Interest from bank deposits is added to one's income and taxed according to the respective tax slabs.

- Investors can buy tax-free bonds from secondary markets

- Tax-free bonds were issued by government-owned entities in past few years

- Investors can deploy some corpus in these bonds, say financial planners

The Reserve Bank of India has brought down its key lending rate by 175 basis points in the last two years, sharply bringing down the interest rates in bank fixed deposits. For example, State Bank of India - the country's largest lender - has cut its interest rate on one-year fixed deposits by 135 basis points, according to estimates.

Falling interest rates and the income tax factor have brought down the appeal of fixed deposits for many investors, particularly for those in higher tax brackets. Interest from bank deposits is added to one's income and taxed according to the respective tax slabs.

This has increased the appeal of tax-free bonds which were issued by government-owned entities in the past few years. These bonds were a huge hit among investors who looked for a steady tax-free interest income but this fiscal year there would not be fresh issues of tax-free bonds. Since tax-free bonds are traded on exchanges, investors can buy them from secondary markets.

With the RBI expected to further cut its key lending rate, financial planners say that investors - particularly those in higher tax brackets - can consider deploying some corpus in the tax-free bonds through secondary purchases.

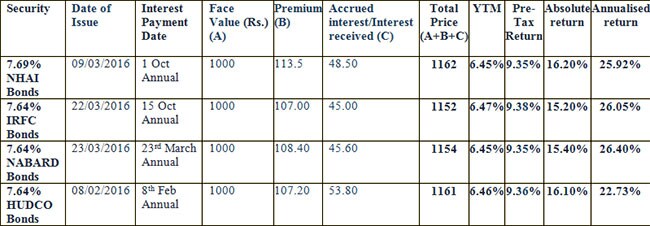

It is not surprising that the prices of tax-free bonds trading in the secondary market have witnessed a sharp rally. For example, the return in 7.69 per cent NHAI tax-free bonds, 7.64 per cent IRFC bonds and 7.64 per cent NABARD bonds have topped over 15 per cent. These bonds were issued earlier this year. Source: Synergee Capital Services (pre-tax return is calculated for investors in 30 per cent tax bracket)

Source: Synergee Capital Services (pre-tax return is calculated for investors in 30 per cent tax bracket)

Yield to maturity or YTM is the total return anticipated on a bond if the bond is held until the end of its lifetime.

The interest rate or coupon on tax-free bonds in the previous years had been issued in line with the then-prevailing yield on government bonds. "Since then, the 10-year government bond yields have now moved to sub-7 per cent in the same period. More importantly, there is no further issuance of any tax free bonds. Both these factors have led to the appreciation in the prices of the already issued tax free bonds," said Manoj Nagpal, CEO of Outlook Asia Capital.

Vikram Dalal, managing director at Synergee Capital Services, says tax-free bonds are a good alternative for investors in higher tax brackets.

"We recommend investment in tax-free bonds, for an investor who is into 30 per cent tax bracket. The Pre-tax return is more than 9.25 cent vs bank deposits (SBI) offering 7.25 per cent for five-year tenure," Mr Dalal said.

Moreover, since the interest income on the bonds is tax exempt, no TDS (tax deduction at source) is levied, unlike bank deposits

Capital gains made on selling of tax-free bonds on stock exchanges are taxed. If the holding period is less than 12 months, capital gains on sale of tax-free bonds on stock exchanges are taxed as per the tax slab of the investor. If bonds are held for more than 12 months, the gains are subjected to tax rate of 10 per cent without any indexation benefit.

However, Mr Nagpal, CEO of Outlook Asia Capital, says liquidity is fairly limited in the secondary markets so it may be a "difficult proposition to acquire the bonds of significant investment value".

Falling interest rates and the income tax factor have brought down the appeal of fixed deposits for many investors, particularly for those in higher tax brackets. Interest from bank deposits is added to one's income and taxed according to the respective tax slabs.

This has increased the appeal of tax-free bonds which were issued by government-owned entities in the past few years. These bonds were a huge hit among investors who looked for a steady tax-free interest income but this fiscal year there would not be fresh issues of tax-free bonds. Since tax-free bonds are traded on exchanges, investors can buy them from secondary markets.

With the RBI expected to further cut its key lending rate, financial planners say that investors - particularly those in higher tax brackets - can consider deploying some corpus in the tax-free bonds through secondary purchases.

It is not surprising that the prices of tax-free bonds trading in the secondary market have witnessed a sharp rally. For example, the return in 7.69 per cent NHAI tax-free bonds, 7.64 per cent IRFC bonds and 7.64 per cent NABARD bonds have topped over 15 per cent. These bonds were issued earlier this year.

Yield to maturity or YTM is the total return anticipated on a bond if the bond is held until the end of its lifetime.

The interest rate or coupon on tax-free bonds in the previous years had been issued in line with the then-prevailing yield on government bonds. "Since then, the 10-year government bond yields have now moved to sub-7 per cent in the same period. More importantly, there is no further issuance of any tax free bonds. Both these factors have led to the appreciation in the prices of the already issued tax free bonds," said Manoj Nagpal, CEO of Outlook Asia Capital.

Vikram Dalal, managing director at Synergee Capital Services, says tax-free bonds are a good alternative for investors in higher tax brackets.

"We recommend investment in tax-free bonds, for an investor who is into 30 per cent tax bracket. The Pre-tax return is more than 9.25 cent vs bank deposits (SBI) offering 7.25 per cent for five-year tenure," Mr Dalal said.

Moreover, since the interest income on the bonds is tax exempt, no TDS (tax deduction at source) is levied, unlike bank deposits

Capital gains made on selling of tax-free bonds on stock exchanges are taxed. If the holding period is less than 12 months, capital gains on sale of tax-free bonds on stock exchanges are taxed as per the tax slab of the investor. If bonds are held for more than 12 months, the gains are subjected to tax rate of 10 per cent without any indexation benefit.

However, Mr Nagpal, CEO of Outlook Asia Capital, says liquidity is fairly limited in the secondary markets so it may be a "difficult proposition to acquire the bonds of significant investment value".

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.