In ‘Talking Points This Week', Niraj Shah studies how top business leaders and market makers are navigating the fast-changing financial landscape.

Investors across the world would have begun the new quarter, and in India's case a new financial year, wondering if the fighting in Ukraine, the U.S. Federal Reserve's increasingly hawkish turn, and the higher input costs will engender more volatility and possible losses for stocks and bonds. Note that raw materials are the only key asset class to deliver major gains so far in 2022. While global stocks finished the quarter with their first loss since the pandemic bear market, commodities had their best run in decades during the quarter gone by.

Economies and companies will bear the weight of this steep uptick in costs, as Q4 FY22 results, that will soon be released, will show the impact of this rise in raw material prices. Sure, the first week of earnings in India will be dominated by IT which won't get impacted as much. But come the second half of April, we are likely to start seeing margin jolts. Even if some of these are anticipated, they will cause a drawdown in FY23 earnings estimates. That will form the main talking point for the next few weeks.

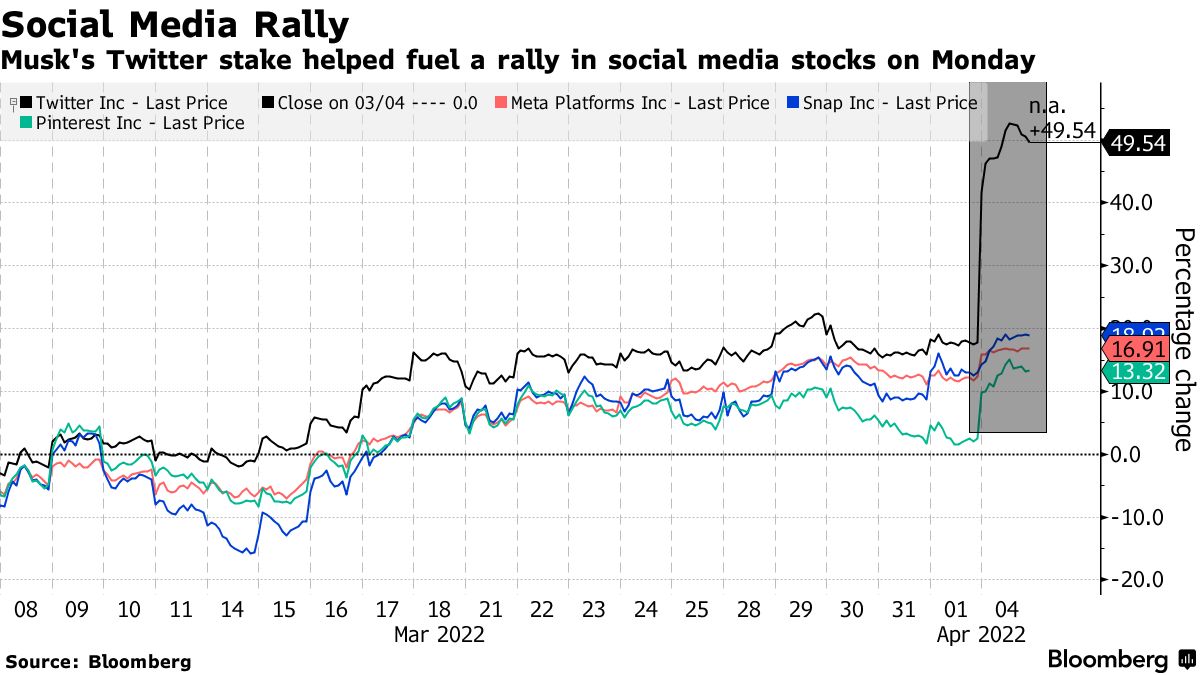

Elsewhere in the world, this week was about Elon Musk and Twitter, and China's mammoth $2.3 trillion infrastructure plan makes other plans look a bit pale.

Central Banks Will Remain Key

The Fed minutes outlined the plan to reduce its balance sheet size. That is the key determinant for liquidity in risk assets. While a 50 basis points hike is now penciled in, if a series of hikes occur along with a swift reduction of the balance sheet size, that may create issues for equities. Elsewhere, the Reserve Bank of Australia dropped its reference to being "patient" and essentially opened the door for a rate increase soon. A number of RBI watchers have said that the Indian central bank will be on that path sooner rather than later, the outcome of the April 8 meeting notwithstanding. Ira's analysis on this would be a good read.

Value Versus Macros

We are now trading with more than 30% discount on European equities versus the U.S. This is an all-time high. If you look at each sector in Europe except pharmaceuticals, you are trading with a heavy discount on the European equities sectors versus U.S. peers, so right now the market has already factored in a lot of bad news, and probably more than what is expected by most of the consensus.Societe Generale

We have heard similar arguments for India versus some other ASEAN markets, where India is way more expensive than the other markets. Yet, if one looks at the first week, despite hiccups midweek, Indian markets haven't really underperformed Asia, nor has Europe outperformed the U.S. markets. Granted, a change in trends takes time, but with the war being fought on their continent and commodity prices playing havoc, it remains to be seen if interest returns to European markets.

If macro data between now and the next Fed meeting stays rosy, the American central bank will likely feel comfortable hiking by 50 basis points and announcing an aggressive rundown of its balance sheet, which may hamper the performance of all equity markets by and large. April tends to be a strong month for U.S. stocks, with its last monthly decline way back in 2012. Will this time be different? How will Asia fare in turn, as there are at least three shocks that are hitting Asia economies at the same time: the tightening of financial conditions led by the Fed hike and reduction of balance sheet leading to a direct credit shock situation and risk aversion or deleveraging; China's zero-Covid policy impacting aggregate demand; and the supply shocks the world at large is facing.

Bank Nifty Returns To The Spotlight

Financials were in focus this week. It started with the HDFC Bank Ltd. quarterly update, which had multiple positives. In addition, updates from Bajaj Finance Ltd., Indusind Bank Ltd., and some others like Federal Bank Ltd. and AU Small Finance Bank Ltd. were all peppered with positives. What, of course, took the cake was the announcement of the merger between HDFC Ltd. and HDFC Bank, which proposes to create a financial behemoth. Ira's Thinkpad note would have all the analysis. I do wish to highlight former RBI Governor D Subbarao's comment on this merger:

I think it is a good thing for the Indian banking system. India wants to upsize its banks to a global scale and it (the merger) will be a good thing for Indian banking, especially private sector banks.D Subbarao, Former RBI Governor

As a result of this announcement, we saw banking aiding the market rally after a really long time. Sure, because the extent of the Nifty pullback from 15,800 levels has been very strong, as the rally fizzled, banks too gave way, but valuations are not egregiously expensive. With a few quarters of stronger asset quality and growth of disbursements, banks may just recover their mojo.

Where Will ITC End Up?

Nikhil Vora, the former IDFC Securities managing director, had famously said in 2012 that cigarette companies around the world would start getting derated because of ESG concerns. A chart from Statista shows the total volume of cigarette sales in the U.S. from 2001 to 2020. 400 billion cigarette sticks were sold in 2001, which has now more than halved.

ITC Ltd.'s numbers in India have not followed a linear trend, as per data provided by the company. After posting volume contraction for all of FY18, the company saw volume growth for seven straight quarters, before Covid-19 hit. Now, after a hiccup that lasted about four quarters, ITC has picked up pace on cigarette volumes, with positive numbers for the last four quarters, with an average of 17.8% for FY22.

How have cigarette stocks performed? The Phillip Morris International Inc. stock price currently is around $100, and its five-year high has been around $120. ITC has a five-year high of Rs 334 in 2017, but has largely remained in the Rs 250 per share range. Similarly, Altria Group Inc. has seen a high of $70 per share but has for long been in the $50 range.

Can its other businesses help ITC recover and breakout from this range or is ITC, like some of its global peers, in a terminal decline?

Did You Know...

The energy sector's share of the S&P 500 market cap has risen from a low of 1.8% in November 2020 to 4.1% in early March, and is now 3.8% compared with a peak of 16% reached in mid-2008, as per a Jefferies note. This ties in with the comments made in a recent op-ed by Ruchir Sharma of Rockefeller International, calling oil the new data. Is it? A conclusive answer to this will be available only by the end of this decade, I reckon.

Niraj Shah is Markets Editor at BloombergQuint.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.