(Bloomberg) --

The European Central Bank is finally about to join the global bandwagon of monetary policy tightening, spurred into action by repeated record highs in inflation.

Almost three months since the US Federal Reserve delivered a first interest-rate hike, its euro-zone counterpart will this week announce an end to bond purchases and formally begin the countdown to an increase in borrowing costs in July.

The ECB has hesitated to remove stimulus while gauging the fallout from the war raging just over the frontier of its currency area in Ukraine.

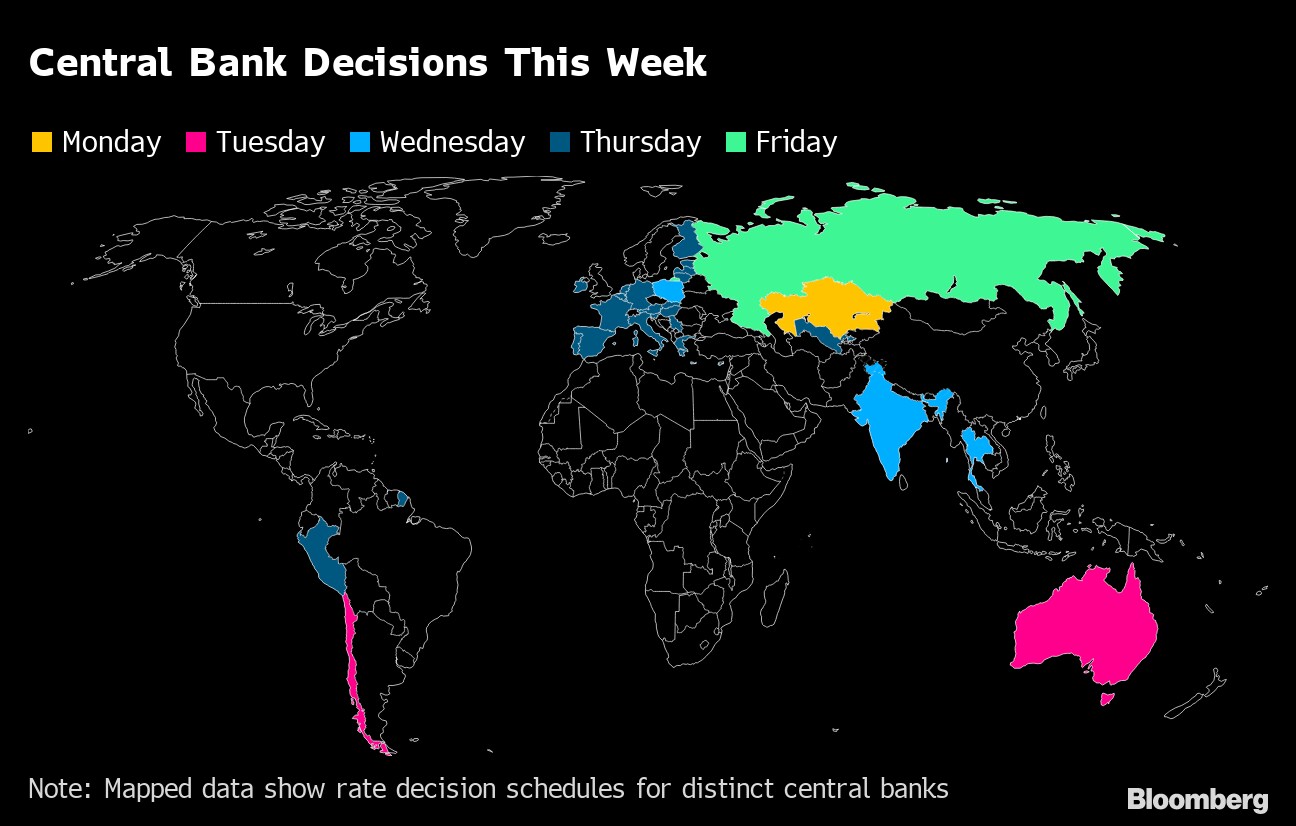

By contrast, most major central banks are now further down the road with tightening, and some are even ratcheting up the pace. The Fed doubled the speed of rate hikes last month with a half-point increase, and policy makers in Australia on Tuesday and India on Wednesday could follow suit with faster moves too.

Against that backdrop and with euro-zone inflation now at 8.1%, there's a clear consensus at the ECB on the need to get started. The argument now within the Governing Council centers on whether quarter-point increases are enough, and on how high to ultimately bring rates next year.

Austrian central bank Governor Robert Holzmann says anything less than a half-point move “risks being seen as soft,” and colleagues from the Netherlands, Slovakia and Latvia have openly called for such an increment to at least be considered.

What Bloomberg Economics Says:

“The majority of the Governing Council seems to be in support of a smaller move, but market participants will be closely watching remarks after the ECB's meeting on June 9 for hints that the hawks are once more gaining the upper hand.”

--David Powell and Jamie Rush. For full analysis, click here

Forecasters at Deutsche Bank and Bank of America now reckon that will materialize, but most economists currently assume the hawks' views won't prevail.

ECB President Christine Lagarde is likely to face questioning on that debate at her press conference on Thursday after the meeting. She will also unveil crucial new forecasts that informed the decision, with projections that may invite comparison with the OECD's latest global outlook due the previous day.

Elsewhere, central banks from Chile to Poland will probably continue hiking too, Russian policy makers may deliver a rate cut, and US consumer-price data is likely to show a monthly acceleration.

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

US Economy

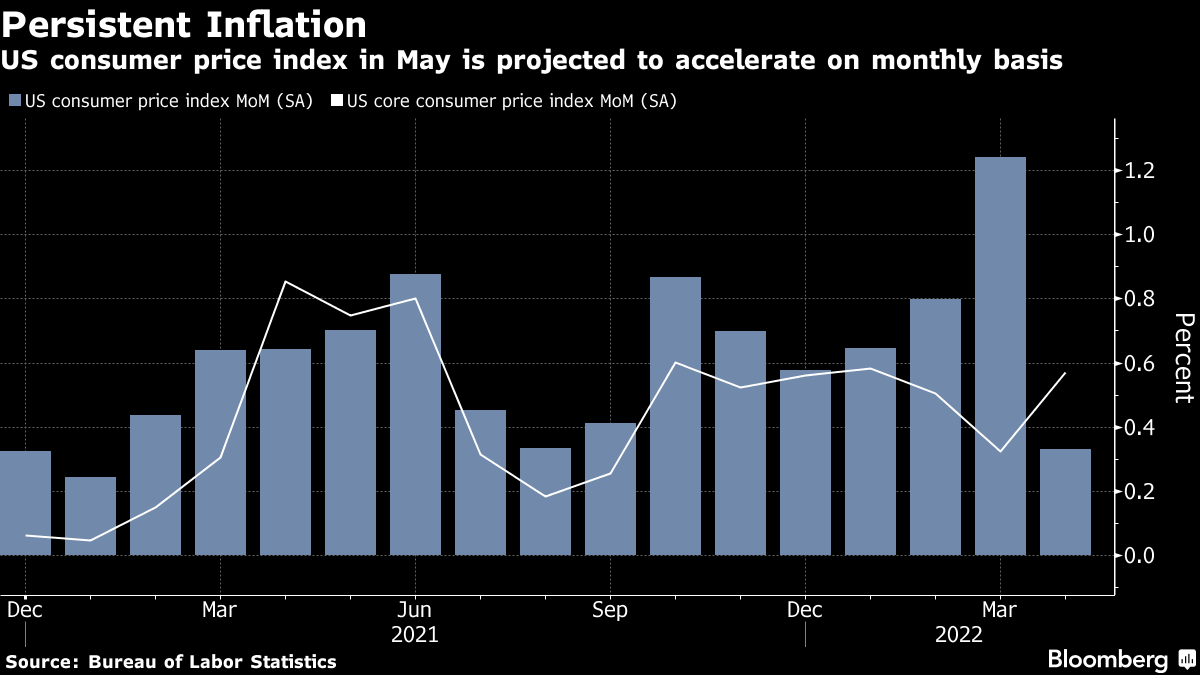

In the US, the May consumer price index takes top billing in an otherwise quiet week for economic data. Fed officials will observe a blackout period ahead of their June 14-15 policy meeting.

The government's CPI report on Friday is expected to show inflation accelerated on a month-to-month basis, due in part to record gasoline prices. Excluding fuel and food, the core measure probably posted another sizable advance that indicates sustained price pressures.

The projected monthly gains are seen keeping annual inflation elevated. Economists are calling for an 8.3% year-over-year increase in the overall CPI and a 5.9% gain in the core measure.

- For more, read Bloomberg Economics' full Week Ahead for the US

Asia

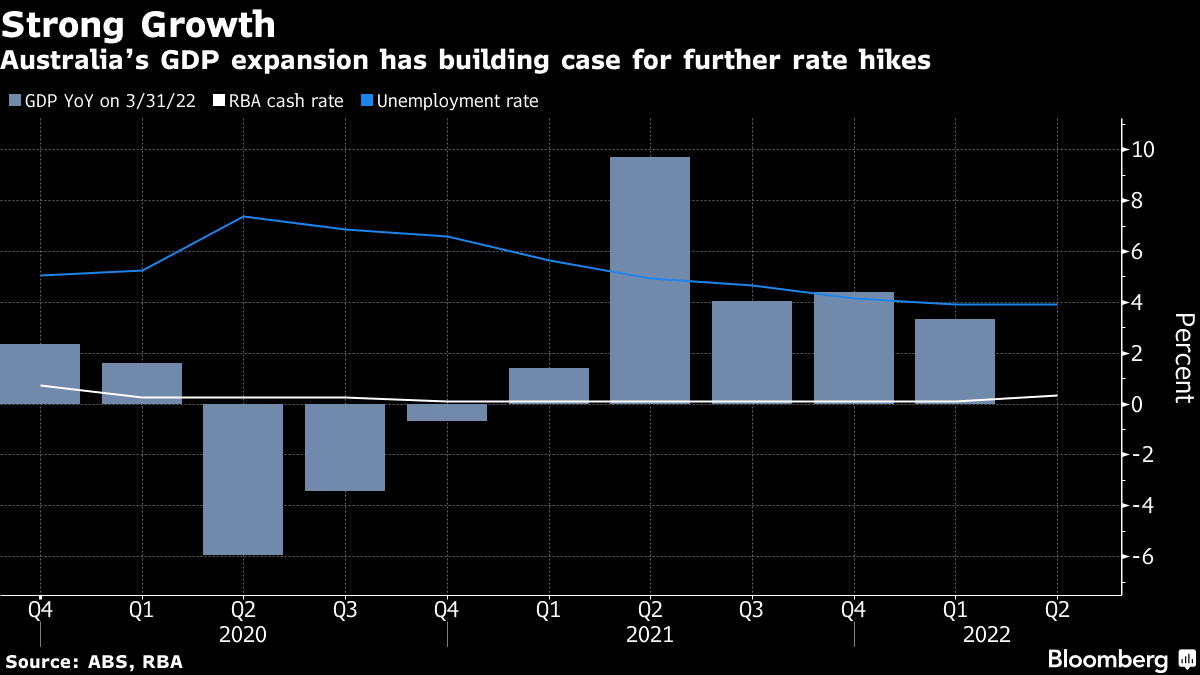

The Reserve Bank of Australia meets Tuesday with another rate hike anticipated as inflation continues to outstrip forecasts and the economy holds up better than forecast.

The question is by how much, with the official cash rate out of sync with its usual quarter-point settings.

Australian consumer prices have accelerated from the 5.1% recorded in the first three months, Treasurer Jim Chalmers said Sunday.

“It's now really clear that the inflation challenge that Australians are facing is worse,” Chalmers told News Corp., saying he'll likely raise the forecast in next month's economic statement to parliament. “People should anticipate that it will be higher than it is now. Significantly higher.”

India's central bank is also expected to raise rates again on Wednesday, while the Bank of Thailand is likely to buck the hiking trend.

Japan and South Korea will revise their GDP figures for the first quarter on Wednesday. Japanese household spending and wage figures for April will show how the rebound from a first-quarter contraction is faring, with soaring energy prices and a weak yen anticipated to limit the release of pent-up demand.

Remarks by Bank of Japan Governor Haruhiko Kuroda during the week will be closely parsed for any signs of change as prices keep rising and the yen shows renewed weakness.

Chinese trade data on Thursday and inflation data on Friday will be closely scrutinized after purchasing managers reports for May pointed to some improvement as lockdowns eased.

- For more, read Bloomberg Economics' full Week Ahead for Asia

Europe, Middle East, Africa

While the ECB decision on Thursday will take center stage, manufacturing data from around the euro zone may also attract investor attention.

Both German factory orders on Tuesday and industrial production the next day are likely to show improvement at the start of the second quarter, picking up after disruptions caused by supply bottlenecks. Spanish output on Tuesday is also expected to rise, though Italian factory data on Friday may have fallen.

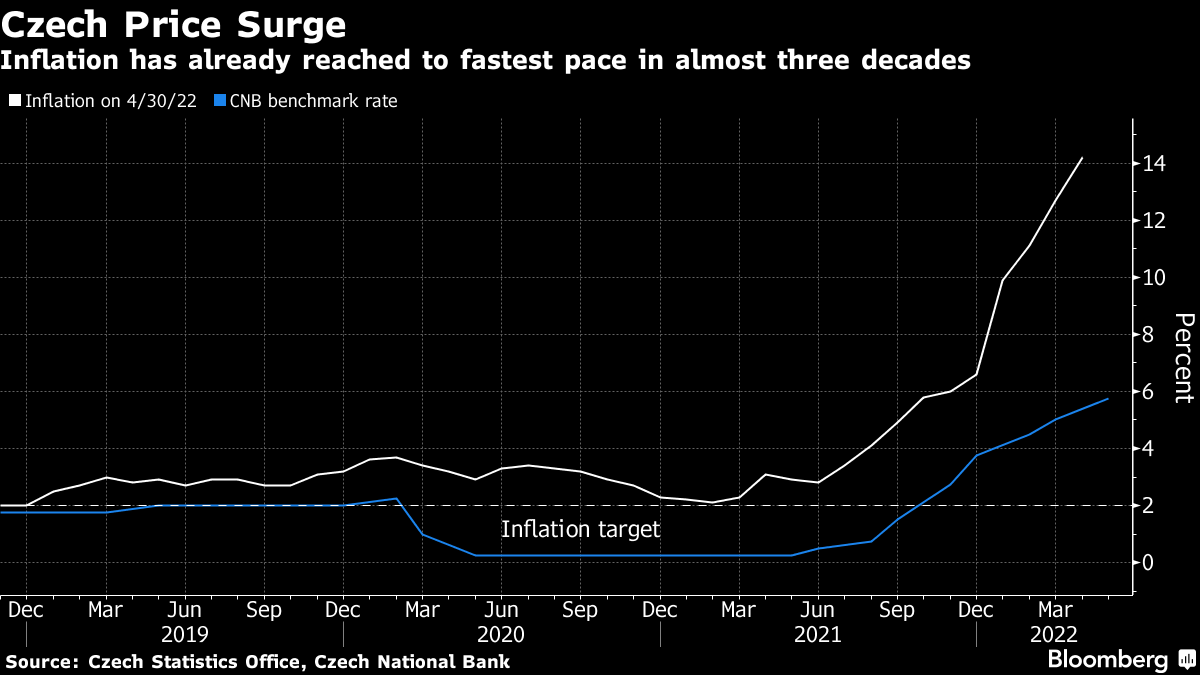

Consumer-price data will draw focus elsewhere in Europe. In the Czech Republic, economists anticipate inflation to surge above 15%, posing a challenge to the incoming central bank governor who plans to halt aggressive rate hikes.

Meanwhile Norwegian officials will watch for an acceleration in annual price increases too, with a reading of 5.6% expected.

Among central bank decisions due, Polish policy makers will probably raise rates for the ninth straight month on Wednesday, and their Serbian counterparts may consider additional tightening too the next day.

Russia is going the other way. Governor Elvira Nabiullina is expected to cut rates further on Friday, dismantling more of the economic defenses she established after sanctions were imposed on Russia following its invasion of Ukraine.

The bank already delivered its third rate reduction in just over a month on May 26 at an extraordinary meeting, reaching 11%.

Nabiullina, who more than doubled the key rate to 20% after the invasion began in late February, said after the last cut that she saw further room for easing at meetings ahead.

- For more, read Bloomberg Economics' full Week Ahead for EMEA

Latin America

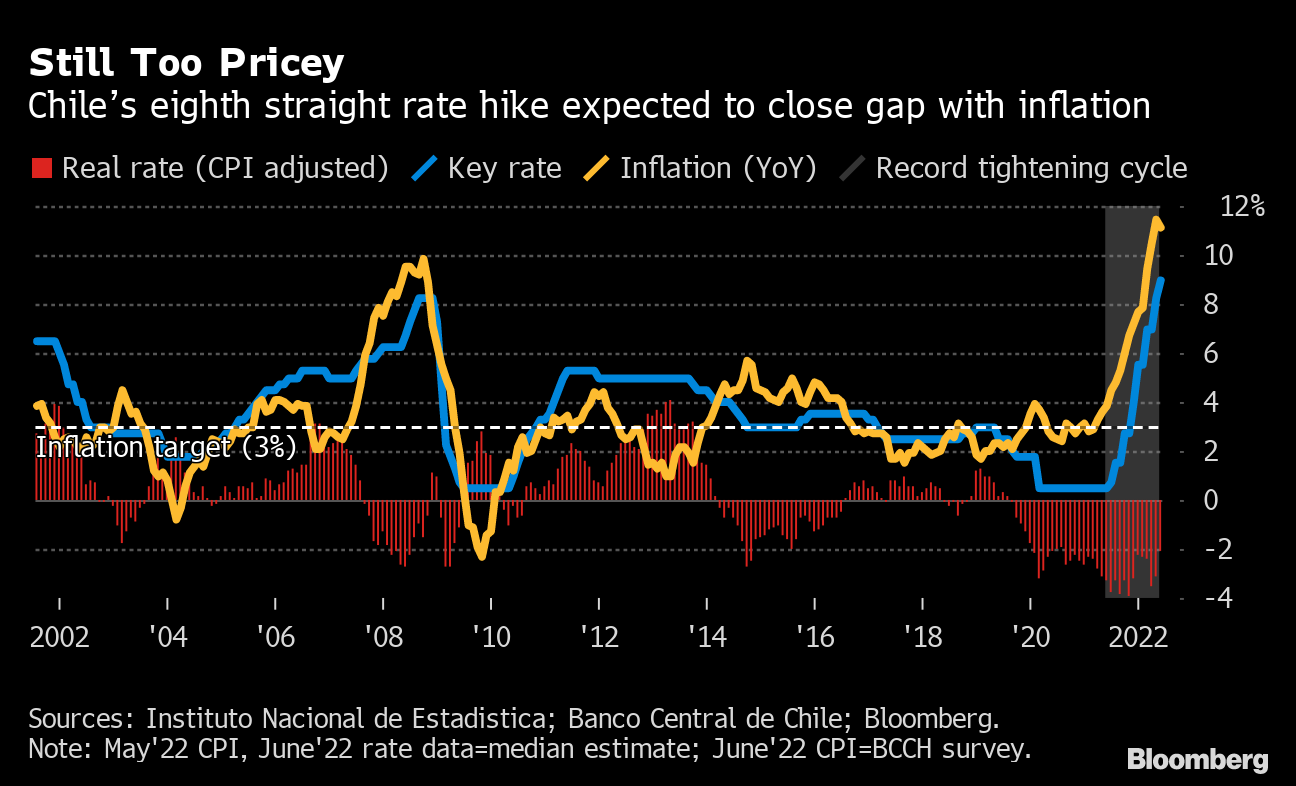

Look for a bit of history out of Chile on Tuesday where the central bank is expected to raise its key rate to a record high 9% to extend its sharpest and longest-ever tightening cycle.

Watch for the May consumer price numbers in Brazil posted Thursday to ease -- some economists see April as the peak -- but not by enough to hold off the 11th straight rate hike next week.

Analysts see Peru's veteran monetary chief, Julio Velarde, going with a 10th straight half-point hike to put the key rate at 5.5%.

On Wednesday, economists expect Chile's May inflation reading to accelerate for a 15th straight month, up from April's near three-decade high, to well over 11%. Core inflation has nearly tripled in the last year.

The numbers may be lower but the consumer price data Mexico reports Wednesday are only slightly less dire as both headline and core readings hover near two-decade highs.

The figures will do nothing to quell speculation that Banxico's patience is wearing thin and a record 75 basis-point hike on June 23 is a very real possibility.

- For more, read Bloomberg Economics' full Week Ahead for Latin America

(Updates with comments on Australia inflation in Asia section)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.