36 crore.

- Ebitda up 18 percent at Rs 88 crore.

- Margins at 6.7 percent versus 7.9 percent.

Kokuyo Camlin Q3 (YoY)

- Revenue up 13 percent at Rs 143.5 crore.

- Net profit of Rs 5 crore versus net loss of Rs 3 crore.

- Ebitda up 525 percent at Rs 12.5 crore.

- Margins at 8.7 percent vs 1.6 percent.

Sharda Cropchem Q3 (YoY)

- Revenue up 34 percent at Rs 325.5 crore.

- Net profit down 43 percent at Rs 10 crore.

- Ebitda up 11 percent at Rs 35.5 crore.

- Margins at 10.9 percent versus 13.2 percent.

South Indian Paper Mills Q3 (YoY)

- Revenue up 2 percent at Rs 52 crore.

- Net profit up 17 percent at Rs 3.4 crore.

- Ebitda down 35 percent at Rs 6.5 crore.

- Margins at 12.5 percent versus 19.6 percent

Jindal Steel & Power Q3 (YoY)

- Revenue up 21 percent at Rs 6,993 crore.

- Net loss of Rs 266 crore vs net loss of Rs 407 crore.

- Ebitda up 26 percent at Rs 1,607 crore.

- Margins at 23 percent versus 22.1 percent.

Shriram City Union Finance Q3 (YoY)

- Net Interest Income up 20 percent at Rs 916 crore.

- Net profit up 43 percent at Rs 225.5 crore.

LIC Housing Finance Q3 (YoY)

- Revenue from operations grew 6.4 percent to Rs 3,738 crore.

- Net profit fell 1.7 percent to Rs 491 crore.

- Provisions at Rs 48.5 crore versus Rs 57.8 crore (QoQ).

Tata Coffee Q3 (YoY)

- Revenue down 8 percent at Rs 377 crore.

- Net profit up 45 percent at Rs 43 crore.

- Ebitda down 6 percent at Rs 75.5 crore.

- Margin at 20.0 percent versus 19.5 percent.

Bhageria Industries Q3 (YoY)

- Revenue up 18 percent at Rs 90 crore.

- Net profit up 128 percent at Rs 14.6 crore.

- Ebitda up 143 percent at Rs 25 crore.

- Margin at 28 percent versus 13.6 percent.

Future Supply Chain Q3 (YoY)

- Net profit up 37 percent at Rs 16.8 crore.

- Revenue up 36.4 percent at Rs 195 crore.

- Ebitda up 60.5 percent at Rs 32.9 crore.

- Margin at 16.9 percent versus 14.3 percent.

Divi's Laboratories Q3 (YoY)

- Revenue up 8 percent to Rs 1,038 crore.

- Net profit down 16 percent to Rs 225 crore.

- Ebitda down 9 percent to Rs 342 crore.

- Margin at 33 percent versus 39 percent.

Persistent Systems Q3 (QoQ)

- Revenue up 4 percent to Rs 792 crore.

- EBIT up 26 percent to Rs 98 crore.

- EBIT margin at 12.4 percent versus 10.2 percent.

- Net profit up 11 percent to Rs 92 crore.

#Q3WithBQ | India's most valued retailer says consumers are buying more than they need.https://t.co/Y3G0IA0Gwm pic.twitter.com/Bs6sdKRZmQ

Stocks To Watch

- Reliance Jio to introduce new affordable plan on Jan 26; offer free voice and unlimited data for Rs 49 for 28 days.

- Government nod to Reliance Industries, BP acquiring Niko's 10 percent stake in gas block.

- Idea Cellular seeks govt nod for raising FDI limit to 100 percent.

- Bharat Forge sets up unit in Israel.

- APL Apollo Tubes terminates JV with One to One Holdings PTE.

- Kokuyo Camlin to wind up Camlin International.

- Sanghi Industries to raise Rs 400.17 crore via QIP. To issue 3.10 crore equity shares at Rs 129 each.

- Ganesh Housing to sell 51 percent stake in Shaily Infrastructure.

- Prataap Snacks signs new pact for third party manufacturing of potato chips at 3 places.

- Raymond to buy 26 percent in Shahane solar power.

- FDC gets GMP nod from U.K. regulators for its Ophthalmic manufacturing facility at Waluj, Aurangabad.

- Havells to set up a new facility to manufacture consumer durables in Rajasthan for a total investment of Rs 360 crore.

- Amrutanjan Health to consider stock split on Feb. 13.

- Hindustan Copper to consider raising funds via QIP.

- Avenue Supermarts to acquire additional 4.35 crore shares or 50.79 percent in Avenue E-Commerce for Rs 49.2 crore.

- Fiem Industries says plant, machinery damaged in fire incident at Hosur unit.

#Budget2018 | Government may consider import duty hike on some medical devices.https://t.co/CWKL4ChRyG pic.twitter.com/aQ1gEro3Wc

Bulk Deals

- PC Jewellers: Vakrangee bought 20 lakh shares or 0.5 percent equity at Rs 561.71 each.

- IDFC: Balanced Fund - ICICI Prudential AMC sold 86 lakh shares or 0.5 percent equity at Rs 56.6 each.

New Listing/Offerings

- Newgen Software Technologies to start trading on the bourses after IPO gets 8.25 times demand.

- Galaxy Surfactants' IPO opens on Monday. (Here's all you need to know about the IPO).

Who's Meeting Whom

- Vakrangee to meet analysts/investors from Jan. 29 to Feb. 13 in U.S. and Canada.

- Symphony to meet Ecofin Asset Management and Greenfield Advisory on Jan. 29.

- Canara Bank to meet investors from Jan. 30 - Feb. 9.

- Sequent Scientific to meet investors on Jan. 31.

Should you switch from small and mid-cap mutual funds? #BQMutualFundShow @_nirajshah @jayeshkhilnanihttps://t.co/cL1YpeZCz5 pic.twitter.com/X9SbgpS78e

Insider Trades

- Gujarat Apollo promoter Dhruv Patel sold 15,000 shares on Jan. 24.

- Mastek promoter Sudhakar Ram sold 1 lakh shares from Jan. 23 – 24.

- KCP Ltd. promoter V R K Grandsons Investments sold 66,270 shares from Jan. 23 – 24.

Trading Tweaks

- Indo Count Industries' and JSW Energy's circuit filter revised to 20 percent.

Rupee

- Rupee ends at 63.54/$ on Thursday versus 63.69/$ on Wednesday.

Top Gainers And Losers

Index Trends

F&O Cues

- Nifty February futures trade at 11,062.6 discount of 7 points versus premium of 19 points.

- Across series-Nifty OI up 6 percent, Bank Nifty OI down 4 percent.

- India VIX ended at 17.5, down 3 percent.

- Rollover-Nifty at 66 percent, Bank Nifty at 71 percent

- Max OI for February series at 12,000 Call (OI at 24 lakh) followed by 10,800 call strike (OI at 22.6 lakh)

- Max OI for February series at 10,500 Put, OI at 48.2 lakh, OI up 21 percent

P-Notes investments hit six-month high of Rs 1.5 lakh crore in December. https://t.co/zbyPEGO09w pic.twitter.com/GAxjPTaHsi

F&O Ban

- In Ban: JP Associates

Alert: Only intraday positions can be taken in stocks which are in F&O ban. There is a penalty in case of rollover of these intraday positions.

Put-Call Ratio

- Nifty PCR at 1.42 versus 1.81.

- Nifty Bank PCR at 1.26 versus 1.43.

BSE's top 9 companies added Rs 97,932 crore to market cap.https://t.co/4wLMM8qZ78 pic.twitter.com/zhbqFPcwrZ

Stocks Seeing High Open Interest Change

Fund Flows

Brokerage Radar

ICICI Direct on TCI Express

- Initiated ‘Buy' with price target of Rs 660.

- GST, e-way bill - structural impetus to organised segment.

- Specialist logistics services like express delivery to gain momentum.

- Sorting centres to provide better efficiencies.

- Positives: low leverage, robust growth trajectory and high return ratios.

- Reduction in rental expense, efficiencies to drive operating income

- Expect revenue, operating income and net profit to compound at 16 percent, 29 percent and 29 percent respectively over the financial years through March 2020.

- Return ratios to remain one of the best in the industry.

- Healthy cash flow to internally fund capex requirements.

- Expect TCI Express to command premium valuations.

Axis Securities on IG Petrochemicals

- Initiated ‘Buy' with price target of Rs 860.

- Market leadership in PhthalicAnhydride industry in India; 49 percent market share.

- Domestic PAN industry expected to grow at 6-8 percent per annum over the next few years.

- Acquisition of new business and capacity expansion to help in volume growth.

- Capacity expansion to address demand supply mismatch.

- Capacity utilisation to be above 90 percent over the financial years through March 2019.

- Expect revenue and net profit to grow at a compounded rate of 13 percent and 32 percent respectively over the financial years through March 2019.

- Strong financials, to improve further.

- Expect return ratios to reduce a bit due to ongoing expansion plans.

Jefferies on Maruti Suzuki

- Maintained ‘Buy'; raised price target to Rs 10,720 from Rs 9,245.

- Positive surprise on margin during December quarter drives operating income beat.

- Lower royalty on new models.

- Revise up near- and long-term margin estimates.

- Revised to factor in marginally higher revenue, better margins and lower other income.

- Maruti remains best way to play large long-term PV opportunity in India.

Credit Suisse on Maruti Suzuki

- Maintained ‘Neutral'; raised price target to Rs 9,800 from Rs 9,400.

- December quarter showed strong operational performance.

- Lower other income impacted reported numbers.

- Decline in royalty rates going forward the key positive.

- Low-double-digit growth possible in the next financial year.

- Facelift of showrooms to pick up pace in coming years.

Nomura on Maruti Suzuki

- Maintained ‘Buy'; raised price target to Rs 11,245 from Rs 9,843.

- December quarter was strong driven by cost control and lower promotion expenses.

- High growth visibility, premiumisation and royalty reduction to drive profitability.

- Expect revenue and earnings per share to compound at 17 percent and 19 percent respectively over the financial years through March 2020.

- Expect free cash flow generation to continue to rise sharply.

- Maruti Suzuki remains top pick.

Deutsche Bank on Dr. Reddy's

- Maintained ‘Hold'; cur price target to Rs 2,163 from Rs 2,310.

- Testing times as key U.S. launches are delayed.

- Should test existing investor optimism on stock.

- Strong pipeline but timelines have been delayed.

- Base business price erosion will stabilise in a few quarters, says management.

- Favourable outcome on impending re-inspection at Duvvada, a key monitorable.

Goldman Sachs on Dr. Reddy's

- Maintained ‘Neutral'; cut price target to Rs 2,360 from Rs 2,450.

- December quarter results were broadly in-line.

- Higher-than-expected U.S. sales offset weaker-than-expected India sales.

- Pipeline updates indicated that key products likely to see delay in launch.

- Lower operating income estimates by 2-6 percent.

Credit Suisse on Dr. Reddy's

- Maintained ‘Underperform' with price target of Rs 1,865.

- US sales increased sharply QoQ but margins disappointed.

- US sales in current quarter should be significantly lower than previous quarter

- India and Russia growth weaker than expected.

- Cut current fiscal's earnings per share estimates by 9 percent due to competition in key U.S. products.

- Copaxone opportunity delayed by a year.

CLSA on UPL

- Maintained ‘Buy' with price target of Rs 960.

- December quarter posted weak revenues due to pricing pressure and delayed planting season

- Price growth remained negative, but volume growth remains robust.

- UPL to benefit from improving industry dynamics this year.

- UPL well positioned to benefit from recovery in market.

Deutsche Bank on UPL

- Maintained ‘Buy'; cut price target to Rs 940 from Rs 960.

- Previous quarter was Operationally lower; Tax writeback leads to PAT beat.

- Rising cost of production in China is improving the prospects for UPL.

- Market share gains to continue, driven by launches of new formulations.

- Reiterating Buy on robust EPS growth and reasonable valuation.

- Correction a buying opportunity.

Edelweiss on UPL

- Maintained ‘Buy'; raised price target to Rs 1,023 from Rs 963.

- December quarter volumes jumped 12 percent; Currency impact persists.

- Debt remained stable; Working capital reduced.

- Fall in interest cost and tax write-back drive net profit.

- Expect stable growth.

- Significant reduction in debt can lead to improved valuations.

HSBC on Avenue Supermarts

- Upgraded to ‘Buy' from ‘Hold'; raised price target to Rs 1,600 from Rs 900.

- Avenue's December quarter's profits were significantly ahead of expectations.

- Revenue growth momentum and margin expansion led to beat.

- D-Mart business model is formidable, scalable and a winning proposition.

- Avenue will be able to capture value from structural growth ahead of competition.

- Valuation not ahead of long term fundamentals.

Edelweiss on Avenue Supermarts

- Maintained ‘Hold' with price target of Rs 1,290.

- December quarter numbers were robust.

- Benefit of gross margin coupled with operating leverage helped D-Mart.

- Store expansion seems to have slowed; Will be key monitorable going forward.

- Expect revenue, operating income and net profit to grow at a compounded rate of 25.5 percent, 31.8 percent and 41.2 percent respectively over the financial years through March 2020.

- We perceive limited upside on the stock.

- D-Mart is a play on the Indian retail story.

Credit Suisse on Jindal Steel & Power

- Maintained ‘Neutral' with price target of Rs 150.

- December quarter beat across all divisions.

- Beat driven by higher EBITDA/unit.

- Shadeed continues to post strong operating income.

- Net debt was flattish QoQ.

- Await details on Angul.

HSBC on Mphasis

- Maintained ‘Hold'; raised price target to Rs 730 from Rs 680.

- Strong quarterly revenue growth in December quarter; Margins improve despite wage hike.

- Growth was broad-based with both HP/DXC and Direct up.

- Stock valuations factor in this optimism.

- Expect revenue and operating income to grow at a compounded rate of 10 percnet and 12 percent respectively over the financial years through March 2020.

Nomura on LIC Housing Finance

- Maintained ‘Buy'; raised price target to Rs 720 from Rs 660.

- December quarter results were operationally in-line with expectations.

- Near-term PPOP growth likely to remain weak.

- Remain cautious on incremental mortgage spreads.

- Large part of the de-rating is done and valuations have bottomed out.

- Spreads pressure now priced in; Maintain Buy on reasonable valuations.

Kotak on Shriram City

- Upgraded to ‘Add' from ‘Reduce'; raised price target to Rs 2,275 from Rs 2,200.

- Signs of turnaround seen after several quarters of weak performance.

- Strong NII and decline in provisions lift net profit.

- Positives: strong growth in business loans, reduction in GNPL ratio and provision and lower borrowing costs.

- Expect business trajectory to improve hereon.

- Expect near-term performance to remain strong.

Morgan Stanley on Shriram City

- Maintained ‘Equal-weight' with price target of Rs 2,300.

- Improvement across metrics in line with expectations.

- NPL formation moderated but remains elevated.

- NIM improved despite high NPL formation.

- AUM and disbursements growth picked up.

- Valuation is attractive, but asset quality and growth have been volatile.

Kotak on Tata Motors

- Maintained ‘Buy'; cut price target to Rs 525 from Rs 535.

- Factoring in recent production cut announcement by JLR.

- JLR announced production cuts in first quarter of next fiscal due to low demand.

- Demand for new models will continue to drive growth for JLR.

- Changes to estimates led by currency changes and JLR volume cuts.

Credit Suisse on Hindalco

- Maintained ‘Outperform' with price target of Rs 310.

- Novelis on path to deleveraging despite capex announcement.

- Net Debt/EBITDA to stay low going ahead.

- Remain constructive on Hindalco.

HSBC on Pheonix Mills

- Maintained ‘Buy'; raised price target to Rs 720 from Rs 580.

- Next fiscal to be year of strong cash flow generation.

- Expect strong cash flow as stake purchases completed and under construction properties ready.

- Current holding structures to open-up value unlocking and monetisation options.

- Lower cost of capital mean falling debt cost.

- Expect weak residential sales momentum.

What Dalal Street wants from #Budget2018https://t.co/VUyoAeX0jp pic.twitter.com/xVWIL5Ivan

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.

.png)

.png)

.png)

.png)