(Bloomberg Opinion) -- A senior Chinese central banker declared this week that he had few worries. President Xi Jinping's modest target of 5% growth, reckoned to be in jeopardy not long ago, is now in sight. That success comes with big caveats, not least of which is inflation. The problem is there isn't any.

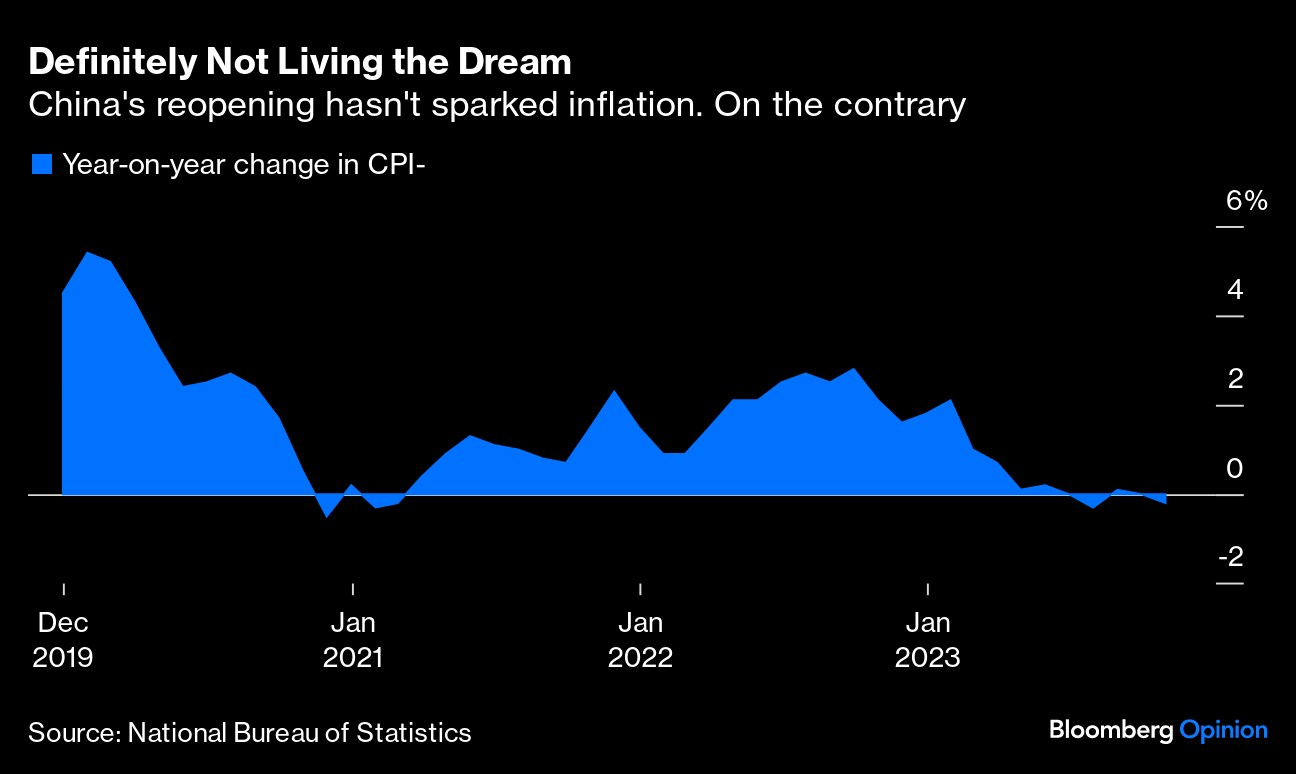

Consumer prices, languishing for a while, took a new step down in October. They dropped 0.2% from a year earlier, according to government figures released on Thursday, while factory-gate prices slipped 2.6%. That's a tad worse than economists expected, but the real disappointment is that it suggests a meaningful recovery is some time away, no matter how good gross domestic product might look in the very short term. Former People's Bank of China Governor Yi Gang once described inflation of 2% as a central banker's dream. By that yardstick, China falls short.

This is miles away from the situation that the Federal Reserve and most other central banks confront. Price increases elsewhere are cooling, though still a way from their comfort zones. For policymakers in Beijing, the challenge is of a different nature: escaping the specter of deflation. For all the reasonably positive short-term news on growth in China, declining prices point to anemic levels of demand.

When CPI dipped below zero over the summer, the news triggered an outbreak of anxiety: “What-the-heck-has-happened-to-China?” Is the world going to hell as a result? It was as though people hadn't grasped that China was in a long-term, if gradual, slowdown well before the pandemic. This wasn't a disaster, and still doesn't have to be. But prices that lie flat, or go into reverse, remind us that all is not well.

It's unfortunate because, after a mid-year retreat in growth, things had been looking a bit better. The economy expanded faster than anticipated last quarter, and a string of investment banks lifted their forecasts, UBS AG and JPMorgan Chase & Co. among them. The International Monetary Fund sounded upbeat. Imports are growing and car sales are on the rise, according to figures this week. Zhang Qingsong, deputy governor of the People's Bank of China, was upbeat. “You may ask me, are you worried? No, not always, not too much,” he told bankers on Tuesday. He was talking about long-term prospects, but near hurdles need attention.

Given the surge in inflation in most major economies last year, you might think cheaper stuff is a blessing for China — or any country. Not really. A protracted fall in prices tends to create the expectation that, if companies or consumers wait a bit longer to make a major purchase, then things will be even less expensive. Businesses relentlessly seek ways to cut their own costs, including investment and, in time, wages and jobs. In a widely cited 2002 speech, Ben Bernanke, then a Fed governor, left no doubt about its corrosiveness. “Sustained deflation can be highly destructive to a modern economy and should be strongly resisted,” he warned.

Interest rates can be cut. The PBOC has been lowering them for a while, though it's been reluctant to make deep reductions. Bloomberg Economics projects a trim of 10 basis points in the main rate next week. There's a huge role for fiscal policy, too, and Beijing appears to be on board. Last month, the legislature green-lighted the deficit exceeding the traditional limit of 3% of GDP. There's now a greater sense of urgency.

The dour statistics remind us how far China has to go before its economy can hum again — at a pace of growth more like that of other major powers, not the exceptional beast of yesteryear. Given the traumas in global policymaking in the past few years, it's easy to forget that in 2017 Janet Yellen, then Fed chair, almost sounded wistful about perky inflation.

Its quiescence in the midst of a long expansion was dubbed a “mystery” by Yellen, who is now Treasury secretary. China can probably relate. Such is the tyranny of being a grown-up economy, complete with ups and downs.

More From Bloomberg Opinion:

- The Yuan's Slide Doesn't Have to End in Tears: Daniel Moss

- Why Investors Fell Out of Love With China Vanke: Shuli Ren

- The Federal Reserve's Pause Could Go Terribly Wrong: Bill Dudley

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously, he was executive editor for economics at Bloomberg News.

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.