In their third meeting, the six members of the Reserve Bank of India's Monetary Policy Committee voted unanimously yet again, to hold the policy rate steady at 6.25 percent for the second review in a row. This pause surprised the markets, which had pencilled in a rate reduction in the February policy review, given the continued decline in headline consumer price index (CPI) inflation as well as the fiscal consolidation attempted in the Union Budget for financial year 2017-18.

Moreover, the repo rate was kept unchanged even though the MPC expects headline CPI inflation to remain softer than its target of 5 percent for January-March 2017 (Q4FY17) and despite the unsurprising cut in its Gross Value Added (GVA) growth forecast for FY17 to 6.9 percent from 7.1 percent. The caution displayed in the policy review was attributed to the ongoing uncertainty related to inflation and growth, after the note ban, and persistently sticky core inflation. Nevertheless, the policy decision re-emphasises the Committee's overarching focus on inflation concerns rather than risks to growth.

Clear Shift To 4% Inflation Target

Without specifying a timeline, the Committee indicated a clear shift in its focus to bringing the CPI inflation to 4 percent, i.e. the midpoint of the inflation target range of 2-6 percent, in a durable and calibrated manner.

This, in conjunction with the change in the monetary stance from accommodative to neutral, lent a decidedly hawkish slant to the policy document.

In light of the bleak assessment of the space for future easing, the MPC laid emphasis on resolution of banks' non-performing assets, faster recapitalization of banks and fuller adjustment of interest rates on small savings schemes to improve transmission to lower lending rates, steps that need to be taken by the banking sector and the government.

Also Read: Wither Away Ambiguity On Monetary Policy

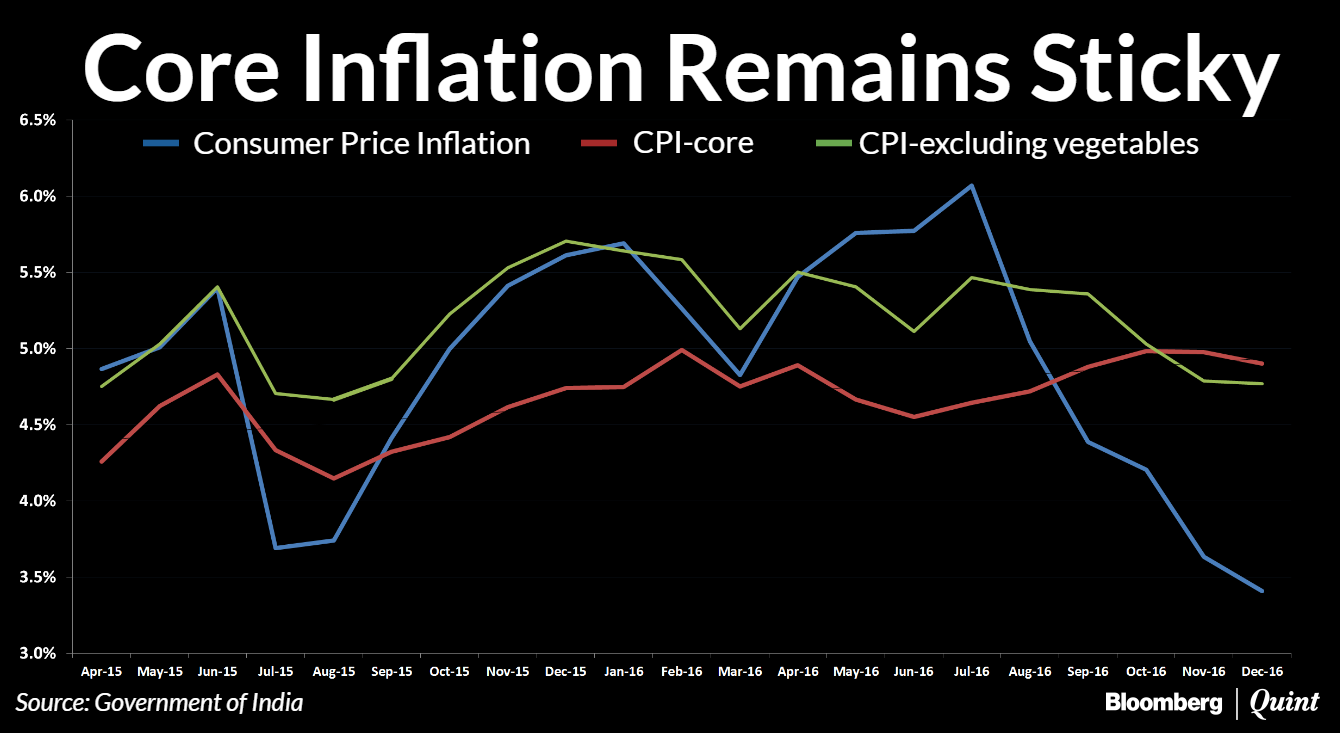

Risk Of Food Price Rebound

Headline year-on-year CPI inflation has declined from 6.1 percent in July 2016 to 3.4 percent in December 2016, well below the Q4FY17 target of 5 percent. However, the Committee highlighted that this has been led by food items, particularly by prices of vegetables. While a part of this decline was seasonal, anecdotal evidence suggests that distress sales after the note ban also contributed to the collapse in perishable prices.

As a result, a likely rebound in vegetable prices may push up CPI inflation going forward.

While CPI inflation excluding vegetables remains significantly higher than headline inflation, it has also declined in recent months, and ICRA forecasts it to remain lower than the overall CPI inflation target of 5 percent during Q4FY17.

FY18 Inflation And Growth Estimates

The MPC expects a favourable base effect and post-demonetisation demand compression to keep CPI inflation between 4.0-4.5 percent in the first half of FY18, after which it would harden to 4.5-5.0 percent in the second half of the next financial year as the base effect wanes. Rising crude oil and base metal prices, exchange rate volatility and higher house rent allowance based on the Seventh Central Pay Commission's recommendations were highlighted as key risks.

In our view, average CPI inflation would ease modestly to 4.5 percent in FY18 from 4.7 percent in FY17.

As the impact of the note ban dissipates, the MPC expects GVA growth to improve sharply from 6.9 percent in FY17 to 7.4 percent in FY18, with a rebound in discretionary consumer spending, improvement in activity in cash intensive sectors and higher capital spending by the union government.

ICRA expects a somewhat milder improvement in GVA growth from 6.6 percent in FY17 to 7 percent in FY18.

Also Read: ‘Inflation Concerns Led RBI To Hold Rates, Shift Policy Stance To Neutral'

Liquidity Outlook

As expected, the neutral stance on system level liquidity was maintained. The MPC indicated that the prevailing surplus liquidity conditions would decline with remonetisation, which would gather pace with the further easing of withdrawals in two tranches in February and March 2017. However, the Committee expects the surplus liquidity to persist until the early months of FY18.

Aditi Nayar is principal economist at ICRA.

The views expressed here are those of the author's and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.