Scan to Download

Indian equity benchmark—NSE Nifty 50—wiped out most of Friday's gain amid F&O expiry and weak global cues due to a sell-off triggered by the US blockade announcement in the Strait of Hormuz.

The 50-stock index declined nearly 1% to settle above 23,800. On Friday, the benchmark index had closed at 24,050.60 on Friday. Meanwhile, the BSE Sensex closed over 700 points lower or 0.97% to end near 77,000.

Meanwhile, Crude prices jumped sharply, with US WTI futures rising more than 7% to $103.66 a barrel. Brent crude advanced 7.2% to $102.05 a barrel. The move takes both key benchmarks above the $100 mark. Elsewhere, US stock futures pared early losses after an initial sell-off triggered by the US blockade announcement in the Strait of Hormuz. Dow futures were down 256 points, or 0.5%. S&P 500 futures fell 0.55%, while Nasdaq 100 futures declined 0.6%.

Eicher Motors and Maruti Suzuki were the top losers in the index, both falling more than 4.5%.

Broader markets outperformed the benchmark, with MidCap 150 down over 0.5% and SmallCap 250 lower by more than 0.3%.

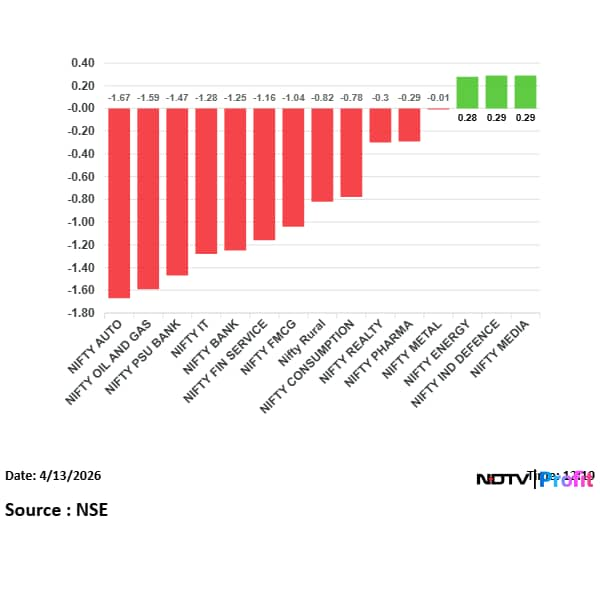

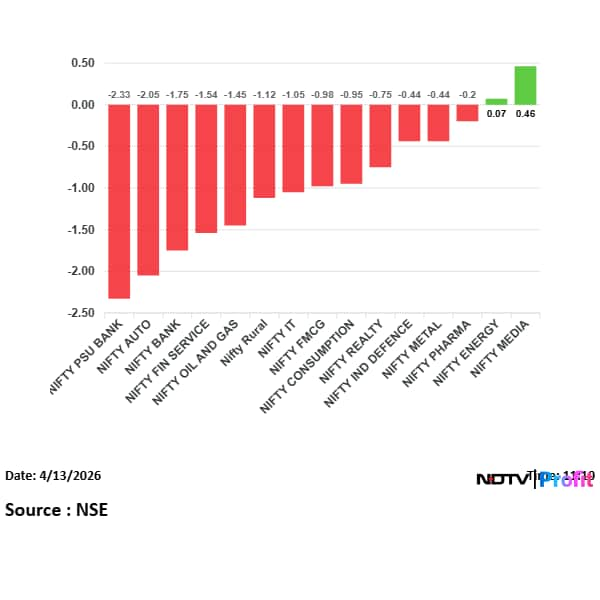

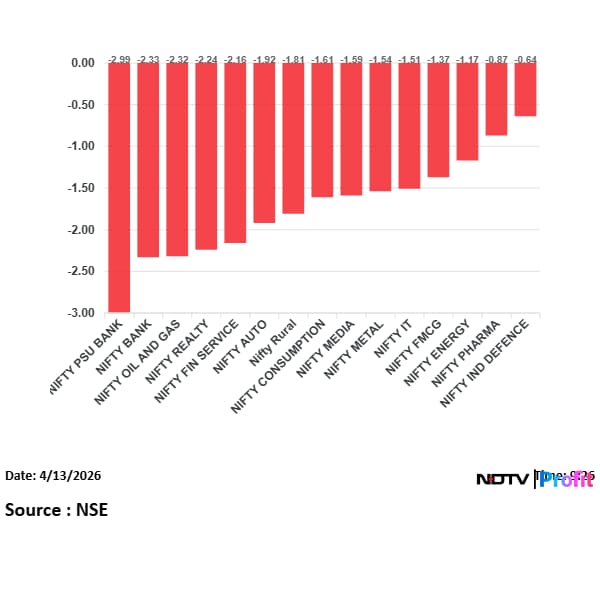

All major sectoral indices ended in the red, led by Nifty Auto, which fell over 2%.

Nifty IT, Oil and Gas, and FMCG declined more than 1%.

Nifty MidCap 150 and SmallCap 250 snapped five-session gaining streaks.

The index fell nearly 1% to close above 23,800, after ending at 24,050.60 on Friday.

BSE Sensex declined more than 700 points, or 0.97%, to close near 77,000.

Brent crude advanced 7.2% to $102.05 a barrel.

The move takes both key benchmarks above the $100 mark.

Dow futures were down 256 points, or 0.5%.

S&P 500 futures fell 0.55%, while Nasdaq 100 futures declined 0.6%.

The company said commercial vehicles have a large share in air pollution, supporting faster electrification.

It added that electrification of school buses could benefit the company.

Olectra said the shift to electric school buses can also help schools lower operating costs.

Put build-up was also visible at 23,600, 23,700 and 24,000 levels.

Fresh call additions were strongest at 23,900, signalling near-term resistance.

Additional call writing was seen at 24,000 and higher strikes, marking further upside hurdles.

Put build-up was also visible at 54,600, 54,800 and 55,200 levels.

Call writing remained highest at 56,000, indicating immediate resistance.

Additional call build-up was seen around 55,700 and 56,500, marking higher resistance zones.

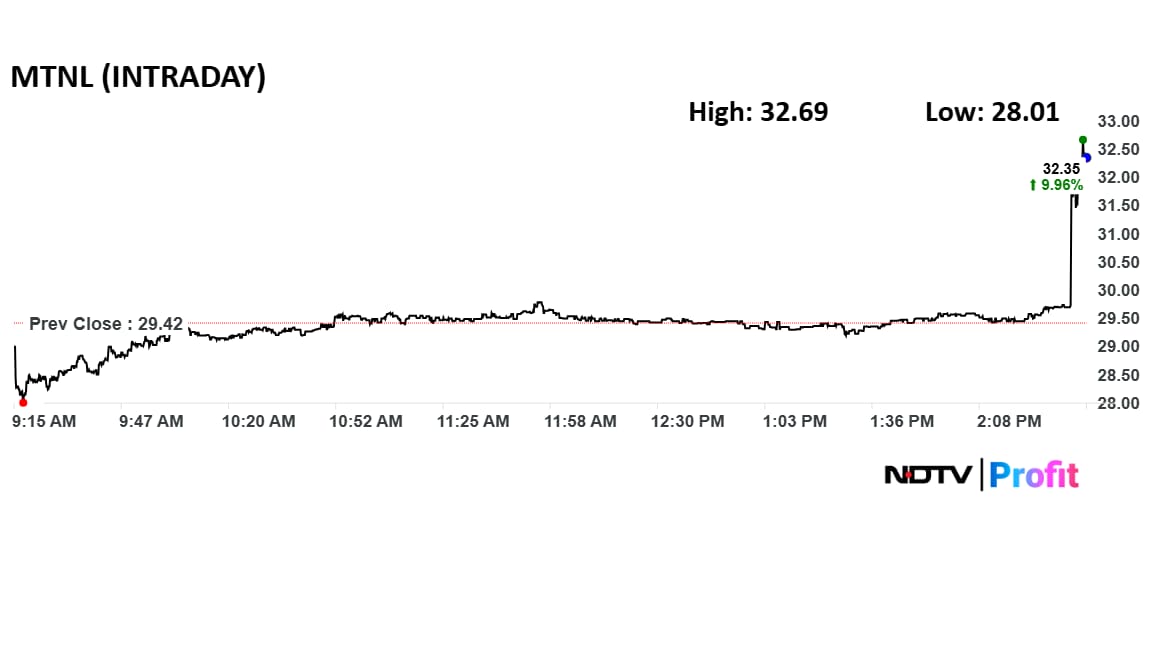

The stock rose as much as 9.96% to Rs 32.35 in intraday trade.

It touched a high of Rs 32.69 and a low of Rs 28.01.

NDTV Profit Exclusive

The government has unlocked over Rs 10,000 crore of assets from BSNL and MTNL under the revival plan.

Asset realisation is estimated at about Rs 7,000 crore for MTNL and around Rs 3,000 crore for BSNL.

Monetisation includes land parcels and other non-core assets across India, including Mumbai.

The proceeds are expected to be used to service MTNL debt and clear bank dues.

The impact is likely to reflect in balance sheets over the next 30-45 days.

Spain’s IBEX 35 fell 1.29%, while France’s CAC 40 declined 1.04%.

Germany’s DAX dropped 1.02% and Italy’s FTSE MIB was down 0.85%.

The STOXX Europe 600 slipped 0.76%, while the UK’s FTSE 100 fell 0.44%.

Under existing rules, the floor price is based on the higher of the two-week or 26-week average share price.

Market participants said this has left issue prices above current market levels after the recent correction.

Several planned QIPs have been delayed, reduced or shelved due to weak investor demand.

Industry participants are seeking a shorter pricing look-back period and greater flexibility during market weakness.

Put build-up was also visible at 23,600 and 23,700, strengthening the lower support zone.

Call writing remained concentrated at 23,900 and 24,000, pointing to resistance on the upside.

Highest put open interest stood at 23,800, while call open interest was strongest near 24,000.

Sensex was down 545 points, or 0.7%, at 77,004, while Nifty fell 0.7% to 23,865.

Earlier in the session, Nifty had dropped as much as 2% to 23,555 and Sensex fell 2.2% to 75,868.

Hang Seng fell 0.9%, while South Korea’s Kospi declined 0.86%.

Japan’s Nikkei dropped 0.74% and Australia’s ASX 200 slipped 0.39%.

China’s Shanghai Composite was the outlier, rising 0.06%.

The Middle East accounts for about 9% of global aluminium output, keeping the market focused on potential disruptions.

Elevated prices are weighing on demand in China, where inventories have climbed to the highest level since 2020.

The bloc also sought full and effective implementation of the ceasefire in the Middle East.

ASEAN urged the US and Iran to continue talks aimed at ending the conflict.

Source: Bloomberg

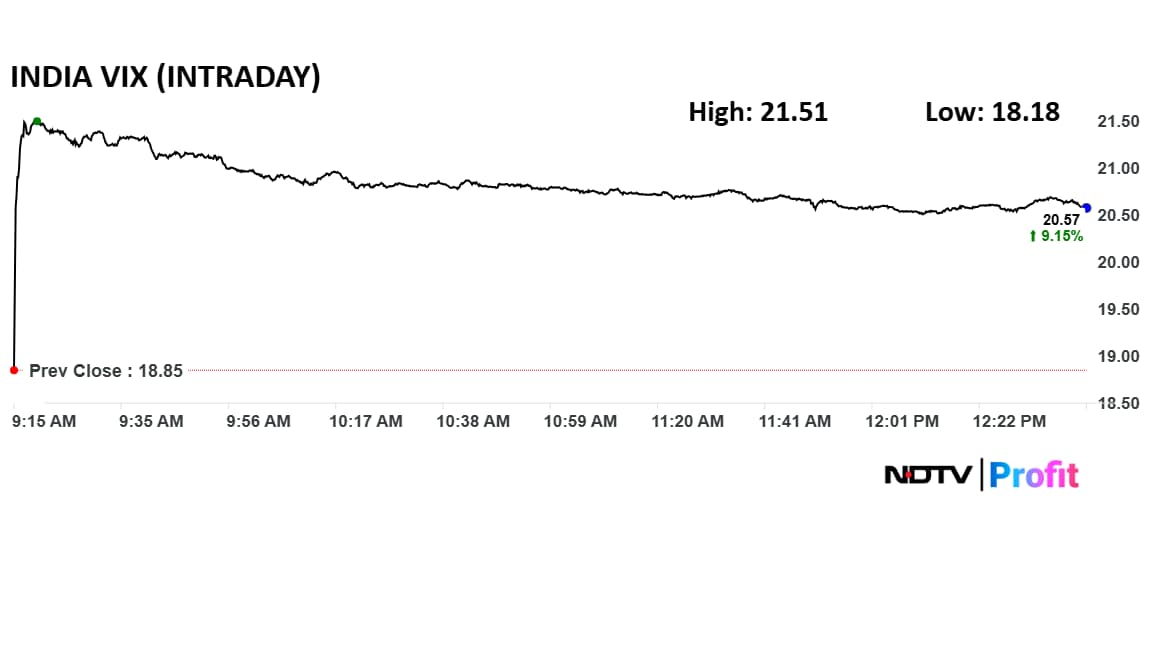

India VIX rose 9.15% to 20.57 in intraday trade. The volatility gauge touched a high of 21.51 and a low of 18.18.

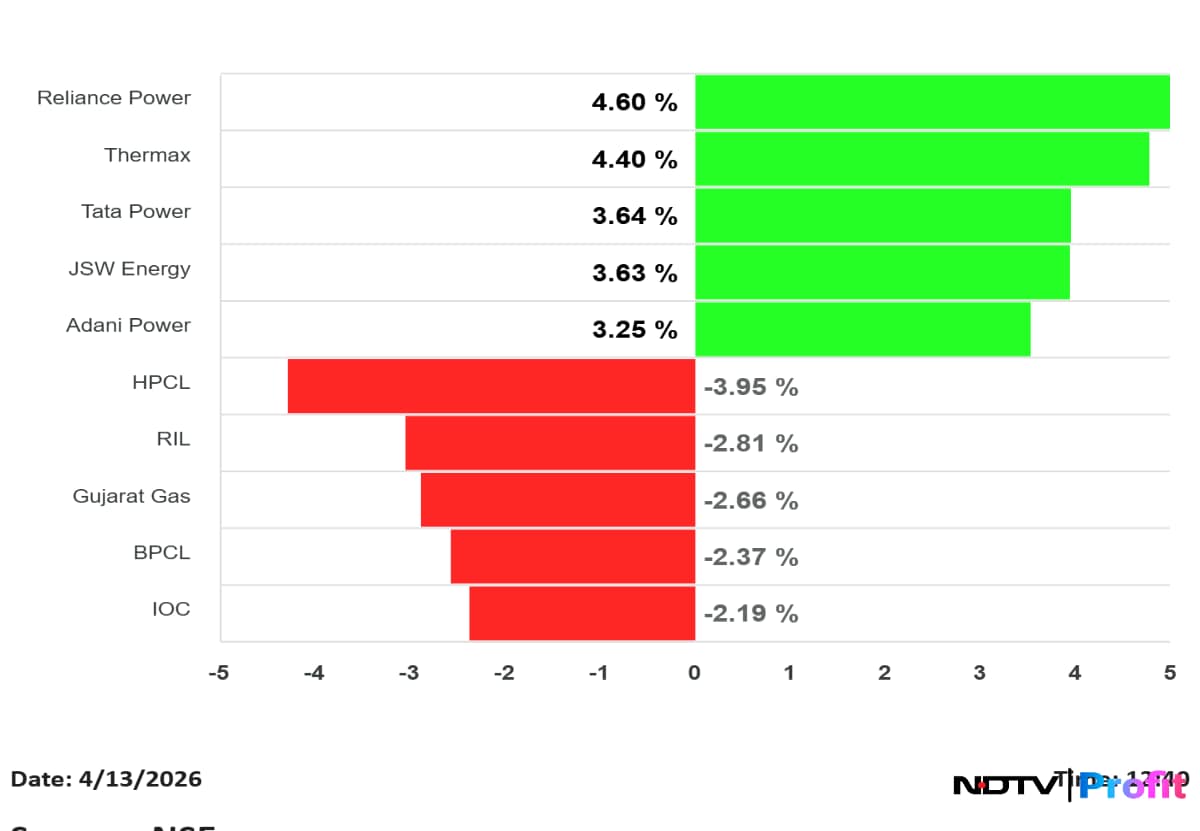

Tata Power, JSW Energy and Adani Power were also among the top gainers.

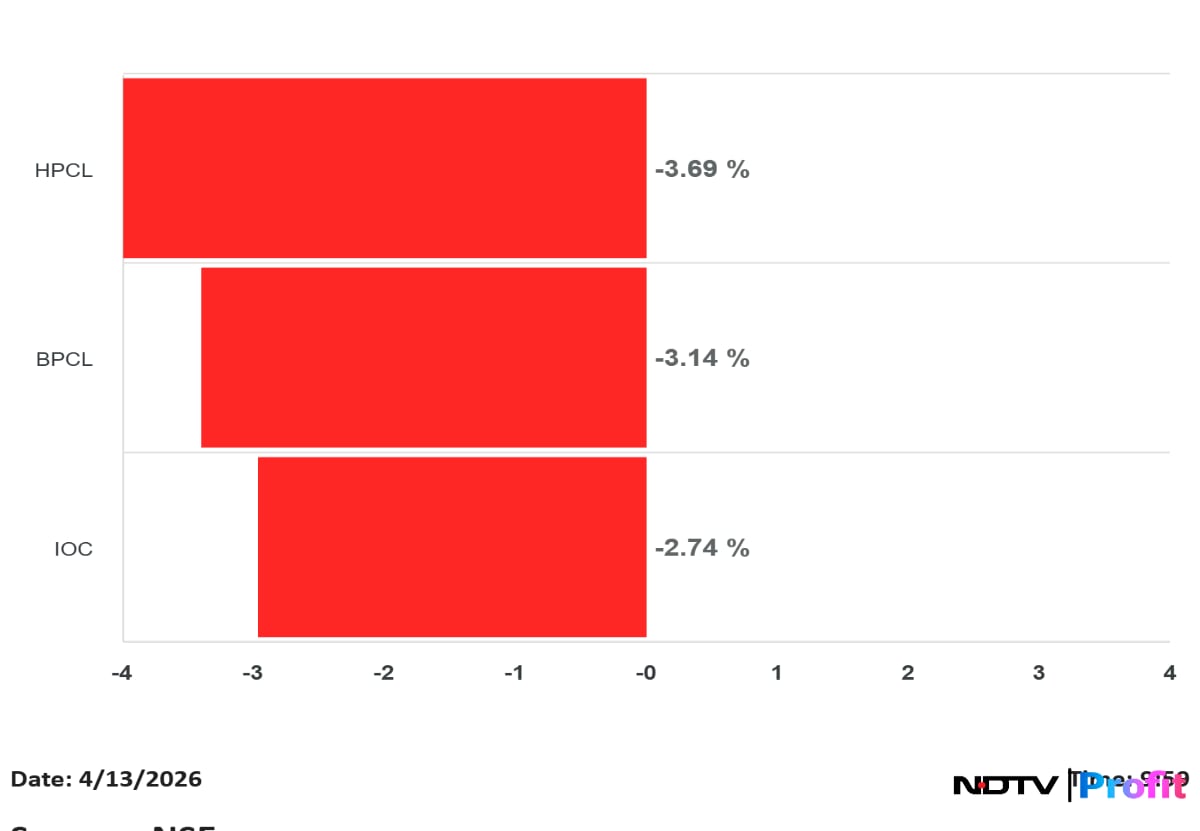

HPCL was the worst performer, falling 3.95%.

Reliance Industries, Gujarat Gas, BPCL and IOC were among other key losers in the index.

Nifty Auto was the worst performer, falling 1.7%.

Oil and Gas, PSU Bank, IT and Bank indices also traded in the red.

Nifty Media was the top gainer, rising 0.3%, while Energy and Defence indices also edged higher.

HDFC Life Insurance and JSW Energy saw short covering.

Samvardhana Motherson International and State Bank of India witnessed long unwinding.

Fresh short build-up was seen in Eicher Motors and Bank of India, signalling new bearish bets.

Passenger traffic averaged 4.5 lakh per day, compared with 4.73 lakh in March.

Airline stocks, including IndiGo, may be in focus on softer traffic trends.

Nifty PSU Bank was the worst performer, falling 2.3%.

Auto, Bank, Financial Services and Oil and Gas indices were also under pressure.

Nifty Media was the top gainer, rising 0.5%, while Nifty Energy edged higher.

One vessel is anchored near Sikka on the west coast, while another is near Paradip on the east coast.

Each tanker is carrying about 2 million barrels of Iranian crude.

The development comes after the US announced a blockade targeting Iranian shipments following failed peace talks.

Markets will watch whether the move affects existing waivers and future crude purchases.

Source: Bloomberg

Police reported arson, vandalism and stone-pelting in Phase-2 and Sector 60 areas.

A vehicle was set on fire and property was damaged during the unrest.

Traffic movement was affected, causing disruption for commuters in nearby areas.

Source: PTI

The complaint said one executive harassed and followed her, while others did not act on her grievance.

She also alleged she was transferred to Dubai against her wishes after raising the issue.

The company said she was advised to file the complaint through the internal POSH committee, but she approached the police.

No arrests have been made and the investigation is continuing.

Source: Pune Mirror

The USFDA has issued a 'voluntary action indicated' status for Piramal Pharma's Lexington unit after inspection.

Source: Exchange Filing

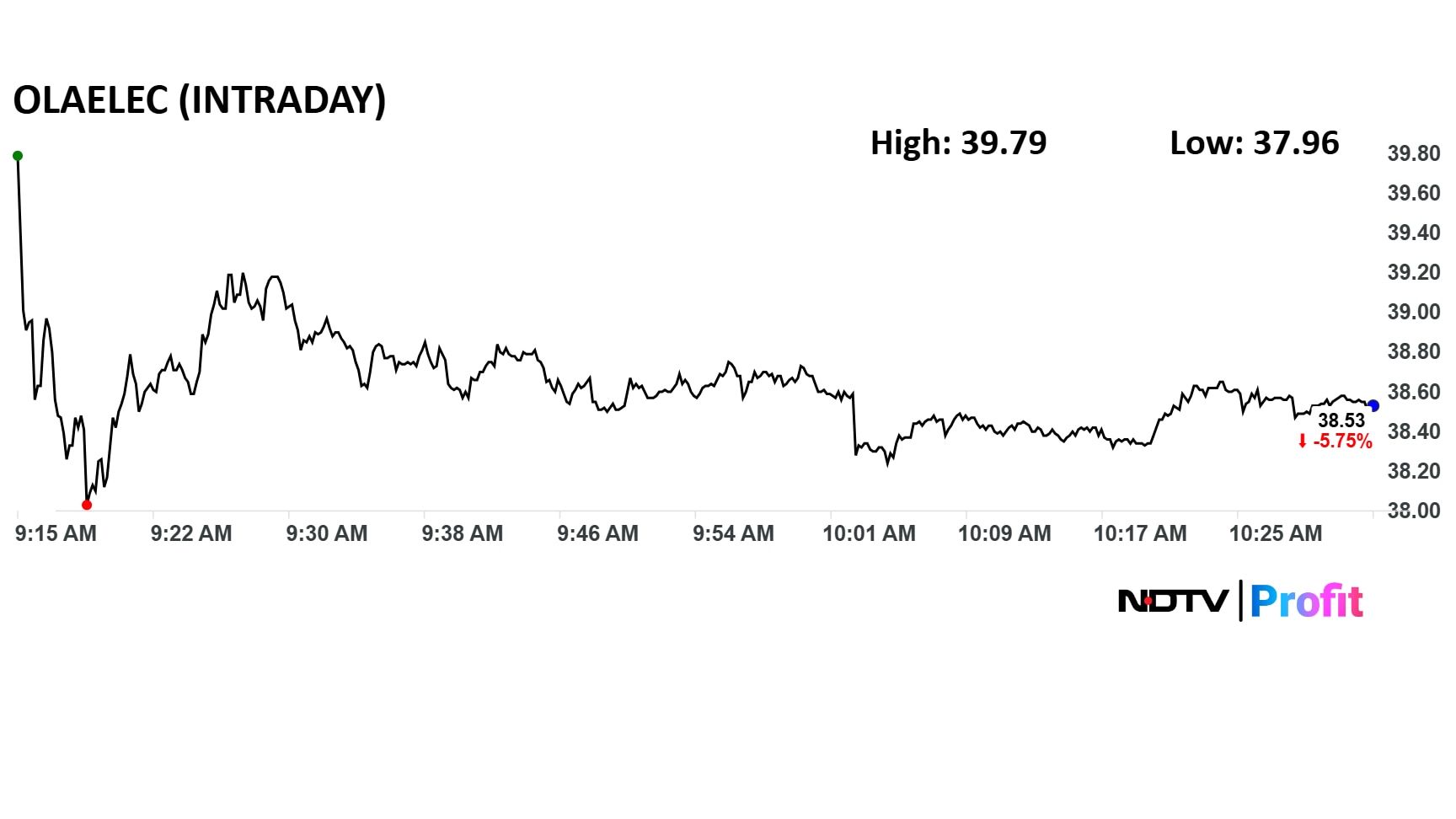

Ola Electric Mobility Ltd. shares dropped over 7% during early trade on Monday, on likely profit booking after three sessions of significant gains. The total traded volume stood at 3.5 times the 30-day average and the turnover was Rs 625 crore on the NSE.

On Friday, the stock closed 12.6% higher, on Thursday 20% and Wednesday 5%. The stock has fallen 23% in the last 12 months and 55% year-to-date.

Open interest increased in both indices, indicating active positioning during the decline.

HDFC Bank, ICICI Bank, Infosys, TCS and Kotak Mahindra Bank saw open interest additions.

SBI and Bharti Airtel saw open interest reduction, signalling some position unwinding.

Futures data points to selective stock-specific activity amid broader market weakness.

Donald Trump said the United States will blockade ships entering or exiting Iranian ports from April 13 at 10:00 a.m. ET.

Union Bank, Bank of India and PFC were also among stocks witnessing new bearish positions.

National Aluminium, Coal India and KEI Industries featured among other names with rising short positions.

MCX, Supreme Industries and Torrent Pharma also saw positions unwind on the short side.

Call writing was concentrated at 23,700 to 24,000, pointing to resistance on any rebound.

Highest put open interest stood near 23,500 and 23,600, while call base remained strong at 24,000 and above.

HPCL fell 3.69%, BPCL declined 3.14% and IOC dropped 2.74%.

Defensive positioning is shifting towards pharma and IT as near-term shelters amid volatility.

Some investors have also increased cash holdings to navigate market swings.

Experts said the duration of uncertainty, rather than short-term price moves, will be key for markets.

They added that domestic cyclical sectors may see stronger recoveries once conditions stabilise.

Read more here.

The revised emission curve allows slightly higher fuel consumption than the earlier September 2025 draft.

The framework retains phased tightening of norms through FY32.

EV and hybrid credits can be used to offset penalties, with trading between companies also permitted.

Higher-emission vehicles may face financial penalties under the proposal.

Companies selling fewer than 1,000 units may be exempt from compliance norms.

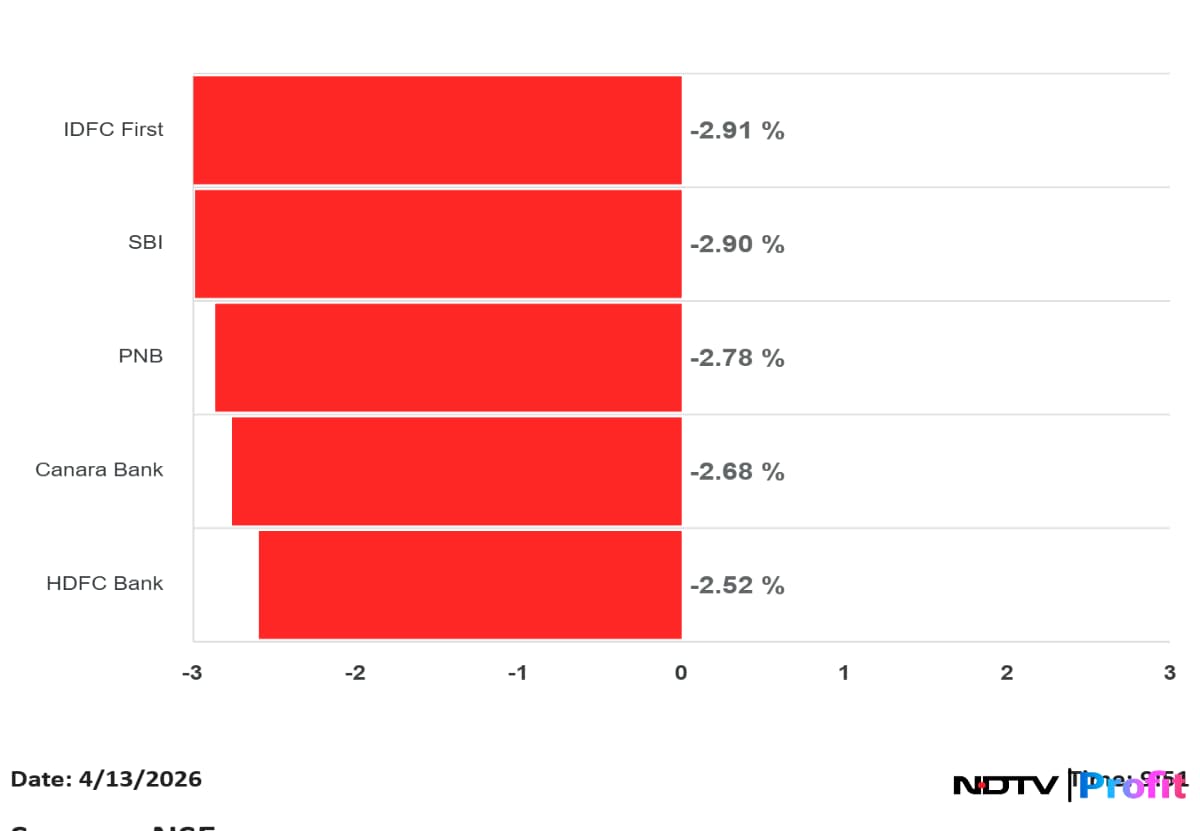

SBI declined 2.90%, while Punjab National Bank dropped 2.78%.

Canara Bank and HDFC Bank also fell, weighing on the Nifty Bank index.

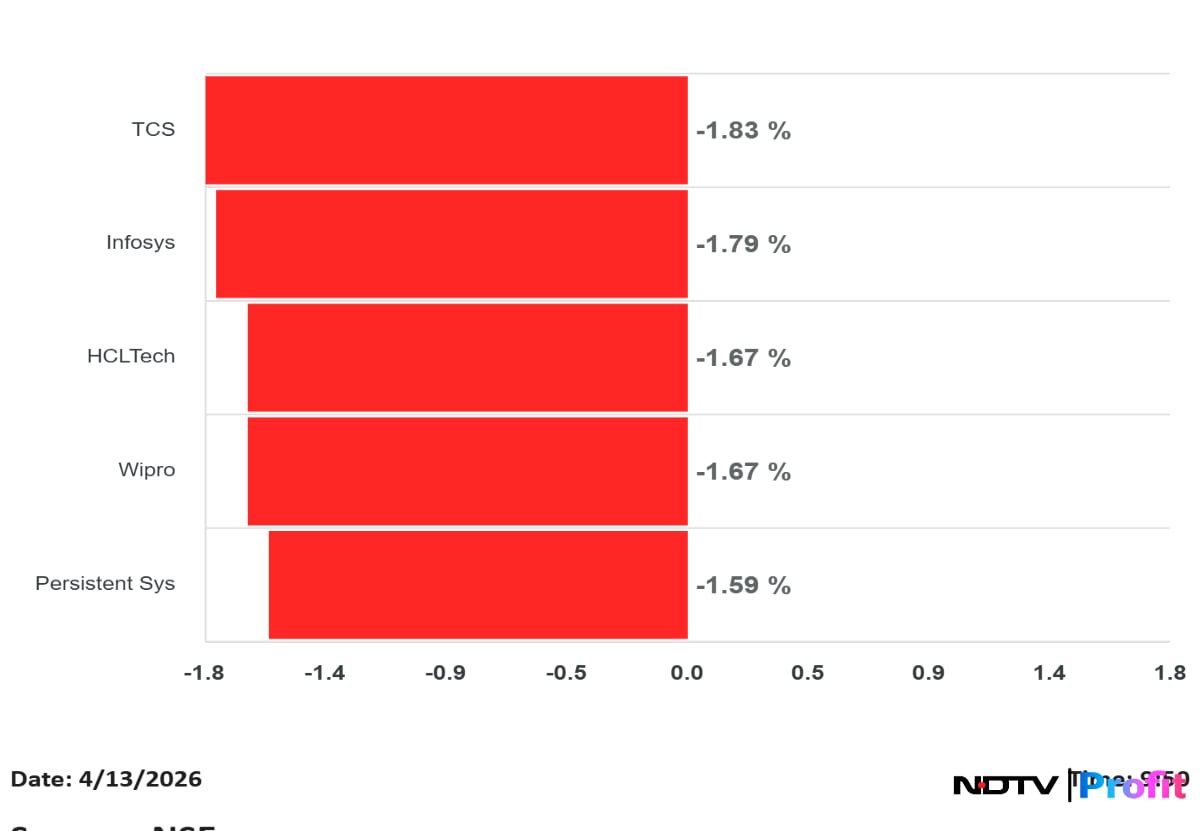

HCLTech and Wipro declined 1.67% each, while Persistent Systems fell 1.59%.

Broad weakness across frontline IT names weighed on the Nifty IT index.

Trading volume was 12 times the 20-day average.

The relative strength index stood at 73, indicating overbought conditions.

Trading volume was nearly four times the 20-day average.

The stock had risen 32% in the last five days and 67% over the past 30 days.

The relative strength index was above 70, indicating the stock had entered overbought territory.

SBI and Infosys were also among the top contributors to the index decline.

Financial heavyweights led the downside pressure on the benchmark.

Nifty PSU Bank was the worst performer, falling 3%.

Bank, Oil and Gas, Realty and Financial Services indices were also among the top losers.

Nifty fell as much as 2% to 23,555

Sensex fell as much as 2.2% or 1,681 points to 75,868

The local currency fell as much as 60 paise to 93.33 in early trade.

The move comes amid pressure from higher crude prices and weak global risk sentiment.

Sensex fell nearly 1,900 points in early indications.

The move signals broad pressure at the open amid weak global cues.

The policy proposes timelines to phase out ICE two-wheelers and three-wheelers in the city.

The brokerage said this could be negative for legacy auto makers if other cities adopt a similar model.

It said implementation may be challenging if buyers shift purchases to NCR markets.

Electric cars priced up to Rs 30 lakh may get road tax and registration fee waivers, while strong hybrids may receive a 50% waiver.

It said the revised framework balances stakeholder interests and keeps FY28 EV targets achievable.

The brokerage said the changes are particularly positive for Mahindra & Mahindra and Hyundai.

It said both companies may find it easier to meet norms without changing product plans to launch hybrids.

Maruti Suzuki and Toyota may need to reassess the viability of hybrid launches under the new framework.

The brokerage cited resilient domestic volumes and continued international scale-up.

It raised FY27 and FY28 volume and earnings estimates, driven by NQXT consolidation.

It said near-term volume disruption may be offset by growth drivers including higher transshipment and stronger coal volumes.

A move above 24,100 is seen as the trigger for further upside.

Immediate support is placed at 23,450–23,100 if markets consolidate.

Bank Nifty is also seen in a bullish setup, with upside levels at 57,300 and 58,000 above 56,300.

Support for Bank Nifty is seen at 53,000–54,000.

It cited parent backing, product pipeline and expansion plans as key growth drivers.

The brokerage said proprietary technology access and differentiated products support its market position.

It highlighted return on capital employed above 18% and low leverage.

It also expects growth from planned capacity expansion and new product launches in FY26.

ONGC and Oil India may react after Brent crude rose following failed ceasefire talks.

RBL Bank plans to issue 90.95 crore equity shares to Emirates NBD at Rs 280 per share.

Tata Power and EV-linked stocks may see action on the New Delhi EV policy draft.

Garware Hi-Tech and Arvind are in focus after textile PLI clearance.

Himadri Specialty and Neogen Chemicals may track plans for a lithium processing support scheme.

Enviro Infra, Advait Energy, Zaggle, Panacea Biotech and Texmaco are in focus on order wins.

Swiggy will be watched after co-founder Nandan Reddy stepped down.

Maruti Suzuki, Bosch and Subros may react to Haryana’s minimum wage increase.

Fertiliser stocks may remain under pressure after reports China may ban sulphuric acid exports.

Swaraj Engines has the highest projected payout at Rs 109.2 per share, followed by CRISIL at Rs 74.8 and HDFC AMC at Rs 54.68, based on Bloomberg estimates.

HDFC Bank may announce Rs 13.43 per share, while ICICI Lombard is seen at Rs 14.34.

Muthoot Finance is the key ex-dividend stock this week, with shares turning ex-dividend on April 17. The company has announced an interim dividend of Rs 30 per share for FY26.

Read more here.

Asian markets opened lower, while rising global bond yields added to pressure on equities.

A weaker rupee opening is expected as higher crude prices may weigh on sentiment.

Foreign investors were buyers in the cash market after 27 sessions, while short positions in index futures eased to 78% from 80%.

Nifty weekly expiry may add volatility today.

Markets will remain shut tomorrow for Ambedkar Jayanti.

The brokerage cited parent support, product pipeline and expansion plans as key growth drivers.

It said access to proprietary technology and differentiated products strengthens the company’s position in the agrochemical market.

The brokerage highlighted return on capital employed above 18% and low leverage.

It added that the company plans up to Rs 400 crore of expansion spending and expects new product launches in FY26.

It also started Clean Max with a buy rating and target price of Rs 1,150.

The brokerage said renewable energy is nearing a new growth phase, with execution now more important than access to capital.

It expects Acme Solar’s contracted capacity to support earnings visibility and sees EBITDA CAGR of 72% over FY26–28.

For Clean Max, it expects strong demand as companies shift to lower-cost green power and sees EBITDA CAGR of 60% over FY26–28.

Copper and aluminium prices are up 35% and 29% YoY, while HDPE prices rose 46% in March.

New energy efficiency norms are adding further pressure on production costs.

Companies have raised prices across categories, with room air conditioners up 5–15%, fans about 5%, and refrigerators and washing machines up 3–5%.

Blue Star, Voltas, LG Electronics, Hitachi, Crompton Greaves Consumer and Whirlpool are among companies in focus.

The full impact on volumes and margins may be visible from Q1FY27 after existing inventory is exhausted.

IMD’s monsoon forecast is due, a key trigger for agriculture, rural demand and inflation-sensitive sectors. Private forecaster Skymet has projected below-normal rainfall.

Q4 earnings due from ICICI Prudential Asset Management, Swaraj Engines and Just Dial.

NSE will start trading in dated Brent crude oil (Platts) futures contracts.

OPEC monthly report will be watched for supply and demand signals.

US home sales data is due later in the day.

Source: Reuters, Al Jazeera and Associated Press

Donald Trump said the US will blockade the Strait of Hormuz after talks with Iran ended without a resolution.

He also said the US Navy would seek and interdict vessels linked to Iranian trade, signalling further escalation in the region.

The Dow Jones Industrial Average declined 269.23 points, or 0.56%, to close at 47,916.57.

The Nasdaq Composite rose 0.35% to 22,902.89, helped by gains in semiconductor stocks such as Nvidia and Broadcom.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.