(Bloomberg) -- Bank of England Governor Andrew Bailey may insist that it is “much too early to be thinking about rate cuts,” but the financial markets have other ideas.

All the talk after the BOE held rates at 5.25% for the second meeting in a row was about when policy makers will begin their descent from “Table Mountain,” the higher-for-longer strategy to tame inflation coined by Chief Economist Huw Pill.

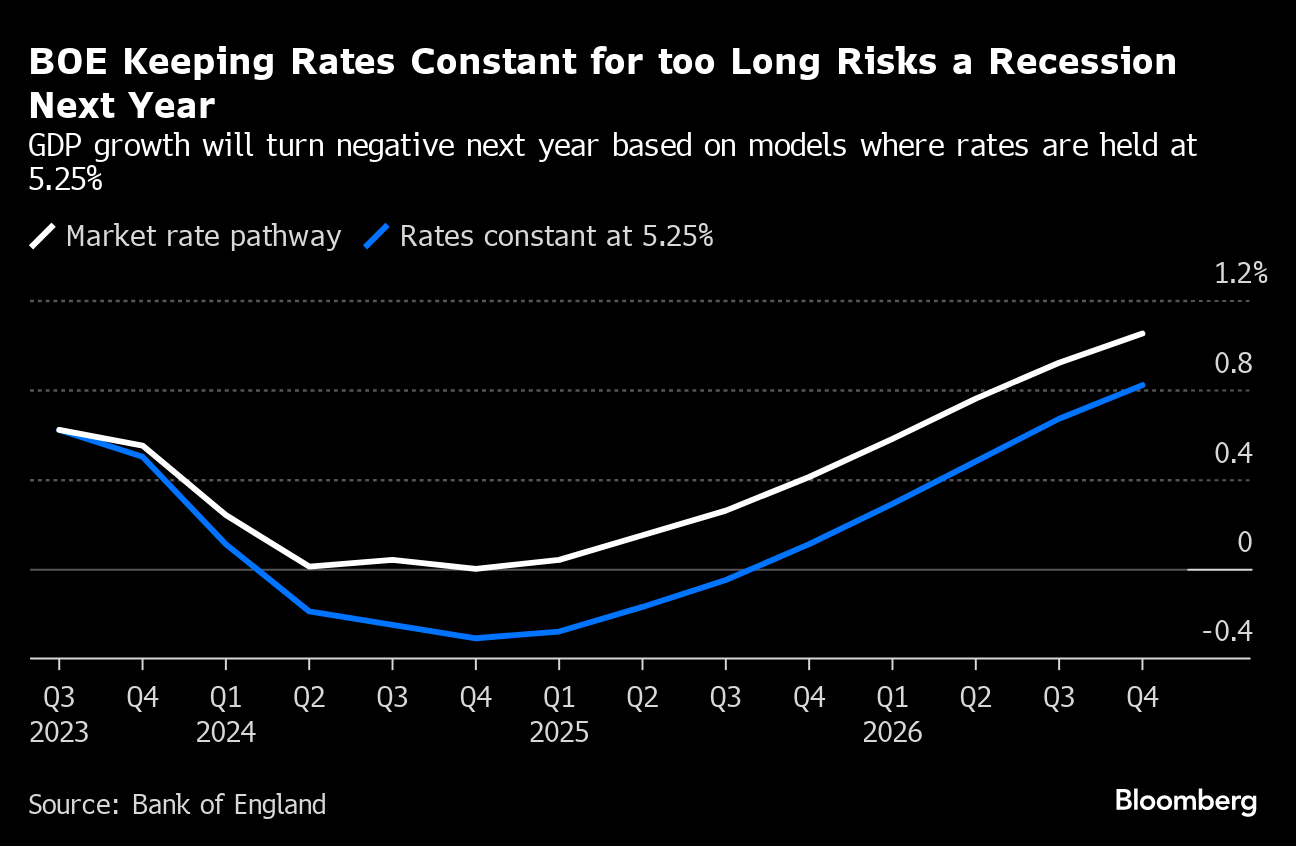

After 14 consecutive rate rises from 0.1% in December 2021, the BOE has now pressed pause on its quickest tightening in three decades. Officials embedded a market expectation for one rate cut to 5% by the end of 2024 when they drew up their latest forecasts last week.

After the markets passed judgment on Thursday, there were two quarter-point reductions fully priced in – the first for August — and the possibility of a third later in 2024, according to swaps tied to policy-meeting dates. That compares with barely one decrease priced just two weeks ago. The betting by investors marks a sharp contrast with the message Bailey repeated in seven interviews and a press conference after the decision.

Investors expect that rates will be cut sharply in the second half of 2024 because they fear the UK economy will break under the strain of rates at their highest level in 15 years. While inflation remains more than triple the BOE's 2% target and wages are rising at near a record rate, unemployment is up, the housing market has ground to a near standstill, and surveys warn a recession is already underway.

“The reluctance to push UK yields higher has suggested greater nervousness about the outlook for the UK economy,” said Oliver Blackbourn, portfolio manager at Janus Henderson Investors. The BOE's new econoomic forecasts painted the same picture.

UK bonds led a global bond rally as the market repriced. The yield on 10-year gilts at one point fell as much as 18 basis points to a three-week low.

The BOE has now swung in line with the US Federal Reserve and the European Central Bank. “The global monetary policy tightening cycle looks done now,” said Henry Cook, senior economist at MUFG.

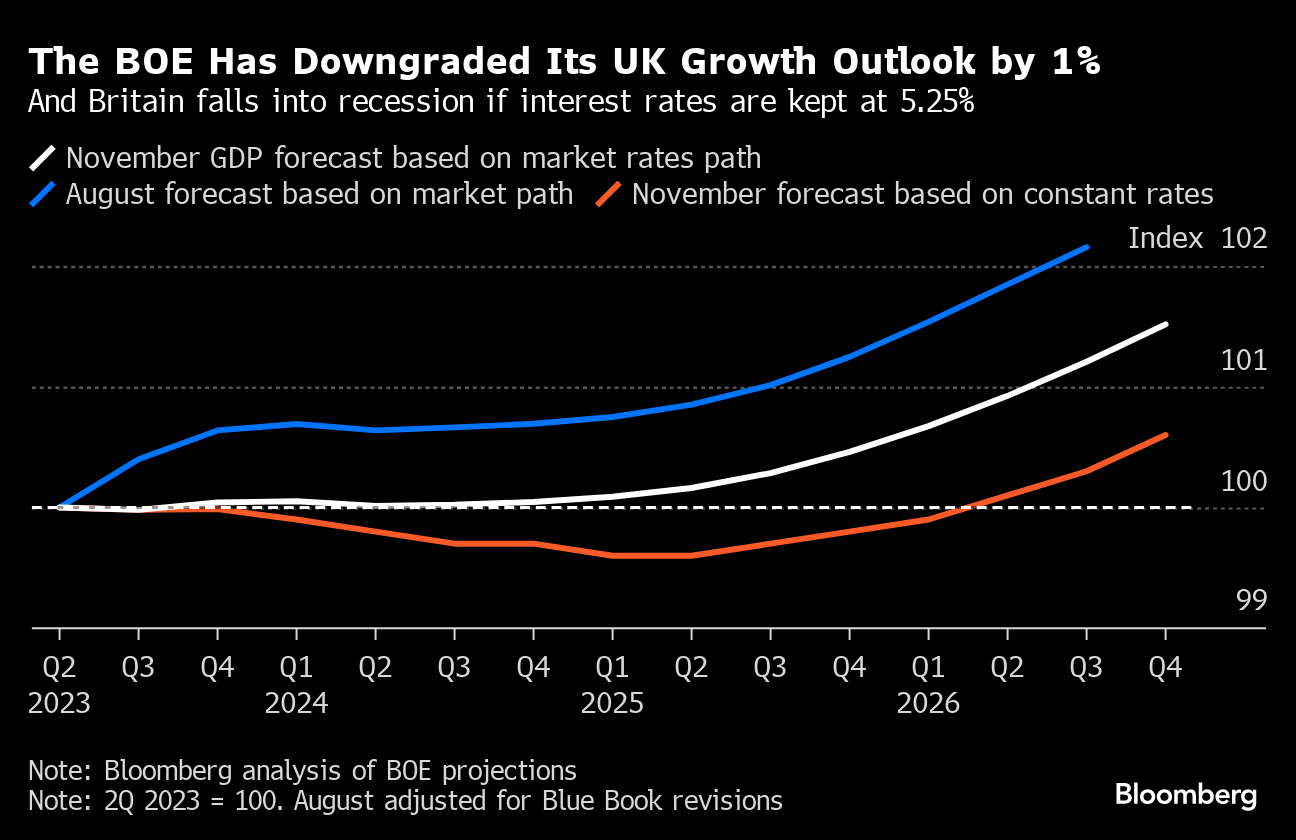

The BOE downgraded growth alongside its rate decision. GDP will be “broadly flat,” with zero growth projected in 2024, down from the 0.5% expansion previously expected. A paltry 0.25% gain is penciled in for 2025.

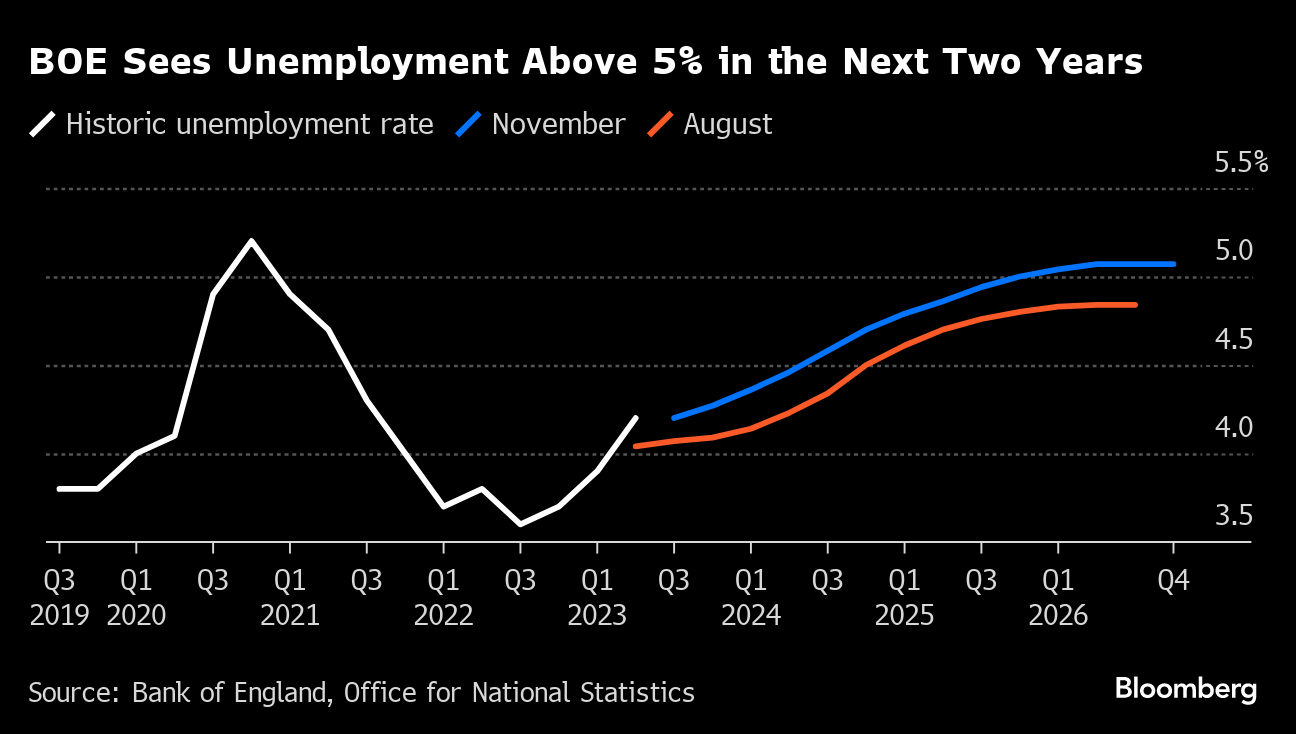

Unemployment will tick up from 4.3% to 5% next year and living standards will stagnate, with post tax household income climbing just 0.25% in 2024. Against that dismal backdrop, Prime Minister Rishi Sunak must call an election by January 2025.

Bailey acknowledged that much of the downturn in the economy stems from the BOE's actions, not energy or food prices. “This forecast reflects the fact that policy is restrictive, and we do see the evidence to support that,” he told reporters in a press conference Thursday. Yet, the central bank believes only half of the full impact of the rate rises has filtered through to the economy so far.

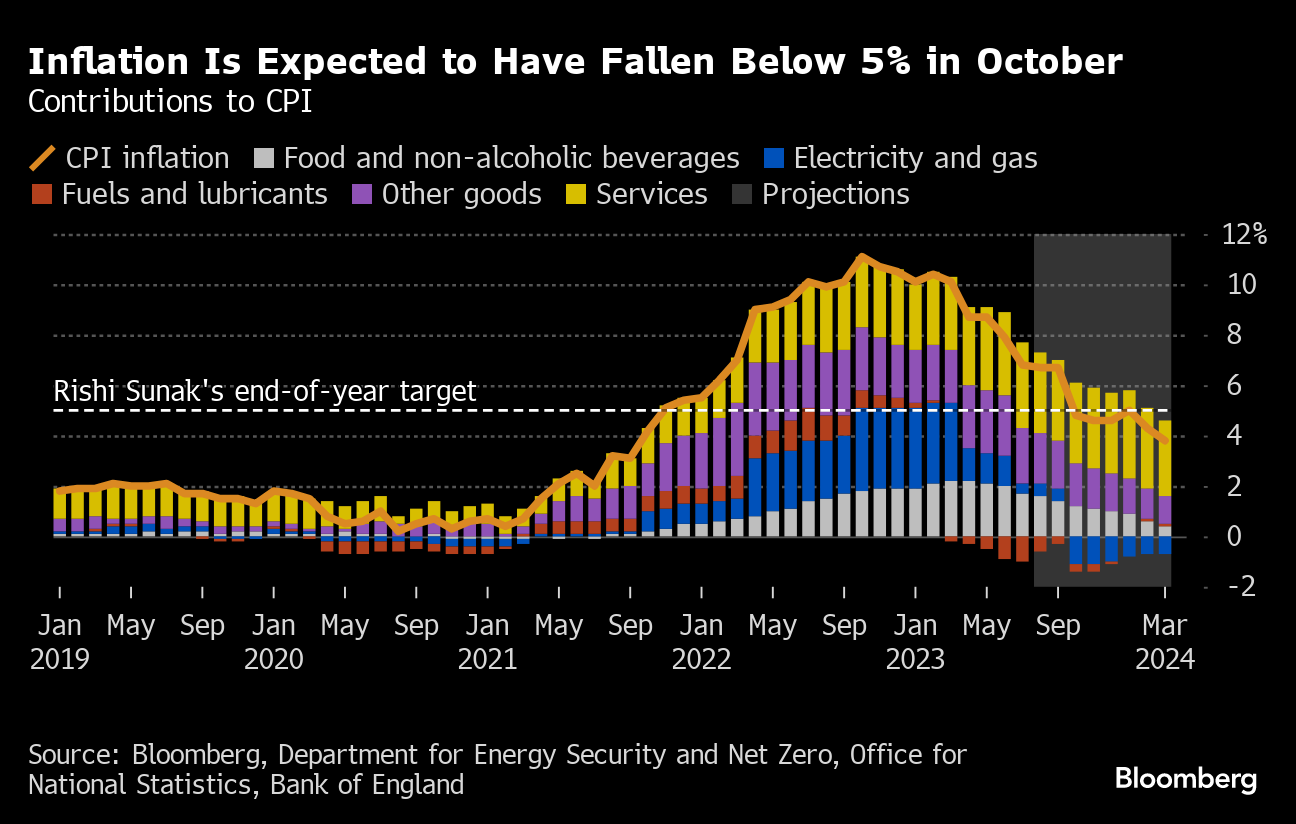

Bailey took credit for a drop in inflation to date. Consumer price growth that peaked at 11.1% last year is now 6.7% and may drop below 5% when October figures are released later this month, he wrote in the Evening Standard newspaper. But inflation is still far above the 2% target, which is why there is “absolutely no reason for complacency,” he told reporters.

For now, the debate at the BOE is about whether to raise rates again. Bailey said there was no discussion this month about a cut because of lingering upside risks for inflation, especially if conflict in the Middle East sends energy prices surging.

Officials also cut their estimate for the supply capacity of the economy, reflecting a shrunken workforce that has contributed to soaring wages. The judgment was among the most important in the forecast, Nomura economists wrote in a note, and helps explain why the nine-member Monetary Policy Committee hasn't yet come around to the market views about rate cuts.

The MPC voted 6-3 for no change this month, with all three dissenters pushing for an increase to 5.5%. Officials strengthened their guidance to stress there will be no easing until inflation is closer to target.

“Policy is likely to need to be restrictive for an extended period of time,” the minutes said. Nomura said the new language was intended to “push back against market pricing for early cuts.”

Bailey pushed back against that reading as well. “If the market has taken from what we have published today a view that we are leaning towards more cuts then I'm afraid I will lean against that,” he said in an interview with Bloomberg TV.

--With assistance from Alice Atkins, Eamon Akil Farhat, Andrew Atkinson, Irina Anghel, Tom Rees and Guy Johnson.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.