Scan to Download

Indian benchmark indices closed sharply lower on Tuesday, extending their longest losing streak since the second week of January, as weakness in global markets triggered broad-based selling across sectors.

The NSE Nifty 50 fell 1.83% to close at 23,579.55, while the BSE Sensex declined 1.92% to 74,559.24. The decline marked the steepest single-day fall for the benchmarks since March 30.

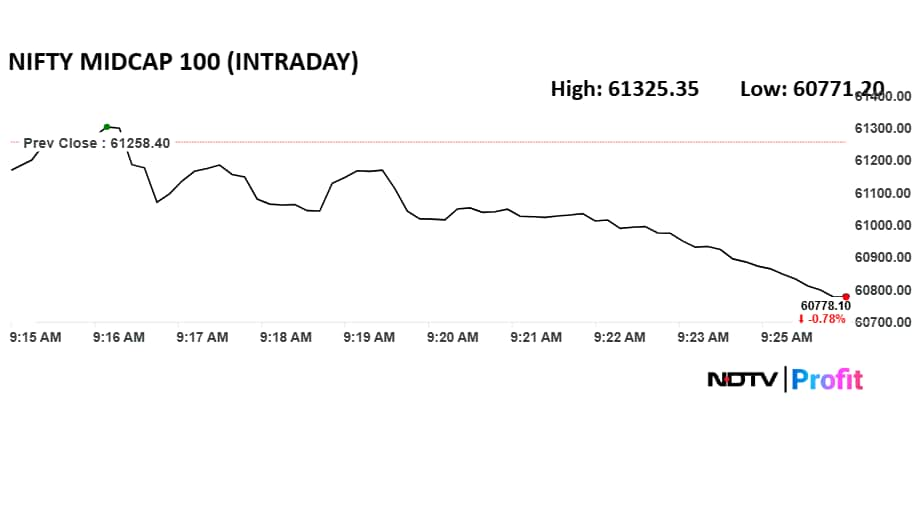

The sell-off spread across the broader market, with mid-cap and small-cap indices underperforming the headline gauges. The Nifty Midcap 150 declined for the third straight session, while the Nifty Smallcap 250 extended losses for a second day. Both indices ended more than 2.5% lower.

UPL and Dixon Technologies were the top losers on the mic-cap index. Sonata Software and GSPL led declines among small-cap stocks.

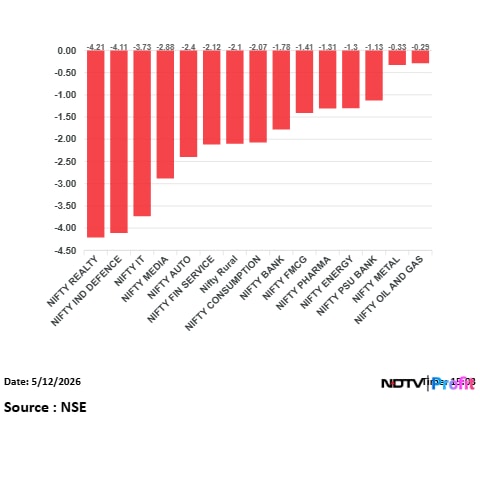

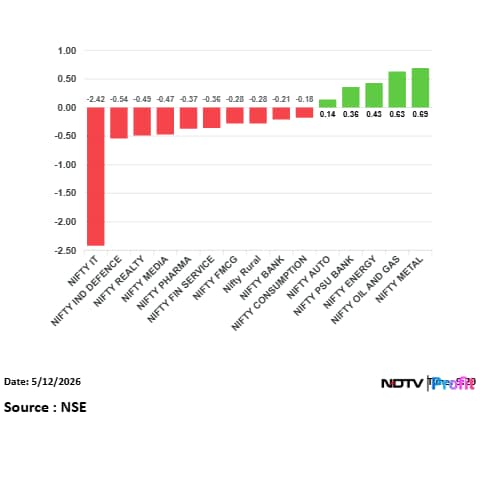

Nifty Realty and Nifty IT were the worst performers, with both indices falling more than 3.5%. Realty extended losses for a third consecutive session, while IT declined for a second straight day. Auto, Financial Services, Bank, Energy and Metal indices also continued their losing streaks. FMCG, meanwhile, snapped a two-day gaining run.

The sharp fall in domestic equities came amid rising concerns over global markets and crude oil prices after comments from US President Donald Trump on the Iran situation. Trump said the ceasefire with Iran was "on life support" after Tehran rejected a counterproposal, raising concerns that tensions in the Middle East could continue.

Brent crude futures for July rose 2.43% to $106.74 a barrel, while US West Texas Intermediate futures for June climbed 2.91% to $100.92 per barrel.

US equity futures also traded lower. S&P 500 futures slipped 0.38%, while Nasdaq 100 futures declined 0.73%. Dow Jones Industrial Average futures were down 55 points, or 0.11%, indicating a weaker start for Wall Street.

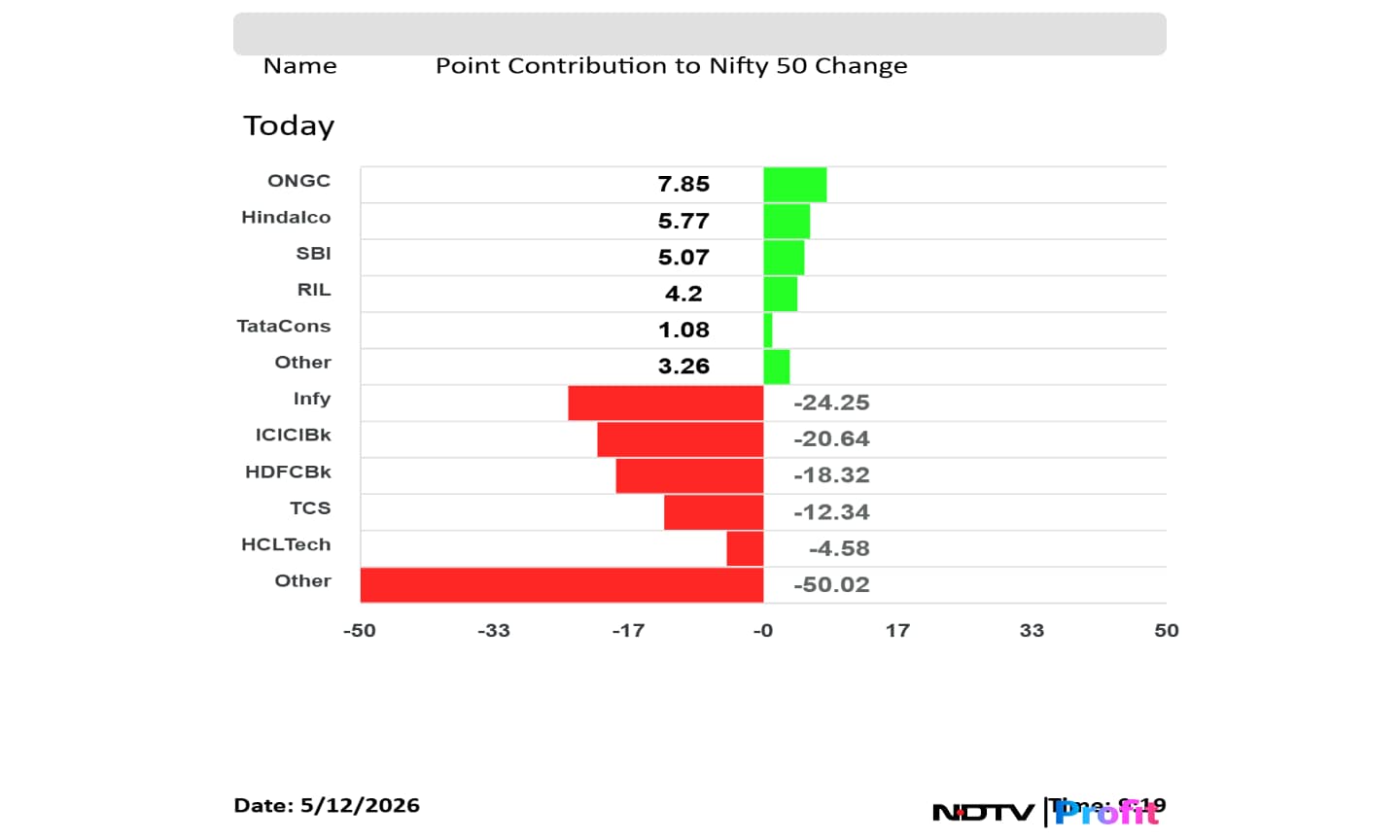

The Nifty 50 closed down over 1.8%, ending its fourth straight session in the red and settling below the 23,400 mark. Forty‑seven of the 50 Nifty stocks ended lower, with 38 stocks declining more than 1%. Shriram Finance and Tech Mahindra were the top losers on the index, both falling over 4%.

The broader market underperformed the benchmarks. The Nifty Midcap 150 fell for the third consecutive session, while the Nifty Smallcap 250 declined for the second day in a row, with both indices ending down over 2.5%. UPL and Dixon Technologies led losses in the Midcap index, while Sonata Software and GSPL were the biggest laggards among smallcaps.

All sectoral indices closed in the red. Nifty Realty and Nifty IT were the worst performers, both down over 3.5%, with Realty falling for the third straight day and IT declining for a second session. Auto, Financial Services, Bank, Energy and Metal indices also extended their losing streaks, while FMCG snapped its two‑day rise.

Indian equity benchmarks ended sharply lower, extending their longest losing streak since the second week of January. The sell-off marked the steepest single-day decline since March 30.

The Nifty 50 closed down 1.83% at 23,579.55, while the Sensex fell 1.92% to 74,559.24, reflecting broad-based selling across sectors.

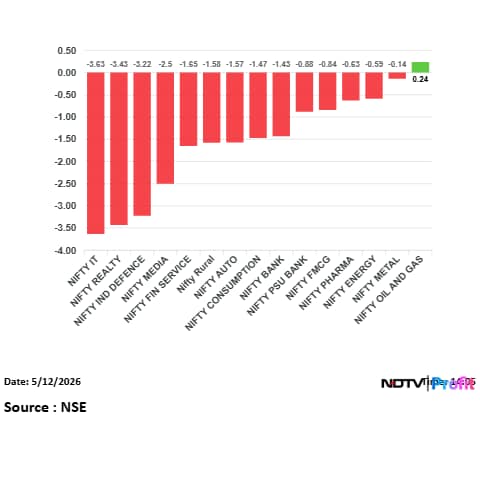

Sectoral indices traded largely lower, with Nifty Realty down about 3.63% and Nifty Defence falling 3.43%. Nifty Media declined 3.22%, while Nifty FMCG, Financial Services, Auto and Consumption indices were also in the red.

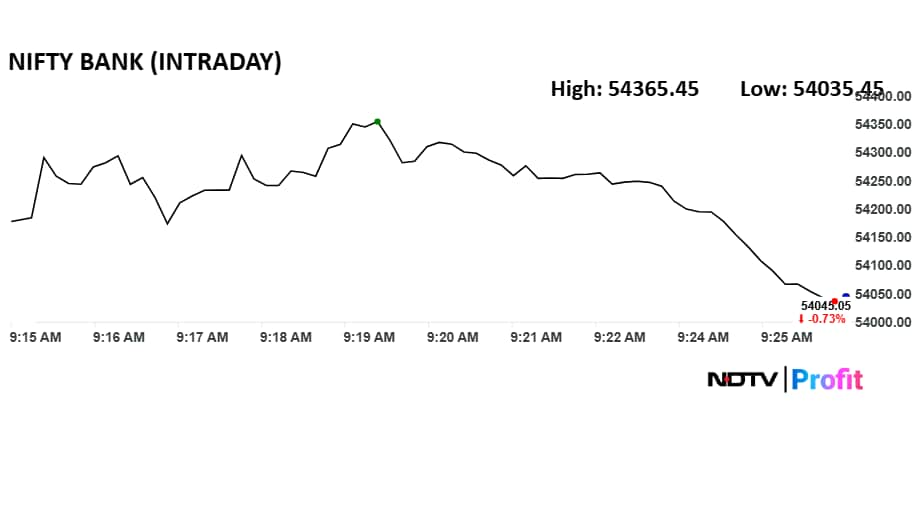

Nifty Bank slipped around 0.88%, while PSU Bank and Pharma saw modest losses. Nifty Metal was the only gainer, rising about 0.24%, while Oil and Gas traded marginally higher.

India’s consumer price inflation likely rose in April, driven by higher cooking gas and fuel prices, according to economists surveyed by Bloomberg. The median estimate pegged CPI inflation at 3.78%, up from 3.4% in March.

Most forecasts see inflation staying below the RBI’s 4% target, though some economists flagged risks from energy prices and weather-related factors. Bloomberg estimates showed a wide range of projections, with expectations reflecting recent LPG price hikes and continued volatility in global energy markets.

The rupee extended losses in trade. The local currency depreciated by as much as 43 paise to 95.74 against the US dollar.

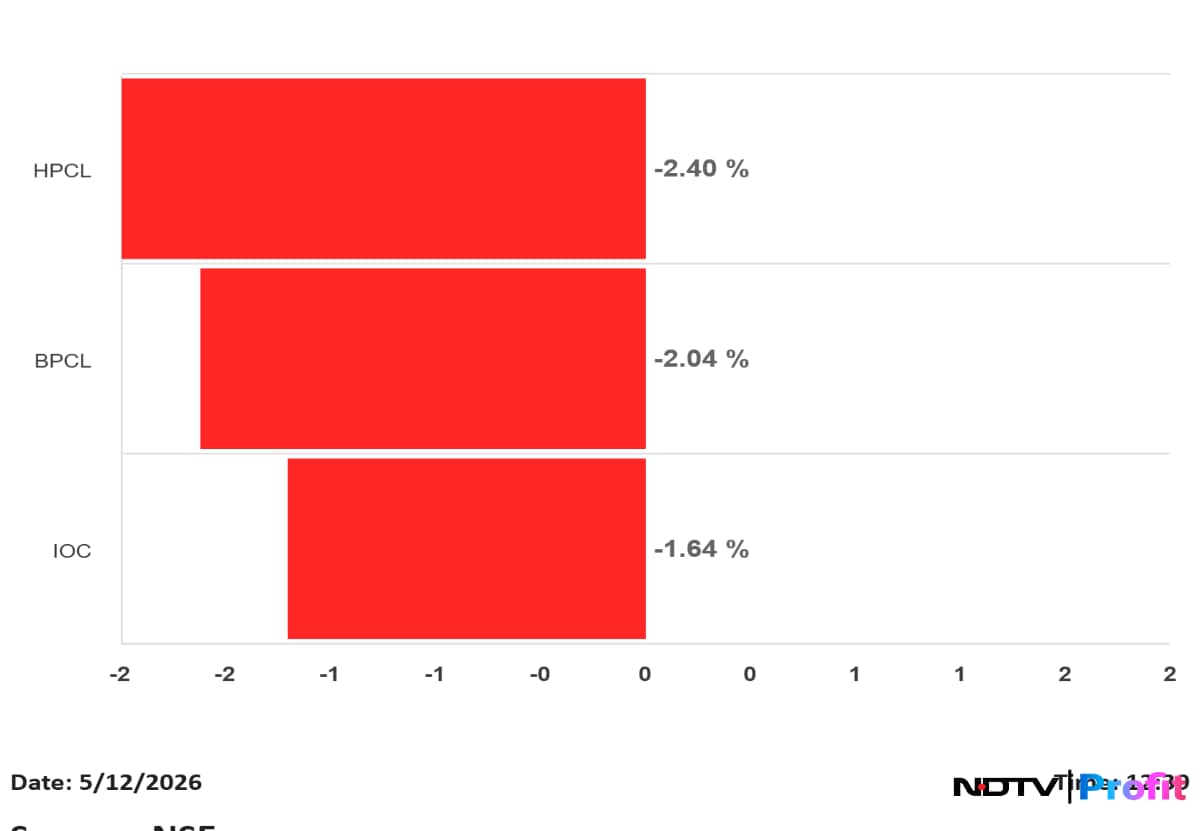

Shares of oil marketing companies traded lower in the session. HPCL fell 2.40%, while BPCL declined 2.04%.

IOC was also under pressure, slipping 1.64% during the trade.

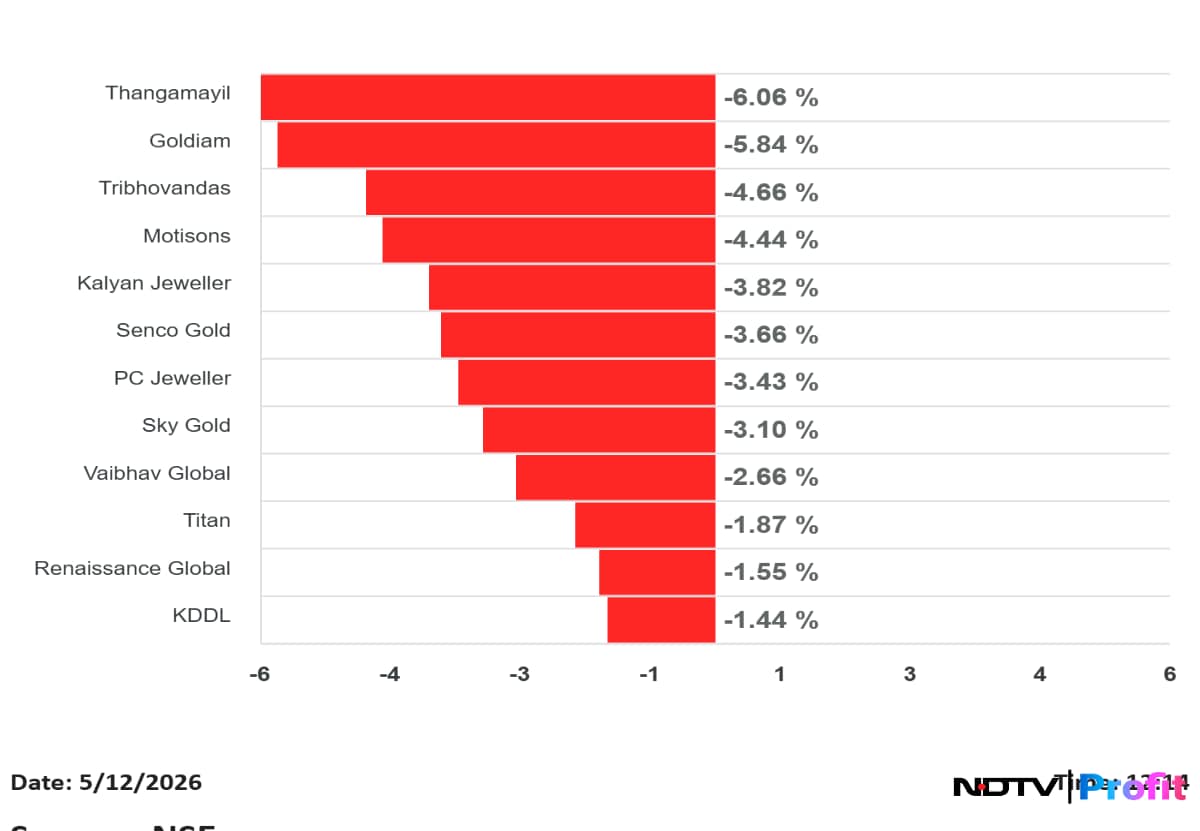

Jewellery stocks traded lower, with Thangamayil falling 6.06% and Goldiam down 5.84%. Tribhovandas Bhimji Zaveri declined 4.66%, while Motisons slipped 4.44%.

Kalyan Jewellers fell 3.82%, Senco Gold dropped 3.66% and PC Jeweller was down 3.43%. Titan declined 1.87%, while Renaissance Global and KDDL also traded lower.

Uday Kotak said Prime Minister Narendra Modi has repeatedly urged Indians to be mindful of spending and dependence, recalling an earlier appeal to hold weddings in India rather than overseas.

He said the Prime Minister has emphasised the risks of living beyond one’s means, warning that excessive reliance on money and power eventually leads to a reckoning. Kotak added that the current global environment reflects a shift towards self-interest, contrasting with forums such as Davos that aim to bring countries together.

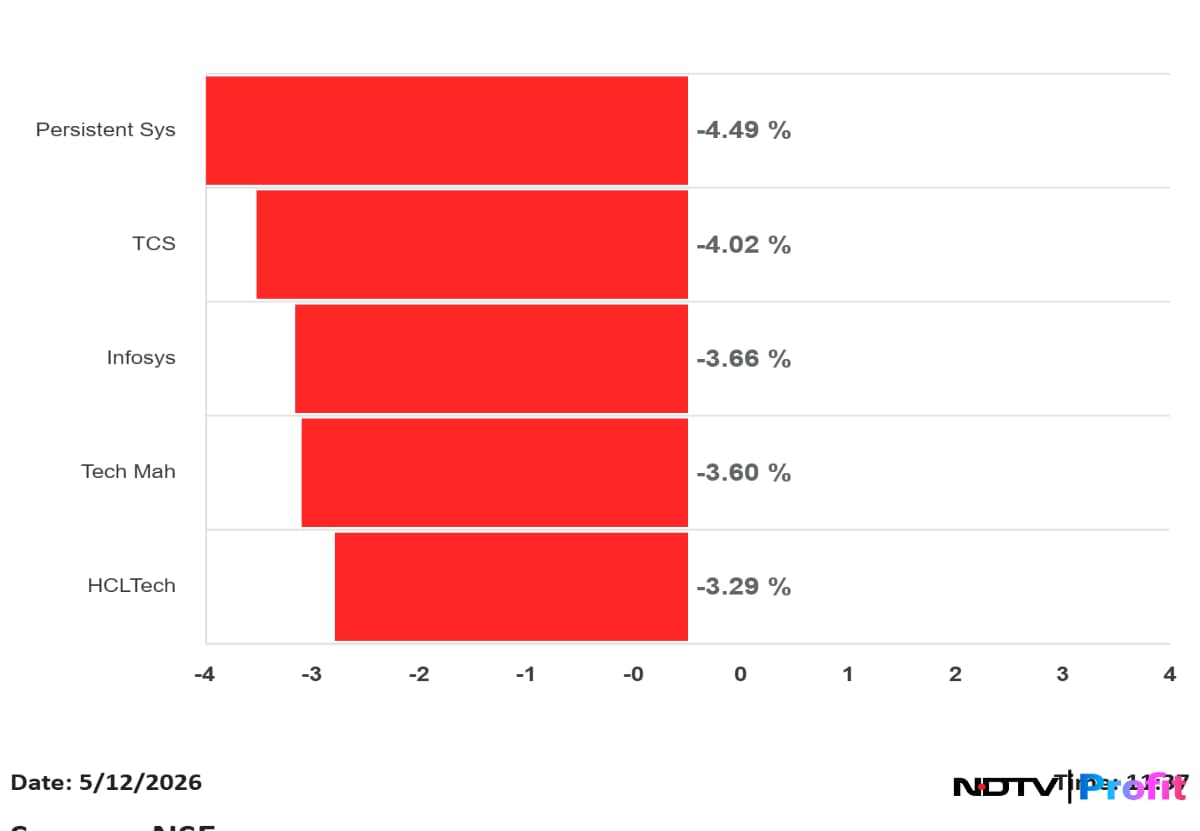

IT stocks remained under pressure, with Persistent Systems falling 4.49% to lead losses in the sector. TCS dropped 4.02%, while Infosys declined 3.66%.

Tech Mahindra slid 3.60% and HCL Technologies fell 3.29%, keeping the Nifty IT index among the top sectoral laggards.

The Nifty 50 slipped below 23,600, falling nearly 1%, while the Sensex dropped over 850 points amid broad-based selling across sectors.

Nifty IT led losses, declining more than 3.5% intraday, weighed by weakness in global technology stocks. Midcap and smallcap indices underperformed the benchmarks, while Bank Nifty also traded about 1% lower. Market breadth remained negative, with declines outpacing advances.

A sharp rebound in small-caps has lifted sentiment, but the bigger question is whether the fundamentals support it.

Key levels, active strikes, big moves and live market cues — all in one place; Join our F&O Hour live blog for real-time action now.

IT stocks remain under pressure as a weaker rupee offers limited support amid weak discretionary tech spending, delayed client decisions and cautious commentary from large companies, said Harshal Dasani, Business Head at INVAsset PMS.

He said investor concerns have shifted to derating risks, with fears that AI-led automation could weigh on billing growth and the traditional outsourcing model. Mixed Q4 commentary, slower deal conversions and global risk-off sentiment have kept export-heavy IT stocks under strain, with investors seeking clearer signs of revenue acceleration.

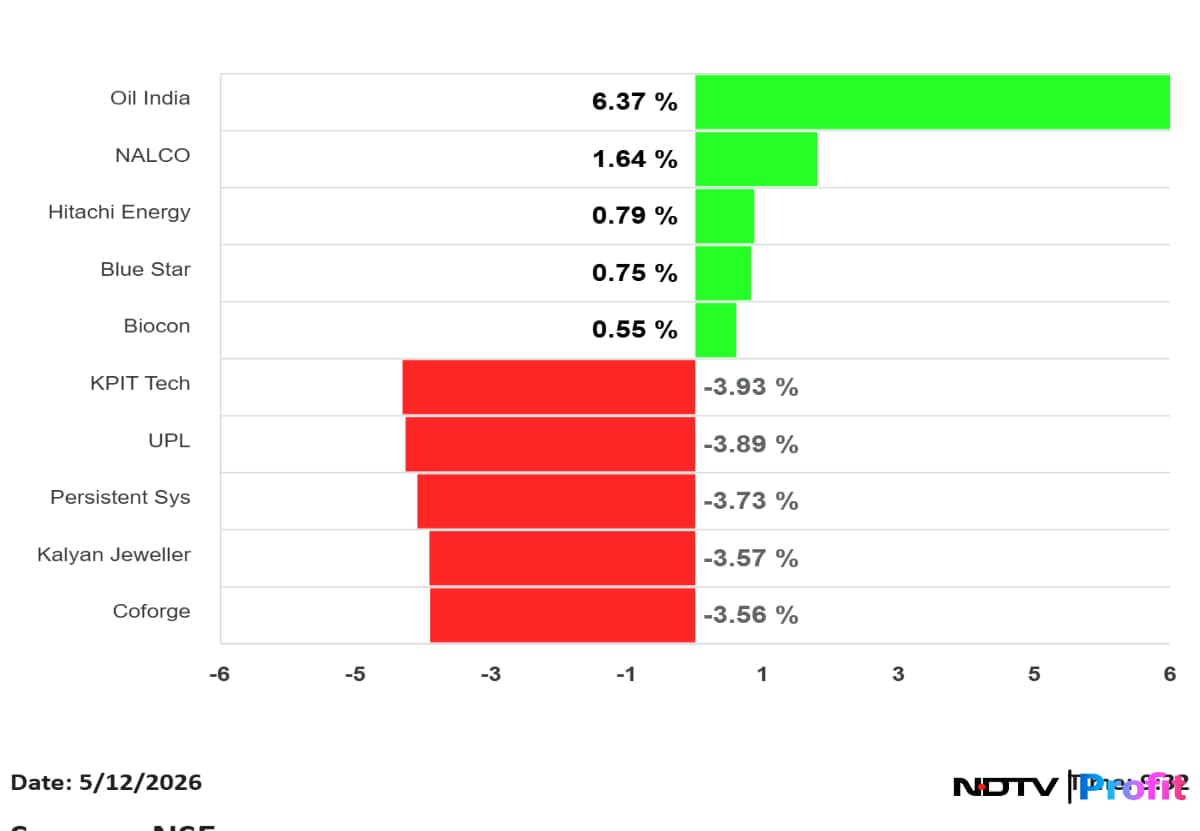

Oil India led the gainers in the Nifty Midcap 100, rising 6.37%, followed by NALCO, Hitachi Energy, Blue Star and Biocon, which posted modest gains.

On the downside, KPIT Technologies, UPL, Persistent Systems, Kalyan Jewellers and Coforge declined between 3.5% and 4%, weighing on the midcap index.

Nifty slipped as much as 0.4% to 23,716 in early trade.

The Sensex fell up to 0.5%, or 384 points, to 75,631.77 at the open.

Bharat Petroleum Corporation may report lower earnings for the March quarter, according to Bloomberg estimates, despite support from inventory gains and stronger refining margins. Net revenue is expected to dip 0.4% year-on-year to Rs 1,17,300 crore, while Ebitda may fall 33% to Rs 7,789 crore and net profit may decline 20% to Rs 6,043 crore. Ebitda margin is seen at 6.6% versus 9.9% a year earlier.

Bloomberg estimates point to inventory gains from higher crude prices and stronger diesel cracks supporting refining earnings, with Singapore GRMs averaging about $9.4 per barrel. However, higher freight and insurance costs, along with losses in petrol, diesel and LPG retailing, are expected to weigh on performance. Blended marketing margins are estimated to turn into a loss, while LPG under-recoveries are seen rising during the quarter.

Investec maintained a Hold rating on Godrej Consumer and cut its target price to Rs 1,130, citing near-term raw material pressure, weakness in soaps and Indonesia, while flagging portfolio changes and category expansion as long-term growth drivers.

Jefferies reiterated a Buy rating with a target price of Rs 1,400, pointing to faster growth in selected categories, steady base business performance and improvement in cash flows and Africa margins. Morgan Stanley kept an Equal-weight rating and lowered its target price to Rs 1,109, highlighting portfolio transformation and double-digit growth expectations over the medium term. Citi maintained a Buy rating with a target price of Rs 1,300, citing improving growth visibility across regions, while flagging some margin sensitivity to commodity inflation.

Dr Reddy’s Laboratories may report lower revenue and profit for the March quarter, according to Bloomberg estimates, due to weakness in its US business and erosion in gRevlimid sales. Revenue is estimated to fall 3.2% year-on-year to Rs 8,248 crore, while net profit may decline 45% to Rs 871 crore. Ebitda is seen down 24.5% at Rs 1,507 crore, with margin at 18.3% versus 23% a year earlier.

Bloomberg estimates indicate the US business may drop about 35% year-on-year amid the gRevlimid patent cliff, portfolio weakness and inventory adjustments, with some estimates showing no gRevlimid contribution in the quarter. India formulations are expected to grow 14–17%, while Russia, CIS and Europe may support performance. Management commentary on semaglutide approvals and biosimilar plans will be in focus.

Dixon Technologies may report pressure on profit and margins in the March quarter, according to Bloomberg estimates, due to weak mobile phone volumes and operating leverage. Revenue is seen rising 2% year-on-year to Rs 10,478 crore, while Ebitda may fall 9% to Rs 399 crore, with margin at 3.8% versus 4.3% a year earlier. Net profit is estimated to decline 54% to Rs 182 crore.

Bloomberg estimates noted that the year-ago quarter included fair value gains of Rs 250 crore from investments in Aditya Vision. Investors will watch for updates on the proposed joint venture with Vivo, for which approvals are still pending.

Citi maintained a Buy rating on PB Fintech with a target price of Rs 2,275, citing market share gains across insurance segments, product-led growth and investments in new platforms such as Pension Bazaar. The brokerage flagged multiple levers to manage commission-related risks.

Macquarie retained its Outperform rating with a target price of Rs 1,945, highlighting continued market dominance, a shift towards a value-partner model and a recalibration at Paisabazaar to improve profitability. Jefferies kept its Buy rating with a target price of Rs 1,950, pointing to operational drivers, value-added services and capital strength. Morgan Stanley maintained an Underweight rating with a target price of Rs 1,215, focusing on higher customer engagement, app-led retention and a gradual recovery in Paisabazaar profitability.

Morgan Stanley retained its Equal-weight rating on Indian Hotels with a target price of Rs 700, citing steady Q4 performance and reiteration of its double-digit revenue growth guidance for FY27. The brokerage flagged stronger-than-expected standalone RevPAR in the quarter.

Macquarie maintained its Outperform rating with a target price of Rs 770, noting a strong Q4 supported by domestic traffic, but said FY27 revenue growth guidance has been lowered by 100 basis points. Jefferies kept its Buy rating with a target price of Rs 800, citing strong domestic demand, 15% EBITDA growth in FY26 and guidance for 12–14% revenue growth in FY27.

Citi maintained its Buy rating on Nuvama Wealth and raised its target price to Rs 2,050 from Rs 2,000.

The brokerage cited strong business momentum, steady yields and healthy wealth flows, and raised its FY2028–29 profit estimate by 2% on higher wealth revenue assumptions.

Afcons Infra emerged as the lowest bidder for a Europe project worth Rs 7,544 crore, while HG Infra Engineering received a Rs 3,931 crore road project order. Bharat Forge signed a long-term supply agreement with Embraer, and HFCL secured export orders worth Rs 184 crore. MRF got relief after a Chennai tax authority set aside a Rs 182 crore tax order, while Canara Bank raised MCLR by 5 basis points across tenures from May 12.

Graphite India raised its stake in Graftech to 9.79%, and Windsor Machines signed an MoU to sell its Thane property for Rs 162 crore. Vodafone Idea said it has received no communication from Vodafone Group on any stake sale. Adani Ports appointed Niraj Bansal as CEO–Ports from June 1, while TeamLease Services’ board will consider a buyback on May 20.

Other updates include Voltas winning its Qatar appeal case with payments and guarantees ordered in its favour, United Spirits amending the RCB share sale agreement with new investors, and NHPC’s stake in Chenab Valley Power Projects declining to 50.86% after dilution.

Earnings are in focus for Bharat Bijlee, Berger Paints India, Bliss GVS Pharma, Borosil Renewables, Bharat Petroleum Corporation, Clean Max Enviro Energy Solutions, Cohance Lifesciences, Dixon Technologies India, Dr Reddy’s Laboratories, Elantas Beck India, Ethos, Gopal Snacks, Huhtamaki India, Indraprastha Medical Corporation, INOX India, Sai Silks Kalamandir, Kalpataru, KPR Mill, Sri Lotus Developers and Realty, Max Financial Services, MTAR Technologies, Nazara Technologies, Neuland Laboratories, NIIT Learning Systems, Novartis India, Park Medi World, Pfizer, Religare Enterprises, Keystone Realtors, Sagility, Seshasayee Paper and Boards, SKF India, Industrial Stove Kraft, Tata Power Company, Texmaco Rail Engineering, Thomas Cook India, Torrent Power, Ventive Hospitality, V-Guard Industries and Vinati Organics.

S&P 500 futures were marginally higher, while Nasdaq 100 futures rose 0.1%. Dow Jones Industrial Average futures gained 24 points, or less than 0.1%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.

.png?im=FeatureCrop,algorithm=dnn,width=350,height=197)