The demand for a waiver of farm loans has emerged from a cross-section of states across the country. From Punjab and Uttar Pradesh in North and Central India to Maharashtra in the West and Karnataka in the South.

The most immediate reason cited to back such demands is the drop in prices of certain items like vegetables and pulses. That, however, is nothing more than a short-term trigger as vegetable prices have been historically volatile. Already, reports have surfaced suggesting a surge in vegetable prices, which appears to correct unnaturally low prices that prevailed in the pre-monsoon season. Similarly, in the case of pulses, research from economist DK Joshi at CRISIL showed that pulses inflation tends to spike and fall every three years.

Writers, including in this publication, have raised a number of fundamental issues plaguing agriculture which lead to recurring demands for farm loan waivers. In an article on June 15, Yoginder Alagh had written about the shifting terms of trade, which are once again turning unfavourable for farmers. In a June 19 article in The Indian Express. Ashok Gulati and Prerna Terway of ICRIER showed that net margins in most agricultural commodities have declined over the last three years. These are all factors adding to the distress in the farm sector.

To this ongoing debate, the Reserve Bank of India (RBI) governor Urjit Patel has added another variable, which is worth mulling over. The minutes of the last monetary policy committee meeting showed that Patel had highlighted a specific data point, albeit without accompanying analysis.

... It may be instructive to note that the outstanding advances to agriculture and allied activities as ratio to GDP from agriculture and allied activities has increased from about 13 percent in 2000-01 to around 53 percent at present; average annual nominal growth rate in Scheduled Commercial Banks' advances to agriculture & allied activities was 21.5 percent during 2000-01 to 2016-17.

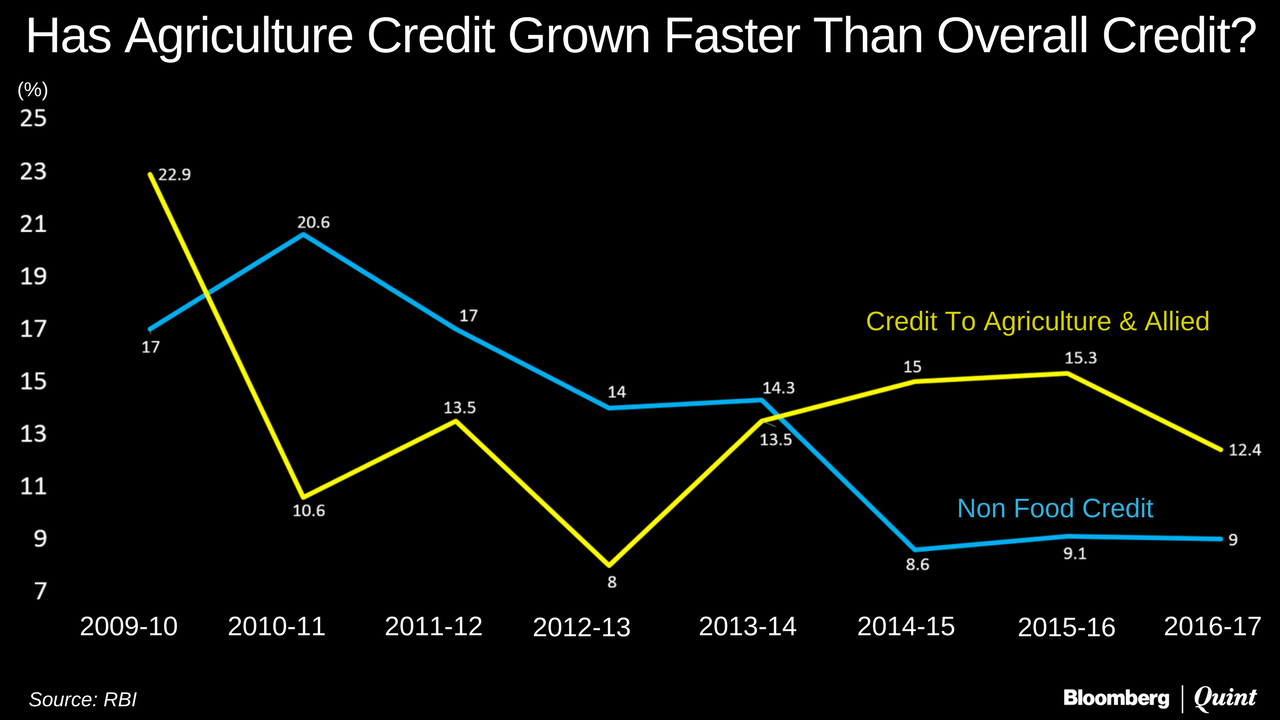

Data on sectoral deployment of credit between 2009-10 and 2016-17 shows that agricultural lending has grown faster than overall credit in the last three years. But this is likely because of the slump seen in industrial credit demand. Data before 2009-10 is not available on the RBI's website.

So, what is Patel trying to say?

The first thing to understand is that the increase in the ratio cited by Patel is a result of a numerator that is growing faster than the denominator. This means that while the share of gross domestic product contributed by agriculture (the denominator) has been declining, the pace at which loans to agriculture have been growing (numerator) has not been moderated.

Think of an example less emotive than agriculture. For instance, the bearings industry. If the income generated by the sector declines, banks should lend less to it because lower income would impact the capacity to repay loans.

This is not so in agriculture, which is governed by priority sector lending rules.

Under the current rules, banks have to lend 40 percent of net credit to sectors which are considered to be a national priority and where access to credit it limited. The largest chunk of this, 18 percent, goes to agriculture. Of this, 8 percent goes to small and marginal farmers. While the priority sector guidelines were reviewed in 2015, the overall target for lending to agriculture was held steady at 18 percent, even though the distinction between direct and indirect lending was removed.

The point being that while the share of agriculture in the country's GDP has declined, the share of lending to agriculture has remained steady. To be sure, at 53 percent, the outstanding credit-to-GDP ratio for agriculture is within comfortable limits. The pace at which this ratio has risen, however, may be noteworthy.

Bindu Ananth, chair of the IFRM Trust, who was also part of a 2013 committee on financial inclusion, said that there has always been a valid argument in favour of making priority sector lending targets more dynamic. Static targets, when not reviewed often enough, may lead to a situation where allocation of credit is not in keeping with developments in the real sector.

The Nachiket Mor Committee report had highlighted this need for a more dynamic approach towards priority sector lending (PSL).

“In order for PSL targets to automatically reflect the needs of the underlying economy, the Committee recommends that since in accordance with its vision, each ―significant sector or sub-sector (with more than a 1 percent contribution to the GDP) of the economy should achieve at least a 50 percent credit to GDP ratio (financial depth) in order to ensure that the absence of finance is not retarding its growth, the difference between actual financial depth and this 50 per cent goal should determine the weight assigned to it,” the report said.

Going by this recommended approach, it may be time to reduce the emphasis on agriculture lending as part of the priority lending program.

The debate, however, can be viewed in other ways as well.

One valid counter argument is that a large part of credit to the rural and agriculture sector continues to come from informal sources. As such, a continued focus on bank credit is important to replace informal credit. Gulati and Terway, in their article, had pointed out that informal credit remains a large part of credit available in rural areas. “Even in 2013 – the latest information we have – of the total outstanding debt of rural households, 44 percent came from informal sources,” the authors wrote.

To bring down this proportion, it would be important to see continued growth in agriculture lending from banks. Since such lending may not always make business sense for banks, some sort of push, through lending targets, may continue to be needed. The extent of the push, however, may need to be adjusted.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.