(Bloomberg Opinion) -- One of this century's top performing European stocks has fallen back to earth with a thud. The struggles of German life-sciences firm Sartorius AG encapsulate the pain caused to businesses by rising interest rates, fading Chinese demand and the normalization of sales following the pandemic. Thought by investors to be somewhat recession-proof, Sartorius has turned out to be alarmingly volatile.

Goettingen-based Sartorius and its fully consolidated Paris-listed subsidiary Sartorius Stedim Biotech make laboratory instruments and sterile plastic products for the development and manufacturing of biological drugs and vaccines. (Biopharmaceuticals are derived from living organisms as opposed to being chemically synthesized.)

Its orders boomed as scientists raced to develop biologics to fight cancer and chronic diseases. Investors were particularly attracted by the perceived stability of bioprocessing: Recurring revenue is high because many Sartorius products are single-use; furthermore, the company's equipment is specified as part of the drug-approval process, meaning it can't easily be dislodged by rivals.

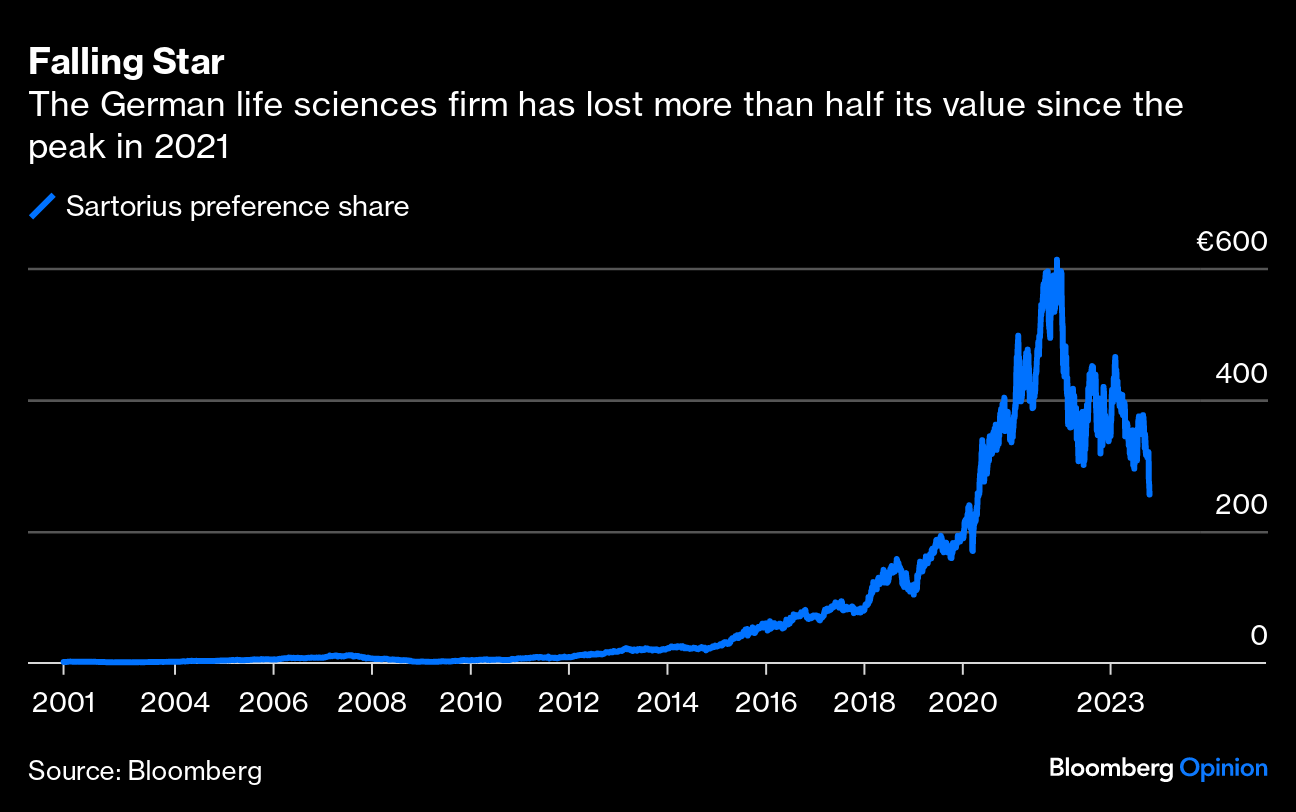

Between 2001 and the peak in 2021, the more widely traded non-voting preference shares returned 46,000%, according to Bloomberg data, which assumes dividends are reinvested. Stock investors would be delighted to own a 10-bagger — a stock that increases 10 times in value — whereas Sartorius was an almost 500-bagger during that 20-year period. The company joined the DAX Index in 2021 when its market capitalization briefly exceeded €50 billion ($53 billion) — larger than BMW AG at the time. Edinburgh-based asset manager Baillie Gifford is one of the biggest shareholders.

The excitement hasn't lasted. The stock has since sunk more than 50% after it twice warned on profit this year and last week said financial targets for 2025 are “under review.” Short interest as a percentage of the Sartorius free float has nearly trebled over the past year to around 15%, according to data from IHS Markit Ltd. AQR Capital Management LLC disclosed a short position earlier this month.

Sartorius and rivals such as Danaher Corp., Merck KGaA and Thermo Fisher Scientific Inc. are facing a cornucopia of challenges. Pharma companies and their contract manufacturers are no longer ordering as much kit to produce Covid-19 vaccines and tests. Other customers are now reducing the extra inventories they amassed to protect themselves from snarled supply chains — a destocking phenomenon we've seen across the economy. Early-stage biotech customers face an R&D funding squeeze triggered by higher interest rates. And US and Chinese customers have grown more cautious about investment or have sufficient capacity. The upshot is Sartorius' revenue is expected to fall about 17% this year.

Destocking can be doubly painful for companies because it can leave factories underutilized. This is one reason why the company's profit has declined. Earnings before interest tax, depreciation and amortization margins fell around 7 percentage points year-on-year in the third quarter — albeit to a still-ample 26.7%. During the same period, net income attributable to Sartorius shareholders slumped 94% to just €8.6 million, according to figures published on Thursday.

These effects have wrong-footed some investors who may have assumed the company's recent bumper earnings growth would continue unabated. In hindsight, Sartorius was “over-earning” in the pandemic. After a 7% rebound in early trading Thursday, the shares are hardly cheap — the price is equivalent to 47 times estimated earnings.

Of course, customer inventories will eventually be depleted, and they will have to start ordering again, but the rebound has taken longer than expected to materialize — a pattern also seen in other sectors, such as chemicals.

However, some headwinds Sartorius is facing might not be temporary. For example, it's encountering more local competition in China — which accounts for about 11% of sales. It's unclear how far Beijing will favor local firms or if Chinese rivals will be able to seize market share overseas.

Sartorius also made its life harder with a €2.4 billion cell- and gene-therapy acquisition earlier this year, which is projected to increase net indebtedness to more than five times Ebitda. Last month, it issued €3 billion of bonds of varying maturities with interest costs in excess of 4.3%, which will weigh on earnings.

A clutch of promising biologic therapies for diseases such as Alzheimer's and the continuing industry shift to single-use plastic bioreactors (which are less expensive and consume less water and energy) from multiuse stainless steel should mean Sartorius' long-term prospects remain rosy. S&P Global Ratings expects the bioprocessing market to expand 10% a year in the medium term.

But the lack of visibility on a demand rebound has lowered the multiple investors are willing to pay for those anticipated earnings. (They must wait until January for detailed guidance on next year's performance and for new midterm targets.)

A business built on preventing contamination requires less blotchy financial reporting.

More From Bloomberg Opinion:

-

The CDC's Covid Booster Strategy Is Failing: F.D. Flam

-

Hedge Funds Feast on a French Train Wreck: Chris Bryant

-

A 35,000% Stock Market Return in Europe? Here's How: Chris Bryant

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies in Europe. Previously, he was a reporter for the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.