Stock Market Highlights: Nifty Reclaims 23,650 After Reversing Morning Losses, Sensex Settles 100 Points Higher

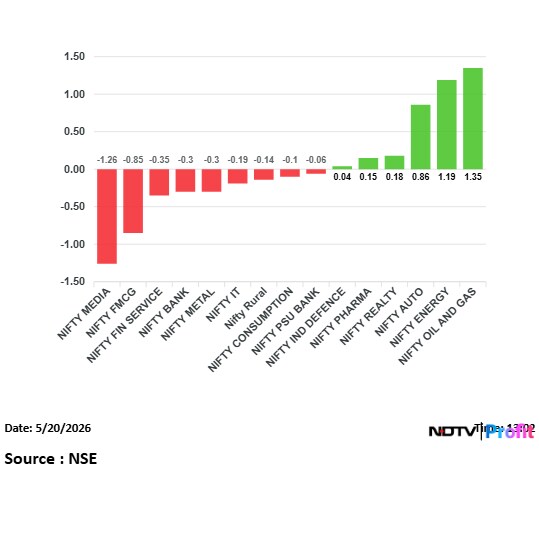

Nifty Oil & Gas was the top-performing sector, while FMCG lagged. Bank and Metal indices snapped a three-day losing streak, while Pharma and IT ended lower after recent gains.

Indian equity benchmarks ended higher, reversing all of their morning losses during the last-hour trade. The NSE Nifty 50 rose 0.17% to close at 23,659.00, while the BSE Sensex gained 0.16% to end at 75,318.39. Both indices had fallen as much as 0.9% earlier in the session before recovering.

Nifty Oil & Gas was the top-performing sector, while FMCG lagged. Bank and Metal indices snapped a three-day losing streak, while Pharma and IT ended lower after recent gains.

Elsewhere, S&P 500 futures rose 0.1% and Nasdaq 100 futures gained 0.4% after earlier declines. Dow Jones futures fell 12 points, or 0.02%, trimming sharper overnight losses.

Stock Market Wrap: Nifty Ends Above 23,650; Oil & Gas Leads Sectoral Gains

- Nifty 50 ended higher by over 0.2%, closing above the 23,650 mark, with Hindalco and Reliance among top gainers

- Midcap and smallcap indices also ended in green, with the Midcap 150 outperforming benchmarks

Nifty Oil & Gas was the top-performing sector, while FMCG lagged. Bank and Metal indices snapped a three-day losing streak, while Pharma and IT ended lower after recent gains.

Stock Market Live: Rupee Ends At Record Low Against US Dollar

- The rupee weakened 0.3% to close at 96.83 per US dollar

- It fell from 96.54 in the previous session

The currency recorded its weakest closing level against the US dollar.

Stock Market Live: Nifty, Sensex End Higher After Recovering From Early Losses

- Nifty rose 0.17% to close at 23,659.00, while the Sensex gained 0.16% to end at 75,318.39

- Both indices had fallen as much as 0.9% earlier in the session before recovering

- The benchmarks staged a rebound through the day to close in positive territory.

Stock Market Live: Lenskart Q4 Profit Falls 8.5%, Revenue Jumps 46%

- Net profit declined 8.5% to Rs 200 crore, while revenue rose 45.6% to Rs 2,516 crore

- EBITDA increased 83.8% to Rs 540 crore, with margin expanding to 21.4% from 17%

The company said it will acquire additional stake in its arm Owndays Inc and is proposing a merger of Dealskart Online and Lenskart Eyetech.

Stock Market Live: Ola Electric Q4 Loss Narrows, Revenue Declines

- Net loss stood at Rs 500 crore compared with Rs 870 crore a year ago

- Revenue fell 56.6% to Rs 265 crore

The company reported an EBITDA loss of Rs 281 crore, narrowing from Rs 695 crore in the previous year.

Stock Market Live: HUL Backs Govt Austerity Push, Expands Renewable Use

- Hindustan Unilever said it supports the government’s call for fuel conservation and austerity

- Over 97% of energy used in its operations comes from renewable sources

The company said it is scaling up EV use in its supply chain and limiting foreign travel to essential needs, while continuing hybrid work practices.

Stock Market Live: Grasim Reports Growth In Fibre And Caustic Soda Volumes

- Cellulosic staple fibre volume rose 12% year-on-year to 2.32 lakh tonnes

- Revenue from the cellulosic fibre segment increased 14% to Rs 4,614 crore

Caustic soda volume grew to 3.2 lakh tonnes compared with 2.9 lakh tonnes a year ago, indicating higher output across key segments.

Stock Market Live: Eris Life Q4 Profit Rises On Tax Credit, Declares Dividend

- Net profit stood at Rs 282 crore compared with Rs 94 crore a year ago, supported by a tax credit of Rs 120 crore

- Revenue increased 7.3% to Rs 756.6 crore, while EBITDA margin improved to 36.2%

The company announced an interim dividend of Rs 7.21 per share.

Stock Market Live: Samvardhana Motherson Q4 Profit Rises 46%, Beats Estimates

- Profit rose 46% to Rs 1,497 crore, ahead of estimate of Rs 1,321 crore

- Revenue increased 9% to Rs 34,304 crore, above estimate of Rs 32,749 crore

EBITDA rose 24.6% to Rs 3,792 crore, with margin at 11.1%, exceeding estimates. The company reported broad-based growth across revenue, profitability and margins on a year-on-year basis.

Stock Market Live: US Futures Turn Mixed; Nasdaq Gains While Dow Slips

- S&P 500 futures rose 0.1% and Nasdaq 100 futures gained 0.4% after earlier declines

- Dow Jones futures fell 12 points, or 0.02%, trimming sharper overnight losses

The moves indicate mixed signals for US equities after futures recovered from initial weakness.

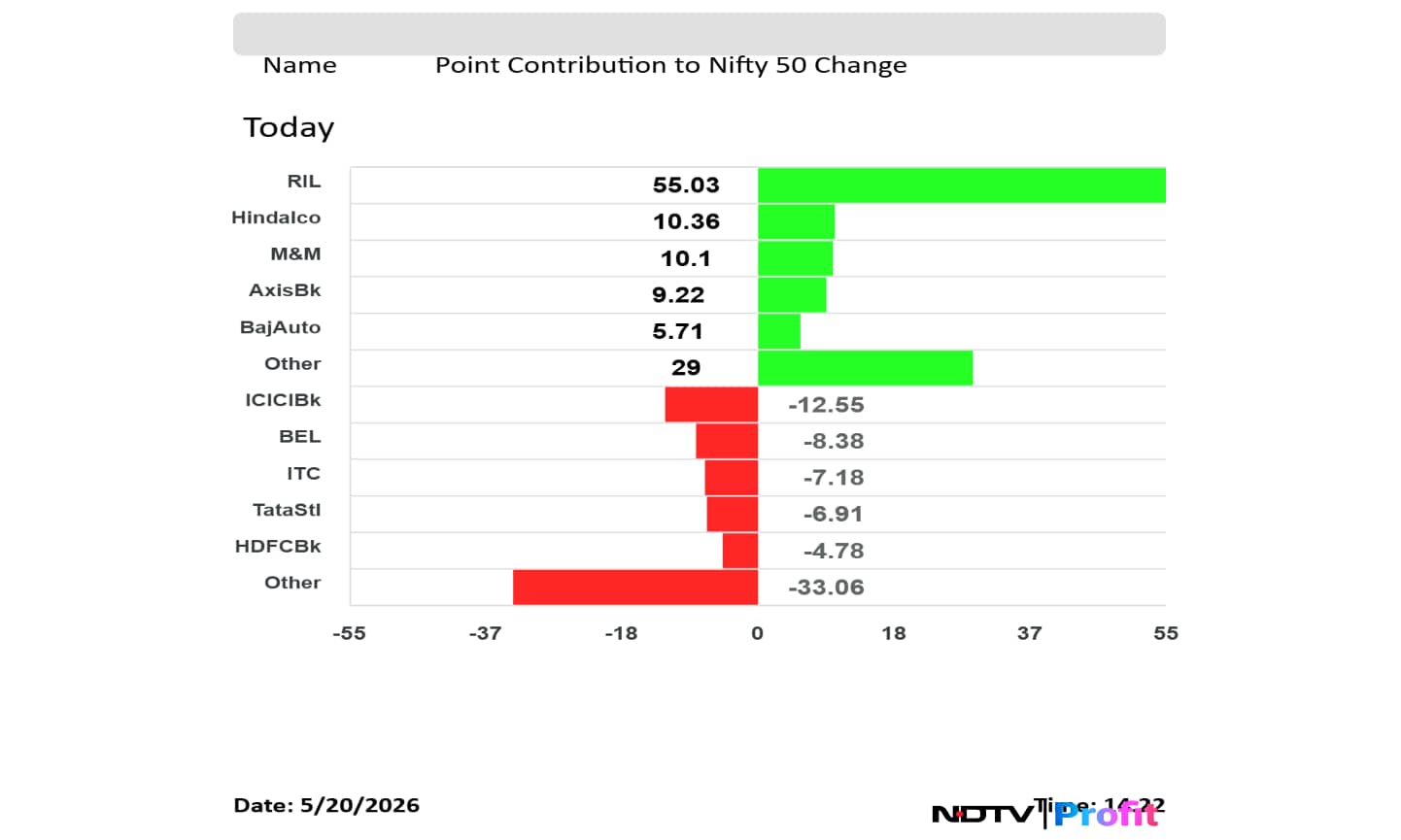

Stock Market Live: Reliance Leads Gains; ICICI Bank, ITC Weigh On Nifty

- Reliance Industries contributed the most to gains, adding 55.03 points to the Nifty

- Hindalco, M&M, Axis Bank and Bajaj Auto also supported the index

ICICI Bank was the top drag, pulling the index down by 12.55 points. ITC, BEL, Tata Steel and HDFC Bank also contributed to losses.

Stock Market Live: European Markets Trade Mixed; FTSE Gains, DAX Slips

- UK’s FTSE 100 and France’s CAC 40 traded higher, while Spain’s IBEX 35 also advanced

- Germany’s DAX edged lower, and STOXX Europe 600 was marginally higher

The moves indicate mixed performance across key European indices in early trade.

Stock Market Live: Asian Markets Close Lower Across Key Indices

- Japan’s Nikkei 225 and South Korea’s Kospi ended lower, reflecting weakness across the region

- Hong Kong’s Hang Seng and Australia’s ASX 200 also closed in the red

- China’s Shanghai Composite declined marginally, extending the downtrend

The broad-based decline across Asian markets indicates continued pressure on regional equities.

Stock Market Live: Akasa Air Signs Deal To Lease Three Boeing Aircraft

- Akasa Air has signed a purchase and leaseback agreement with BOC Aviation for three Boeing 737-8-200 aircraft

- The airline will lease the planes under long-term operating lease agreements

The three aircraft are scheduled for delivery by the end of 2026, according to a press release.

Stock Market Live: Bajaj Finance Allots NCDs Worth Rs 1,025 Crore

Bajaj Finance has allotted non-convertible debentures worth Rs 1,025 crore on a private placement basis, according to an exchange filing.

Stock Market Live: Iran IRGC Warns Of Wider Conflict If Attacked Again

- Iran’s Islamic Revolutionary Guard Corps said any fresh attack could expand the conflict beyond the region

- The statement was reported by Iran’s semi-official Tasnim news agency

The warning signals the risk of escalation in the ongoing tensions, with the IRGC indicating a broader response to any further aggression.

Stock Market Live: CCI Tracks Market Trends, Acts Against Cartelisation, Says CAG

- The Competition Commission of India is keeping pace with evolving market trends, the CAG said

- The regulator continues to take a firm stance against cartelisation across sectors

The CAG added that CCI has helped shift India towards a competitive market system, while work is underway on an AI-based platform for public sector auditing.

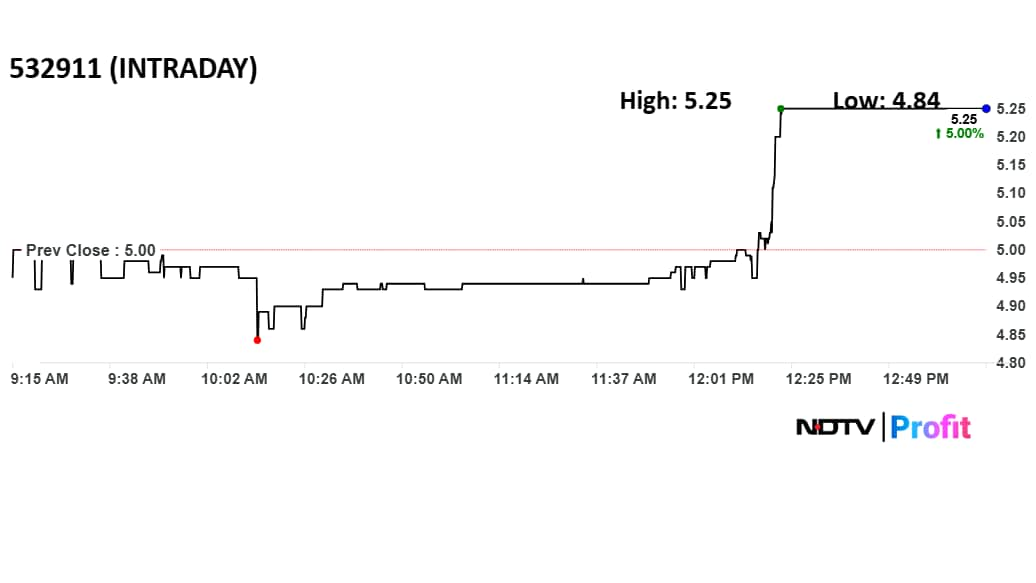

Stock Market Live: Parle Industries Hits Upper Circuit After Modi-Meloni Toffee Moment

- Parle Industries shares rose 5% to Rs 5.25, hitting the upper circuit on the BSE

- The stock moved after Prime Minister Narendra Modi gifted Italian Prime Minister Giorgia Meloni a Melody toffee during his visit

Stock Market Live: Oil & Gas, Energy Lead Gains; Media, FMCG Drag

- Nifty Oil & Gas and Energy indices rose around 1.35% and 1.19%, leading sectoral gains

- Auto and Realty indices also advanced, while Pharma and PSU Bank saw marginal uptick

Media fell 1.26% and FMCG declined 0.85%, with Financial Services, Bank and Metal indices also trading in the red.

Stock Market Live: Mankind Pharma Sees FY27 Margin At 25.5–26.5%

- Mankind Pharma expects FY27 EBITDA margin in the range of 25.5–26.5%

- The company expects double-digit growth in revenue from global operations

It does not plan to launch any new products in FY27, according to Informist.

Stock Market Live: Solfin Sustainable Raises Rs 280 Crore In Private Round

- Solfin Sustainable, backed by Waaree Energies, raised Rs 280 crore in a private round led by HNIs and individual investors

- The funds will be used to expand AI-led credit models, launch new products and scale operations

The NBFC plans to focus on financing rooftop solar and commercial projects, with expansion across Tier 2 and Tier 3 markets.

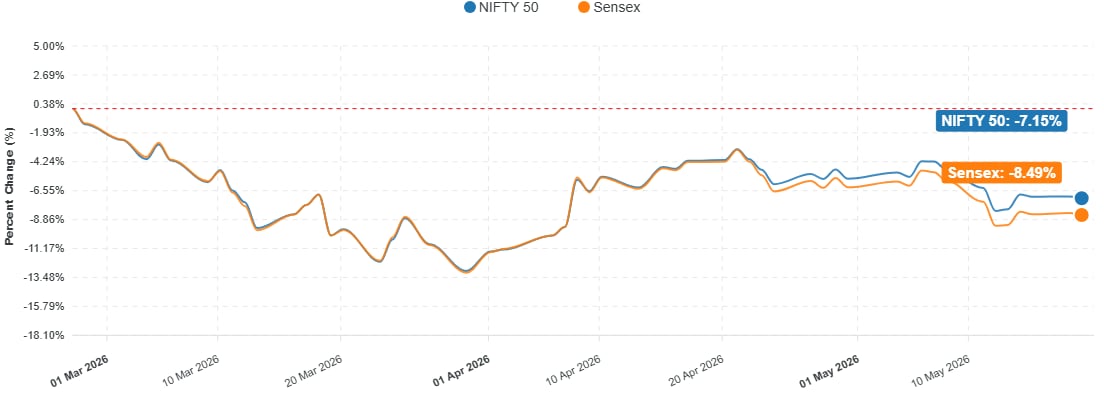

Stock Market Live: Nifty, Sensex Down Up To 8% Since Start Of Middle East Crisis

- Nifty 50 has declined 7.15% since the onset of the Middle East conflict

- Sensex has fallen 8.49% over the same period

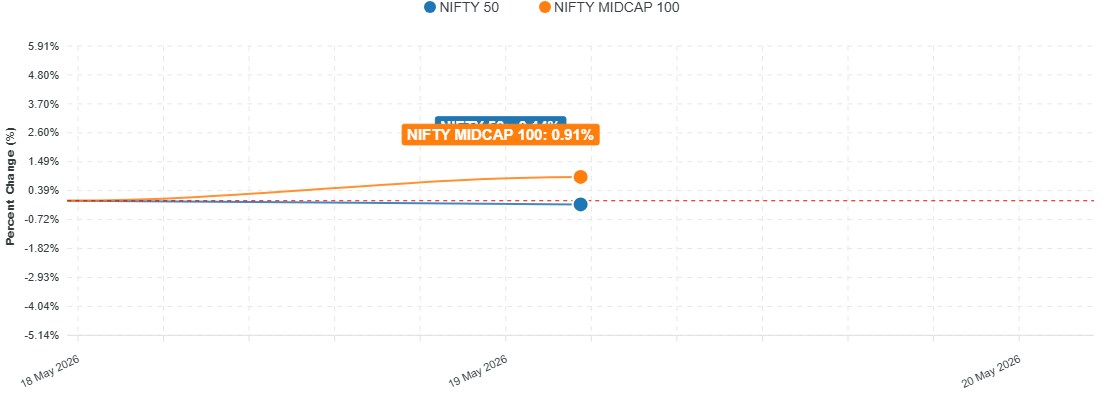

Stock Market Live: Mid-Cap Index Outperforms Nifty

- Nifty Midcap 100 rose 0.91%, outperforming the broader market

- Nifty 50 remained near flat with a marginal decline

Stock Market Live: Emkay Sees Demand Recovery; Expects Better H2 FY27

- Emkay said private banks are trading at 16–20x valuations

- The firm expects the second half of FY27 to be stronger than the first

It noted demand has returned after a gap of six to eight quarters, while IT services trends remained muted in Q4. The brokerage added that earnings in Q4 came in better than expected.

Stock Market Live: RIL, Hindalco Lead Gains; HDFC Bank, ICICI Bank Drag Nifty

- Reliance Industries contributed 35.38 points to the Nifty’s gains, followed by Hindalco at 12.08 points

- Axis Bank, M&M and Bajaj Auto also supported the index

HDFC Bank and ICICI Bank were the top drags, pulling down the index by 17.6 and 15.03 points, respectively. BEL, Tata Steel and Bharti Airtel also weighed on the Nifty.

Stock Market Live: Ester Industries Signs Nike For New JV

- Ester Industries said it has signed Nike as an anchor customer for its new joint venture

- The company plans to increase the share of specialty films in its portfolio

It expects demand for rPET to rise in the coming quarters and anticipates government action on anti-dumping duty for BoPET, with margins dependent on export competition.

Stock Market Live: Nifty, Sensex Near Flat After Recovering From Early Losses

- Nifty traded marginally lower by 0.02% at 23,614.30, while the Sensex slipped 0.06% to 75,152.00.

- Earlier in the session, both indices had fallen as much as 0.9%, with Nifty sliding 220 points and Sensex dropping 671 points before recovering most of the losses.

Stock Market Live: Mankind Pharma Q4 Profit Rises 32%, Margins Expand

- Net profit rose 31.7% to Rs 554 crore, while revenue increased 11.8% to Rs 3,443 crore

- EBITDA jumped 36.1% to Rs 930 crore, with margin expanding to 27% from 22.2%

The performance was supported by domestic growth and an improved product mix. Morgan Stanley maintained an Overweight rating with a target price of Rs 2,500, citing growth in key therapies and operating performance.

Stock Market Live: Andhra Pradesh Approves 2,250 MW Pumped Storage Project For Adani Group

The Andhra Pradesh government has approved allocation of the 2,250 MW Gandikota-2 pumped storage project to an Adani Group entity.

- The project will be developed in YSR Kadapa district under the state’s clean energy policy

- It is aimed at supporting renewable energy storage and balancing power supply

The project is scheduled for completion within 72 months and will use water allocation from the Gandikota reservoir.

Stock Market Live: Zerodha’s Nithin Kamath Flags MTF Risks In Non-F&O Stocks

MTF books are growing across brokers despite the broader markets going nowhere. This isn't like the Korean markets, for example, where the markets are up 150% in the last year alone, and people are borrowing to ride that rally. Our situation is different.

— Nithin Kamath (@Nithin0dha) May 19, 2026

The big risk with MTF… pic.twitter.com/4eGFp3dVMP

Stock Market Live: Kotak AMC Sees Credit Growth Pickup, Cautions On Near-Term Earnings

- Kotak AMC said credit growth for banks has started to increase, while largecap valuations remain more favourable than midcaps

- It expects higher earnings growth for midcaps, but cautioned that earnings may see some impact in the first half of FY27

The fund house highlighted strong demand, pricing and margins supporting chemical companies, with double-digit earnings growth expected in FY27. It advised against aggressive sector calls amid geopolitical shifts, while noting defence exports could benefit from ongoing uncertainty.

Stock Market Live: JSW Steel, Kotak Mahindra Bank See Fresh Bearish Positioning

- JSW Steel and Kotak Mahindra Bank appeared among counters witnessing fresh short build-up.

- The stocks declined during the session while open interest rose.

- Patanjali Foods and InterGlobe Aviation also featured among stocks seeing bearish derivatives positioning.

Stock Market Live: Reliance, Infosys See Short Covering In Futures Segment

- Reliance Industries and Infosys appeared among counters witnessing short covering activity.

- The stocks gained alongside declining open interest levels.

- ONGC and Oil India also featured in the list.

Stock Market Live: KEI Industries, Manappuram Finance Witness Short Covering

- KEI Industries and Manappuram Finance featured among stocks witnessing short covering activity.

- Both counters advanced during the session while open interest declined in futures trade.

- Persistent Systems and Cipla also showed similar trends.

Stock Market Live: Reliance, LIC Housing Finance See Liquidation In Futures Trade

- Reliance Industries and LIC Housing Finance witnessed long unwinding activity in the latest derivatives data.

- The stocks declined alongside lower open interest levels.

- Union Bank of India and Godfrey Phillips India also appeared in the liquidation basket.

Stock Market Live: Federal Bank, Kaynes Technology Witness Long Unwinding Activity

- Federal Bank and Kaynes Technology appeared among counters witnessing liquidation in futures positioning.

- Both stocks declined while open interest also eased during the session.

- NMDC and AU Small Finance Bank also featured in the long unwinding category.

Stock Market Live: Mankind Pharma, OFSS See Fresh Long Additions In Futures Trade

- Mankind Pharma and OFSS featured among stocks witnessing fresh long build-up.

- The counters gained during the session while open interest also increased.

- Tech Mahindra and Zydus Life Sciences additionally showed similar trends.

Stock Market Live: Biocon, Laurus Labs Feature In Long Build-Up List

- Biocon and Laurus Labs appeared among stocks witnessing fresh accumulation activity in futures trade.

- Both counters advanced alongside rising open interest, signalling fresh long positioning.

- Glenmark Pharma and Hindalco Industries also featured in the accumulation basket.

Stock Market Live: PI Industries, Glenmark Pharma See Heavy Derivatives Activity

- PI Industries and Glenmark Pharma recorded sharp increases in Call and Put open interest since the previous expiry.

- PI Industries Put open interest rose more than 748%, while Glenmark Pharma Put open interest climbed over 526%.

- Both counters also saw sizeable total open interest additions.

Stock Market Live: Wipro, Persistent Systems Witness Sharp Derivatives Build-Up

- Wipro and Persistent Systems featured among stocks witnessing strong open interest increases since the previous expiry.

- Wipro total derivatives open interest climbed 174.49%, while Persistent Systems recorded a 114.12% increase.

- PI Industries and Glenmark Pharma also saw elevated positioning activity.

Stock Market Live: Nifty Financial Services Derivatives Open Interest Jumps Over 760%

- Nifty Financial Services recorded one of the sharpest increases in derivatives positioning since the previous expiry cycle.

- Call open interest surged 1,197.45%, while Put open interest climbed 839%.

- Total derivatives open interest rose 769.29%.

Stock Market Live: Nifty 50 Derivatives Open Interest Rises 76% Since Last Expiry

- Nifty 50 total derivatives open interest rose 76.22% since the previous expiry despite the index declining 9.43%.

- Call open interest increased 72.86%, while Put open interest climbed 83.98%.

- The data indicated elevated hedging activity in the derivatives segment.

Stock Market Live: Nifty Bank 54,000 Strike Holds Key Monthly Resistance

- Nifty Bank monthly options positioning showed the 54,000 strike carrying the largest Call open interest base.

- Fresh Call additions also remained strong around the 53,000 strike.

- The 53,500 strike additionally witnessed elevated resistance positioning.

Stock Market Live: Nifty Bank Monthly Options Data Signals Support Near 53,000

- Nifty Bank monthly options data showed the 53,000 strike witnessing the highest Put open interest and fresh Put additions.

- The 52,000 strike also carried elevated Put open interest positioning.

- The data indicated traders continued to defend lower levels around 53,000.

Stock Market Live: Nifty Bank 53,000 Strike Holds Strong Weekly Support

- Nifty Bank weekly options positioning showed the 53,000 strike carrying the highest Put open interest concentration.

- Fresh Put additions also remained elevated at the strike.

- The 52,000 and 52,500 strikes additionally saw sizeable Put positioning.

Stock Market Live: Nifty Bank 53,000 Strike Emerges As Key Weekly Resistance

- Nifty Bank weekly options data showed aggressive Call additions at the 53,000 strike.

- The strike also carried one of the highest Call open interest bases for the weekly series.

- The 54,000 strike additionally witnessed elevated Call positioning.

Stock Market Live: Nifty 24,000 Strike Remains Key Monthly Resistance

- Nifty monthly options positioning showed the 24,000 strike holding the largest Call open interest base.

- Fresh Call additions were also visible at the 23,500 and 23,800 strikes.

- The 24,500 strike additionally carried sizeable Call open interest positioning.

Stock Market Live: Nifty Monthly Options Data Signals Support Near 23,500

- Nifty monthly options data showed the 23,500 strike witnessing the strongest Put additions and highest Put open interest.

- The 23,400 strike also saw notable Put accumulation.

- The positioning indicated support expectations remained concentrated around the 23,400–23,500 zone.

Stock Market Live: Nifty 23,500 Strike Emerges As Key Weekly Support Zone

- Nifty weekly options data showed aggressive Put additions at the 23,500 strike.

- The strike also carried the highest Put open interest concentration, indicating traders were defending the zone as immediate support.

- The 23,400 and 23,300 strikes additionally witnessed sizeable Put build-up.

F&O Hour Is Here

Key levels, active strikes, big moves and live market cues — all in one place; Join our F&O Hour live blog for real-time action now.

Stock Market Live: Nifty 24,000 Strike Holds Strong Weekly Resistance

- Nifty weekly options positioning showed the 24,000 strike carrying the largest Call open interest base.

- Fresh Call writing was also visible at 23,500 and 23,800 strikes.

- The data indicated traders were placing resistance expectations around the 24,000 zone.

Stock Market Live: Nifty, Sensex Recover From Opening Lows But Stay Lower

Nifty traded 0.31% lower at 23,543.70, while the Sensex was down 0.46% at 74,857.33 in early trade.

During the opening session, the Nifty fell as much as 0.9%, or 220 points, to 23,397.30. The Sensex dropped as much as 0.9%, or 671.44 points, to 74,529.

Stock Market Live: Amagi Media Q4 Profit Rises 4% Sequentially, Revenue Falls

- Amagi Media’s net profit rose 4.2% quarter-on-quarter to Rs 19.7 crore, while revenue declined 5% to Rs 249 crore.

- The company reported an EBITDA loss of Rs 3.4 crore in Q4, compared with an EBITDA profit of Rs 7.6 crore in the previous quarter.

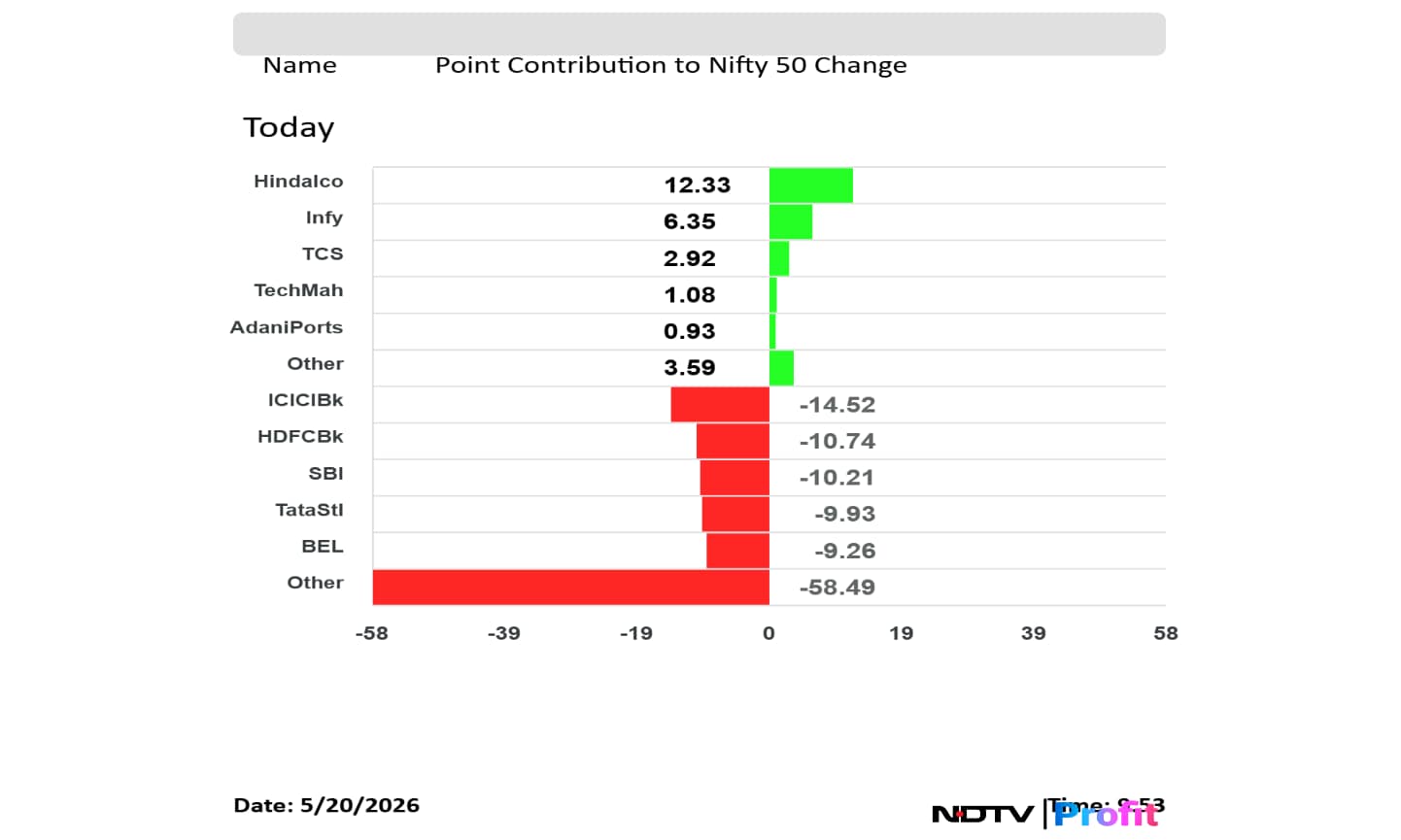

Stock Market Live: Banks, SBI And BEL Drag Nifty; Hindalco Limits Losses

- ICICI Bank, HDFC Bank, SBI, Tata Steel and BEL were among the top drags on the Nifty 50

- Hindalco added 12.33 points, while Infosys contributed 6.35 points to the index

ICICI Bank had the largest negative contribution among listed stocks at 14.52 points, followed by HDFC Bank at 10.74 points and SBI at 10.21 points.

Stock Market Live: Morgan Stanley Sees Short-Term Upside In TVS Motor

Morgan Stanley maintained an Overweight rating on TVS Motor with a target price of Rs 4,327 and issued a tactical Buy call.

The brokerage expects the stock to rise over the next 30 days, citing the company’s buyback plan, past record and upcoming triggers. It said TVS Motor’s two-wheeler volumes rose 9.5% year-on-year in the first 19 days of May, ahead of the industry’s 6% growth.

Stock Market Live: India Prepares To Send Oil Tankers Through Hormuz For Middle East Supply

India is preparing to send vessels through the Strait of Hormuz to load energy cargoes from Middle East suppliers, according to Bloomberg.

State-owned Shipping Corp. of India is ready to return to the Persian Gulf once it gets approval from the Indian Navy and business from oil refiners. India wants to continue sourcing energy from traditional Middle East suppliers as alternate routes may take longer and cost more.

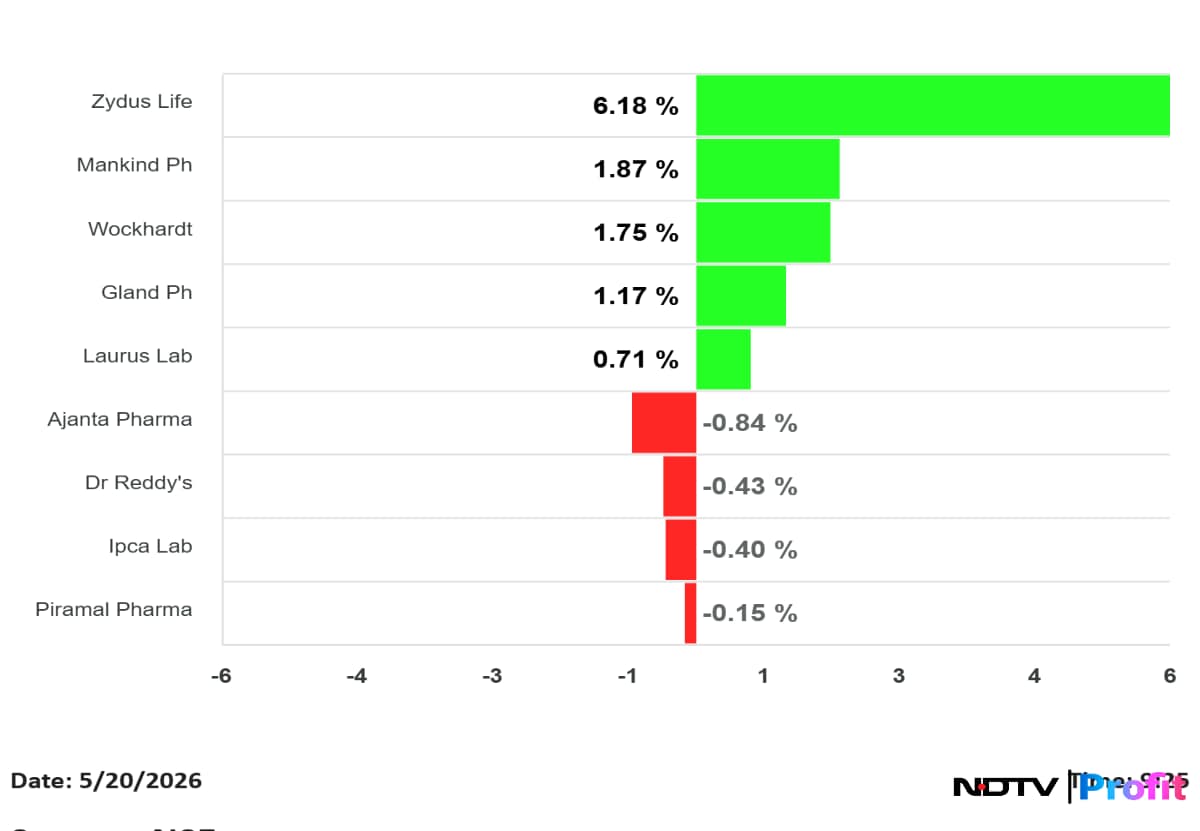

Stock Market Live: Zydus Life Leads Pharma Gains; Ajanta Pharma Falls

- Zydus Life rose 6.18%, while Mankind Pharma gained 1.87%

- Wockhardt, Gland Pharma and Laurus Labs also traded higher, with gains of up to 1.75%

Ajanta Pharma, Dr Reddy’s, Ipca Labs and Piramal Pharma traded lower, with Ajanta Pharma down 0.84%.

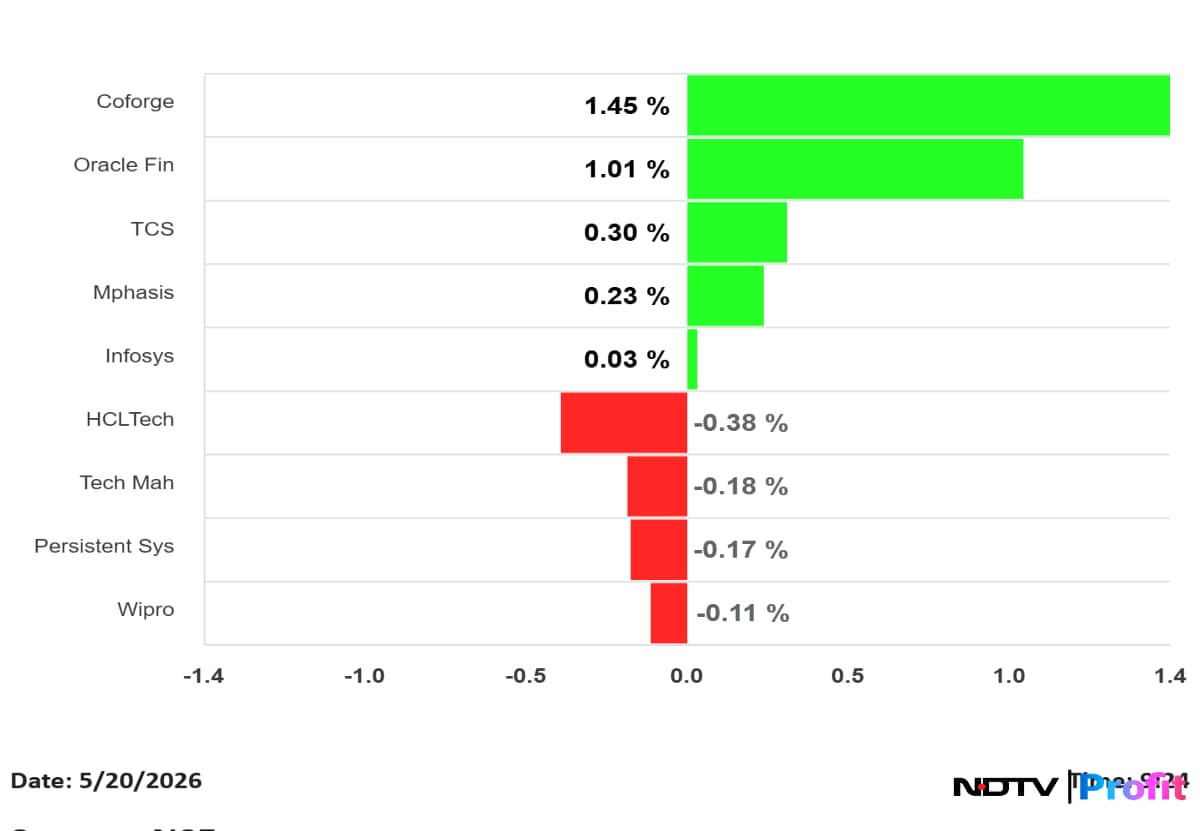

Stock Market Live: IT Stocks Trade Mixed; Coforge, Oracle Financial Gain

- Coforge rose 1.45%, while Oracle Financial Services gained 1.01%

- TCS, Mphasis and Infosys also traded higher, with gains of up to 0.30%

HCLTech, Tech Mahindra, Persistent Systems and Wipro traded lower, with HCLTech down 0.38%.

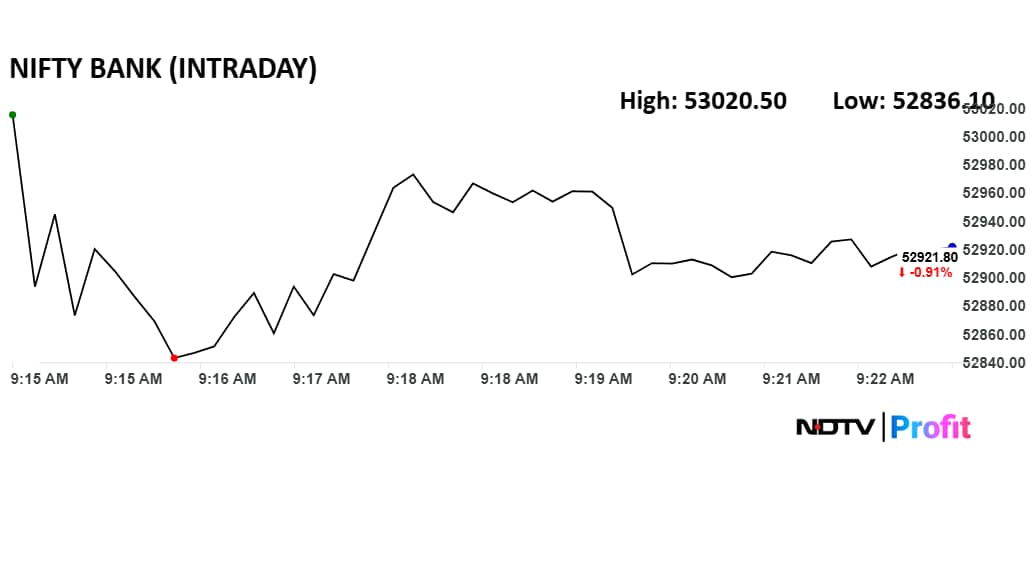

Stock Market Live: Nifty Bank Falls 0.9% In Early Trade

Nifty Bank traded 0.91% lower at 52,921.80 in early trade. The index moved between an intraday high of 53,020.50 and a low of 52,836.10.

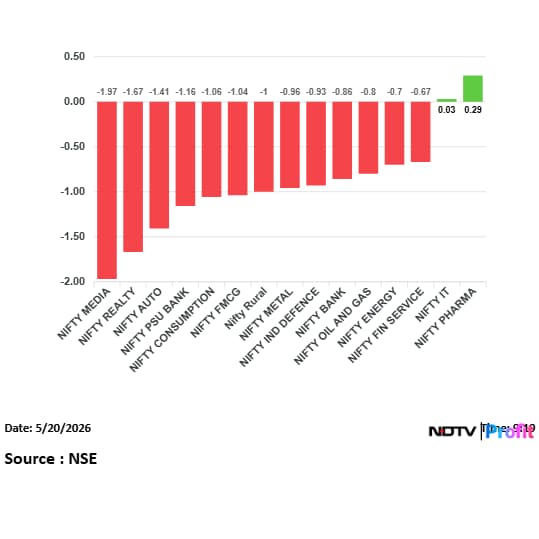

Stock Market Live: Pharma, IT Hold Gains While Most Sectoral Indices Decline

- Nifty Pharma rose 0.29% and Nifty IT edged up 0.03%

- All other sectoral indices traded lower, led by Nifty Media down 1.97% and Realty down 1.67%

Auto, PSU Bank, Consumption and Metal indices also saw declines of over 1%, reflecting broad-based weakness across sectors.

Stock Market Live: Nifty Falls 0.9% To 23,397; Sensex Drops 671 Points

- Indian equity benchmarks declined, tracking losses in Asian markets and overnight weakness on Wall Street.

- Nifty fell as much as 0.9% or 220 points to 23,397.30.

- Sensex slipped 0.9% or 671.44 points to 74,529, indicating broad-based selling across markets.

Stock Market Live: Rupee Hits Record Low Of 96.93 Against US Dollar

- Rupee weakened to a fresh record low, depreciating as much as 40 paise to 96.93 against the US dollar.

- The sharp fall reflects continued pressure on the domestic currency in early trade.

Stock Market Live: Nifty Below 23,400 In Pre-Open; Sensex Down 500 Points

- Nifty slipped below the 23,400 mark in pre-open trade, indicating a weak start for the session.

- Sensex declined around 500 points in early signals, pointing to broad-based pressure at the open.

Stock Market Live: Govt Reviews Startup Fund Strategy To Boost Innovation

Commerce Minister Piyush Goyal chaired a review meeting on Startup India Fund of Funds 1.0 and 2.0 to assess support measures for startups.

- Discussions focused on funding access, deep-tech and manufacturing startups, and private sector participation

- The review also covered steps to strengthen institutional support and promote growth in Tier 2 and Tier 3 cities

The government also discussed enhancing long-term capital availability and supporting sectors linked to technology and economic growth.

Stock Market Live: Australian Dollar Falls As Yield Gap With US Narrows

- The Australian dollar declined 0.7% this week to around 71 US cents

- The drop comes as the yield gap between Australian and US bonds narrows

The currency faced pressure amid a global bond sell-off and concerns over interest rates staying elevated. Rising tensions in the Middle East have also added to uncertainty, weighing on sentiment.

Stock Market Live: Brent Crude Slips Amid Uncertainty Over US Action On Iran

- Brent crude fell below $111 per barrel, while WTI traded under $104

- Prices declined alongside Asian equities as markets weighed fresh US comments on Iran

US President Donald Trump renewed the possibility of strikes on Iran but had earlier said an attack was called off. The mixed signals have kept traders cautious on further price movement.

Stock Market Live: BEL Q4 Profit Rises 4.7%, Board Recommends Dividend

- Net profit rose 4.7% to Rs 2,226 crore, while revenue increased 11.7% to Rs 10,224 crore

- EBITDA grew 5.9% to Rs 2,982 crore, but margin narrowed to 29.2% from 30.8%

The company’s order book stood at Rs 73,882 crore. The board recommended a final dividend of Rs 0.55 per share, while cash equivalents increased to Rs 1,888 crore.

Stock Market Live: Focus On US-Iran Developments, Says Cameron Brandt

- Market attention remains on developments in the US-Iran conflict

- The US is seen playing its traditional role as a safe-haven market

Investors are focusing more on individual markets rather than broader regional exposure.

Stock Market Live: Citi Raises Ajax Engineering Target To Rs 680, Maintains Buy

- Citi maintained a Buy rating on Ajax Engineering and raised the target price to Rs 680 from Rs 600

- The brokerage said Q4 performance was driven by pricing discipline and stable market share

The company increased prices by 2% in Q4 and aims to sustain EBITDA margins in the 13–15% range. Demand is seen supported by infrastructure spending and mechanised construction, with potential M&A activity in the second half.

Stock Market Live: Citi Sees ICICI Bank Growth, Maintains Buy With Rs 1,720 Target

- Citi maintained a Buy rating on ICICI Bank with a target price of Rs 1,720

- The brokerage highlighted broad-based growth led by retail, with corporate lending supported by a shift from bond markets to banks

Citi expects margins to remain range-bound with higher deposit costs, while the West Asia situation has not led to portfolio stress. The bank has tightened credit filters in select sectors, with operating costs seen growing slower than revenue and credit costs expected to rise marginally.

Stock Market Live: Citi Sees Axis Bank Growth, Maintains Buy With Rs 1,620 Target

- Citi maintained a Buy rating on Axis Bank with a target price of Rs 1,620

- The brokerage said there is no visible impact from the West Asia situation on growth or asset quality

Axis Bank is seen maintaining a disciplined growth approach, with buffers in place for adverse scenarios. Citi expects near-term margin pressure due to mix changes but sees positive operating leverage in FY27 and gradual improvement in efficiency metrics.

Stock Market Live: Brokerages Maintain Positive View On Zydus Life, Raise Targets

- Macquarie maintained an Outperform rating with a target of Rs 1,110 and raised its FY28 earnings estimate

- Jefferies maintained Buy and increased its target price to Rs 1,200 from Rs 1,100

The brokerages cited performance across key markets and new product opportunities, with expectations of growth supported by upcoming launches and portfolio expansion.

Stock Market Live: Citi Keeps Hindalco Neutral; Sees FCF By FY27

- Citi maintained a Neutral rating on Hindalco with a target price of Rs 1,000

- The brokerage expects positive free cash flow by end-FY27, supported by project progress and business momentum

Cost savings in FY26 crossed $125 million, above earlier guidance. The Oswego restart is expected within weeks, ahead of the end-June FY26 timeline.

Stock Market Live: Nomura Initiates Avalon Technologies With Buy Rating, Sets Rs 1,722 Target

- Nomura has initiated coverage on Avalon Technologies with a Buy rating and a target price of Rs 1,722

- The brokerage expects demand from sectors such as AI, HVDC and semiconductors to support growth

Management aims to double revenue between FY26 and FY29. Nomura expects revenue and earnings growth over the period, supported by margin improvement and execution.

Stock Market Live: EM Gains Led By Korea, Taiwan, Says Geoffrey Dennis

- Korea and Taiwan account for the gains seen in emerging markets so far this year

- No immediate impact is expected from NATO involvement in the Hormuz region

Oil prices may take time to ease, while the reopening of the Hormuz route remains a key factor after any potential deal. Dennis added that market participants are unlikely to accept claims of peace quickly.

Iran Warns 'Return To War Will Feature Many More Surprises,' Cites US Report On Aircraft Losses

Stock Market Live: PI Industries Q4 Profit Falls 39%, EBITDA Misses Estimates

- Revenue fell 12.4% to Rs 1,565 crore, while EBITDA declined 26.1% to Rs 337 crore

- Net profit dropped 39.4% to Rs 200 crore; EBITDA margin narrowed to 21.5% from 25.5%

The company said performance was affected by delivery schedules, weak exports and domestic softness, with pressure from high inventory and lower volumes. EBITDA also came in below estimates, continuing a trend of misses in recent quarters.

Stock Market Live: Meta Cuts Jobs In AI-Led Efficiency Drive

- Meta has begun laying off around 8,000 employees globally as part of an efficiency push led by AI

- The cuts are expected to impact product and engineering teams

Staff have been asked to work from home during the process, with further layoffs possible later this year.

Stock Market Live: Q4 Results Announced After Market Hours

WPIL (Q4, Consolidated YoY)

-

Revenue down 10.6% to Rs 511 crore versus Rs 572 crore.

-

Ebitda down 4.7% to Rs 76.2 crore versus Rs 79.9 crore.

-

Margin at 14.9% versus 14.0%.

-

Net profit up 2,208.6% to Rs 40.4 crore versus Rs 1.75 crore.

-

Company recorded Rs 70.5 crore tax on discontinued operations in Q4 FY25.

Novelis (Q4, Consolidated YoY)

-

Revenue up 4.4% to $4,787 million versus $4,587 million.

-

Adjusted Ebitda down 3% to $459 million.

-

Net loss at $84 million versus profit of $294 million.

-

Oswego Hot Mill expected to resume operations in a few weeks.

PNC Infratech (Q4, Consolidated YoY)

-

Revenue down 5.1% to Rs 1,617 crore versus Rs 1,704 crore.

-

Ebitda down 23.5% to Rs 277 crore versus Rs 362 crore.

-

Margin at 17.1% versus 21.3%.

-

Net profit up 42.1% to Rs 108 crore versus Rs 76 crore.

-

MD Chakresh Kumar Jain appointed as CFO.

Orkla India (Q4, Consolidated YoY)

-

Revenue up 5% to Rs 626 crore versus Rs 596 crore.

-

Ebitda up 2% to Rs 97.3 crore versus Rs 95.4 crore.

-

Margin at 15.5% versus 16%.

-

Net profit up 108.5% to Rs 73.4 crore versus Rs 35.2 crore.

Prince Pipes (Q4, YoY)

-

Revenue up 18.1% to Rs 850 crore versus Rs 720 crore.

-

Ebitda up 100.9% to Rs 109.7 crore versus Rs 54.6 crore.

-

Margin at 12.9% versus 7.6%.

-

Net profit up 131.8% to Rs 56.1 crore versus Rs 24.2 crore.

Bosch Home Comfort (Q4, YoY)

-

Revenue up 3.5% to Rs 965.4 crore versus Rs 932.6 crore.

-

Ebitda down 26.1% to Rs 67.8 crore versus Rs 91.7 crore.

-

Margin at 7% versus 9.8%.

-

Net profit down 27.1% to Rs 40.9 crore versus Rs 56.1 crore.

-

Marcel Heese appointed Chairperson from July 1; Sanjay Sudhakaran reappointed as MD.

Zee Entertainment (Q4, Consolidated YoY)

-

Revenue down 7.3% to Rs 2,025 crore versus Rs 2,184 crore.

-

Ebitda loss at Rs 255 crore versus profit of Rs 298 crore.

-

Net loss at Rs 102.4 crore versus profit of Rs 188.4 crore.

-

Board declared dividend of Rs 2/share.

Trident (Q4, Consolidated YoY)

-

Revenue down 12.4% to Rs 1,633 crore versus Rs 1,864 crore.

-

Ebitda down 2.1% to Rs 242.2 crore versus Rs 247.4 crore.

-

Margin at 14.8% versus 13.3%.

-

Net profit down 23.5% to Rs 102 crore versus Rs 133.3 crore.

-

Deepak Nanda reappointed as MD for three years.

-

Board approved raising up to Rs 500 crore via NCDs.

Hatsun Agro (Q4, YoY)

-

Revenue up 14.9% to Rs 2,578 crore versus Rs 2,243 crore.

-

Ebitda up 4.8% to Rs 235.3 crore versus Rs 224.5 crore.

-

Margin at 9.1% versus 10%.

-

Net profit up 18.6% to Rs 51 crore versus Rs 43 crore.

-

Board declared interim dividend of Rs 10/share.

Godawari Power (Q4, Consolidated YoY)

-

Revenue up 9.7% to Rs 1,610 crore versus Rs 1,468 crore.

-

Ebitda up 38.1% to Rs 439 crore versus Rs 318 crore.

-

Margin at 27.3% versus 21.7%.

-

Net profit up 26.7% to Rs 280 crore versus Rs 221 crore.

-

Plans loan of up to Rs 150 crore to GERF and additional Rs 200 crore investment in Godawari New Energy.

Nephrocare Health (Q4, Consolidated YoY)

-

Revenue up 21.5% to Rs 266 crore versus Rs 219 crore.

-

Ebitda up 4.3% to Rs 53.6 crore versus Rs 51.4 crore.

-

Margin at 20.2% versus 23.4%.

-

Net profit up 22.1% to Rs 30.4 crore versus Rs 24.9 crore.

ASK Automotive (Q4, Consolidated YoY)

-

Revenue up 35% to Rs 1,147 crore versus Rs 850 crore.

-

Ebitda up 28.4% to Rs 133.3 crore versus Rs 103.8 crore.

-

Margin at 11.6% versus 12.2%.

-

Net profit up 24.1% to Rs 71.5 crore versus Rs 57.6 crore.

BPCL (Q4, QoQ)

-

Revenue down 0.3% to Rs 1.18 lakh crore versus Rs 1.19 lakh crore.

-

Ebitda down 13.8% to Rs 10,061 crore versus Rs 11,677 crore.

-

Margin at 8.5% versus 9.8%.

-

Net profit down 57.7% to Rs 3,191 crore versus Rs 7,545 crore.

-

One-time loss stood at Rs 4,349 crore in Q4.

Dredging Corp (Q4, YoY)

-

Revenue up 73.2% to Rs 478.2 crore versus Rs 276.1 crore.

-

Ebitda up 334.7% to Rs 143 crore versus Rs 32.9 crore.

-

Margin at 29.9% versus 11%.

-

Net profit at Rs 86.9 crore versus loss of Rs 24.6 crore.

PTC India (Q4, Consolidated YoY)

-

Revenue up 33.3% to Rs 3,898 crore versus Rs 2,924 crore.

-

Ebitda down 6.9% to Rs 145 crore versus Rs 156 crore.

-

Margin at 3.7% versus 5.3%.

-

Net profit down 69.4% to Rs 105 crore versus Rs 343 crore.

-

Board declared final dividend of Rs 5.50/share.

-

Company to consider monetising stake in PTC India Financial Services.

Anthem Biosciences (Q4, Consolidated YoY)

-

Revenue up 26.5% to Rs 611 crore versus Rs 483 crore.

-

Ebitda up 36.9% to Rs 267 crore versus Rs 195 crore.

-

Margin at 43.7% versus 40.4%.

-

Net profit up 129.8% to Rs 189.8 crore versus Rs 82.6 crore.

-

Board declared final dividend of Rs 2/share.

Mankind Pharma (Q4, Consolidated YoY)

-

Revenue up 11.8% to Rs 3,443 crore versus Rs 3,079 crore.

-

Ebitda up 36.2% to Rs 930 crore versus Rs 683 crore.

-

Margin at 27% versus 22.2%.

-

Net profit up 31.6% to Rs 554 crore versus Rs 421 crore.

-

Satish Kumar Sharma appointed Whole-Time Director for five years.

-

Company to invest additional Rs 500 crore in Mankind Medicare.

Karnataka Bank (Q4, YoY)

-

NII up 8% to Rs 843 crore versus Rs 781 crore.

-

Operating profit up 64% to Rs 615 crore versus Rs 375 crore.

-

Net profit up 61.9% to Rs 408 crore versus Rs 252 crore.

-

Gross NPA improved to 2.78% versus 3.32% QoQ.

-

Net NPA improved to 0.98% versus 1.31% QoQ.

-

Provisions down 4.8% to Rs 90.3 crore versus Rs 94.9 crore QoQ.

-

Board declared final dividend of Rs 5/share.

Automotive Axles (Q4, YoY)

-

Revenue up 18.6% to Rs 664 crore versus Rs 560 crore.

-

Ebitda up 23.2% to Rs 77.1 crore versus Rs 62.6 crore.

-

Margin at 11.6% versus 11.2%.

-

Net profit up 17.4% to Rs 53.9 crore versus Rs 45.9 crore.

-

Board declared final dividend of Rs 32/share; record date set as August 5.

Hindware Home Innovation (Q4, Consolidated YoY)

-

Revenue down 5.2% to Rs 663 crore versus Rs 699 crore.

-

Ebitda up 8.1% to Rs 44.2 crore versus Rs 40.9 crore.

-

Margin at 6.7%.

-

Net loss at Rs 19 crore versus loss of Rs 31 crore.

Viyash Scientific (Q4, Consolidated YoY)

-

Revenue up 19.2% to Rs 920 crore versus Rs 772 crore.

-

Ebitda up 62.8% to Rs 184 crore versus Rs 113 crore.

-

Margin at 20% versus 14.6%.

-

Net profit at Rs 52.1 crore versus loss of Rs 26.2 crore.

-

One-time cost stood at Rs 7 crore in Q4.

CE Info Systems (Q4, Consolidated QoQ)

-

Revenue up 54.7% to Rs 145 crore versus Rs 93.7 crore.

-

EBIT up 197.9% to Rs 56.9 crore versus Rs 19.1 crore.

-

EBIT margin at 39.2% versus 20.4%.

-

Net profit up 170.2% to Rs 50.8 crore versus Rs 18.8 crore.

-

Board declared final dividend of Rs 3.50/share.

Dynamatic Tech (Q4, Consolidated YoY)

-

Revenue up 13.6% to Rs 433 crore versus Rs 381 crore.

-

Ebitda up 28.2% to Rs 48.6 crore versus Rs 37.9 crore.

-

Margin at 11.2% versus 10%.

-

Net profit down 21.7% to Rs 12.6 crore versus Rs 16.1 crore.

-

Board declared interim dividend of Rs 5/share.

Borosil (Q4, Consolidated YoY)

-

Revenue up 5.2% to Rs 284 crore versus Rs 270 crore.

-

Ebitda down 18.8% to Rs 30.2 crore versus Rs 37.2 crore.

-

Margin at 10.6% versus 13.8%.

-

Net profit down 4.5% to Rs 10.6 crore versus Rs 11.1 crore.

-

Board approved raising up to Rs 250 crore via QIP and other routes.

Siyaram Silk Mills (Q4, Consolidated YoY)

-

Revenue up 15.9% to Rs 853 crore versus Rs 736 crore.

-

Ebitda up 23.4% to Rs 137 crore versus Rs 111 crore.

-

Margin at 16% versus 15.1%.

-

Net profit up 35.8% to Rs 97.8 crore versus Rs 72.04 crore.

-

Board declared special dividend of Rs 4/share and final dividend of Rs 5/share.

Fine Organic (Q4, Consolidated YoY)

-

Revenue up 3% to Rs 625 crore versus Rs 607 crore.

-

Ebitda up 8.3% to Rs 130 crore versus Rs 120 crore.

-

Margin at 20.8% versus 19.7%.

-

Net profit up 21% to Rs 117.5 crore versus Rs 97.1 crore.

-

Board declared final dividend of Rs 11/share.

-

Company to acquire 80% stake in Oleofine Organics.

Stock Market Live: Kaynes, SAIL Under F&O Ban

- Kaynes Technology India and SAIL are in the F&O ban period

- Trading in their derivative contracts is restricted as they have crossed market-wide position limits.

Stock Market Live: Nine Stocks Removed From ASM Framework

- Avalon Technologies, Awfis Space Solutions, Bhagiradha Chemicals & Industries and Exicom Tele-Systems have been excluded from the ASM framework

- Firstsource Solutions, Marine Electricals (India), Neogen Chemicals, Simplex Infrastructures and Venus Pipes & Tubes are also removed

Stock Market Live: Four Stocks Placed Under Short-Term ASM Framework

- Balaji Amines, Kaynes Technology India, Rane Holdings and Wheels India have been shortlisted under the short-term ASM framework

Stock Market Live: Paisalo Promoters Buy Shares; Afcons Promoter Pledges Stake

- Promoter group entities in Paisalo Digital acquired a total of 21 lakh shares

- Afcons Infrastructure’s promoter, Goswami Infratech, created a pledge on 22.05 crore shares

Stock Market Live: Stocks In Focus On Deals, Regulatory Actions And Corporate Updates

-

ITC Hotels acquired 100% stake in Zuri Hotels for Rs 205 crore; ITC bought 49.3% in Mother Sparsh for Rs 30 crore; Wipro completed acquisition of Olam’s IT arm

-

PG Electroplast received SEBI warning on insider norms; IndusInd Bank denied reports of SEBI summons; Paradeep Phosphates’ tax relief plea rejected by NCLAT

-

JSW Energy to buy 10.7% in Toshiba JSW Power for Rs 150 crore; M&M Financial approved Rs 2,200 crore NCD issue; Omaxe secured Rs 75 crore investment

-

Sula Vineyards announced CFO change; Puravankara named new CTO; IDBI Bank reappointed Deputy MD for one year

-

Mphasis saw release of pledge on 30.55% shares; Zee Entertainment to invest up to Rs 100 crore in arm; Aditya Birla Capital received RBI nod for factoring business

-

Bharti Airtel launched new 5G postpaid plans; United Breweries launched Heineken Silver in Haryana; Nibe completed rocket system test firing

-

Mangalore Refinery received approval for ATF pipeline; Blue Star to acquire remaining stake in Qatar arm; Sundry updates include investments, approvals and subsidiary expansions across firms

Stock Market Live: Weak Start Seen As Global Cues Stay Negative

- Asian equities declined as global bond yields continued to rise

- Oil prices held firm, while gold remained under pressure

- US futures traded steady ahead of Nvidia earnings

Foreign institutional investors turned sellers in the cash market after three sessions, with short positions unchanged at 88%. The rupee is seen under pressure, while technical indicators point to a weak setup.

Stock Market Live: US Futures Edge Higher Across Major Indices

- S&P 500 futures rose 0.14% and Nasdaq 100 futures gained 0.25%

- Dow Jones futures advanced 55 points, or 0.11%

Stock Market Live: US 30-Year Bond Yield Hits Nearly 19-Year High

- US Treasury yields rose as investors sold bonds amid concerns over inflation

- The 30-year yield briefly touched 5.197%, its highest level since July 2007

It was last trading at 5.174%, slightly lower during the session.

Stock Market Live: GIFT Nifty Indicates Lower Start For Nifty 50

GIFT Nifty traded at 23,467.50, below the previous close of the Nifty 50 at 23,618, indicating a weaker start for domestic markets.

Stock Market Live: Asian Markets Decline; Hang Seng Futures Signal Lower Open

- Japan’s Nikkei 225 fell 0.88% and the Topix declined 0.75%

- South Korea’s Kospi slipped 0.52%, while the Kosdaq dropped 2.15%

- Australia’s S&P/ASX 200 lost 0.5%

Hong Kong’s Hang Seng index futures stood at 25,603, below the previous close of 25,797.85, indicating a weaker start.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.