Hello and welcome to our live coverage of stock markets.

Indian equity benchmarks declined for the fifth straight week, marking their longest weekly losing streak since the week ending August 10, 2025. In the holiday-shortened week, the Sensex fell 1.2% and the Nifty dropped 1.3%. On Friday, the Sensex slumped 2.3%, or nearly 1,700 points, to close near 73,600. The Nifty fell 2.1% to end marginally above 22,800.

Meanwhile, Oil prices fell as tensions eased in the conflict that has lasted nearly a month. West Texas Intermediate crude dropped 1.5% to $93.07 a barrel, while Brent crude futures fell 0.7% to $100.57 a barrel. Elsewhere in Europe, The pan-European Stoxx 600 fell 0.8%, tracking losses in Aisan markets earlier in the day and overnight Wall Steet's slump. Germany's DAX opened 0.9% lower, while France's CAC 40 dropped 0.5%. The UK's FTSE 100 also opened lower, down 0.35%.

Stock Market Wrap: Rupee Ends Week At Record Low Of 94.75 Per Dollar

- The rupee depreciated by 1.04 against the US dollar during the week.

-

It ended the week at a record low of 94.75 per dollar.

Stock Market Crash Highlights: Nifty, Sensex Register Longest Weekly Losing Streak In Over Seven Months

- Indian equity benchmarks declined for the fifth straight week, marking their longest weekly losing streak since the week ending August 10, 2025. In the holiday-shortened week, the Sensex fell 1.2% and the Nifty dropped 1.3%.

-

On Friday, the Sensex slumped 2.3%, or nearly 1,700 points, to close near 73,600. The Nifty fell 2.1% to end marginally above 22,800.

-

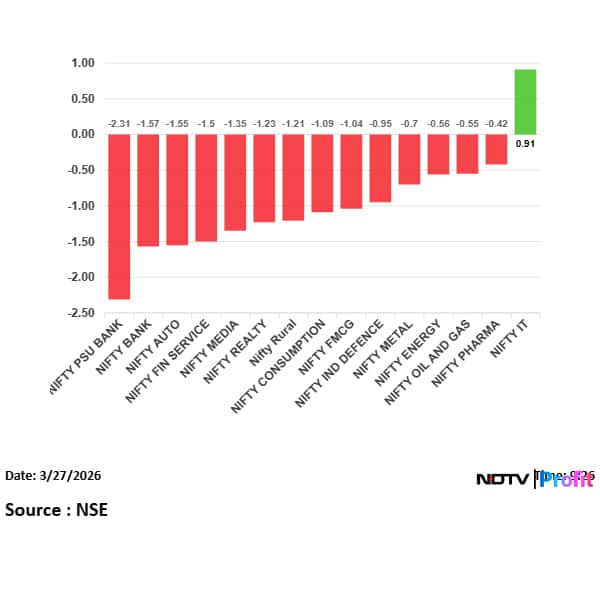

All NSE sectoral indices closed lower, with Nifty PSU Bank leading the losses with a 3.9% fall.

Stock Market Live: Nifty Extends Losing Run To Fifth Week; IT Only Sectoral Gainer

- Nifty ended the week down over 1% and closed in the red for the fifth straight week. BEL and Trent were the top losers in the index, both down over 5%.

-

The broader market also ended lower. Nifty Midcap 150 fell 1.5% for the week and closed in the red for the fifth week in a row, while Nifty Smallcap 250 lost nearly 1% and declined for the sixth straight week. IDBI Bank and Gujarat Gas were the top losers in Nifty Midcap 150, both down over 11%. Firstcry and Chennai Petro were the top losers in Nifty Smallcap 250, both down over 10%.

-

All sectoral indices ended lower for the week except Nifty IT. Nifty India Defence was the worst-performing sector, down over 4%, with GRSE and BDL falling over 9%. Nifty IT rose over 1% and gained for the second week in a row, led by Coforge and Oracle Fin, both up over 5%.

-

Nifty Realty fell for the seventh straight week. Nifty Bank, Nifty Fin Service and Nifty FMCG declined for the fifth week in a row, while Nifty Oil & Gas fell for the fourth straight week and Nifty Pharma ended lower for the third consecutive week. Nifty FMCG marked its lowest weekly close since April 2023, while Nifty Realty posted its lowest weekly close since November 2023.

Stock Market Live: Adani Ports Starts Operations At India’s First Refuge Port For Maritime Safety

- Adani Ports and SEZ has started operations at India’s first refuge port for maritime safety, according to an exchange filing.

-

The update puts the port operator in focus.

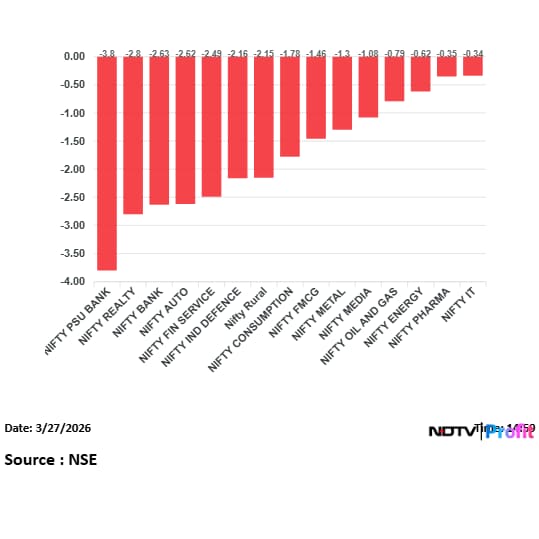

Stock Market Live: All NSE Sectoral Indices Fall; PSU Bank Leads Losses

- All sectoral gauges compiled by the NSE traded lower in the session.

-

Nifty PSU Bank was the worst-performing sectoral index, falling 3.8%.

-

Nifty Realty, Nifty Bank, Nifty Auto and Nifty Fin Service were also among the main losers.

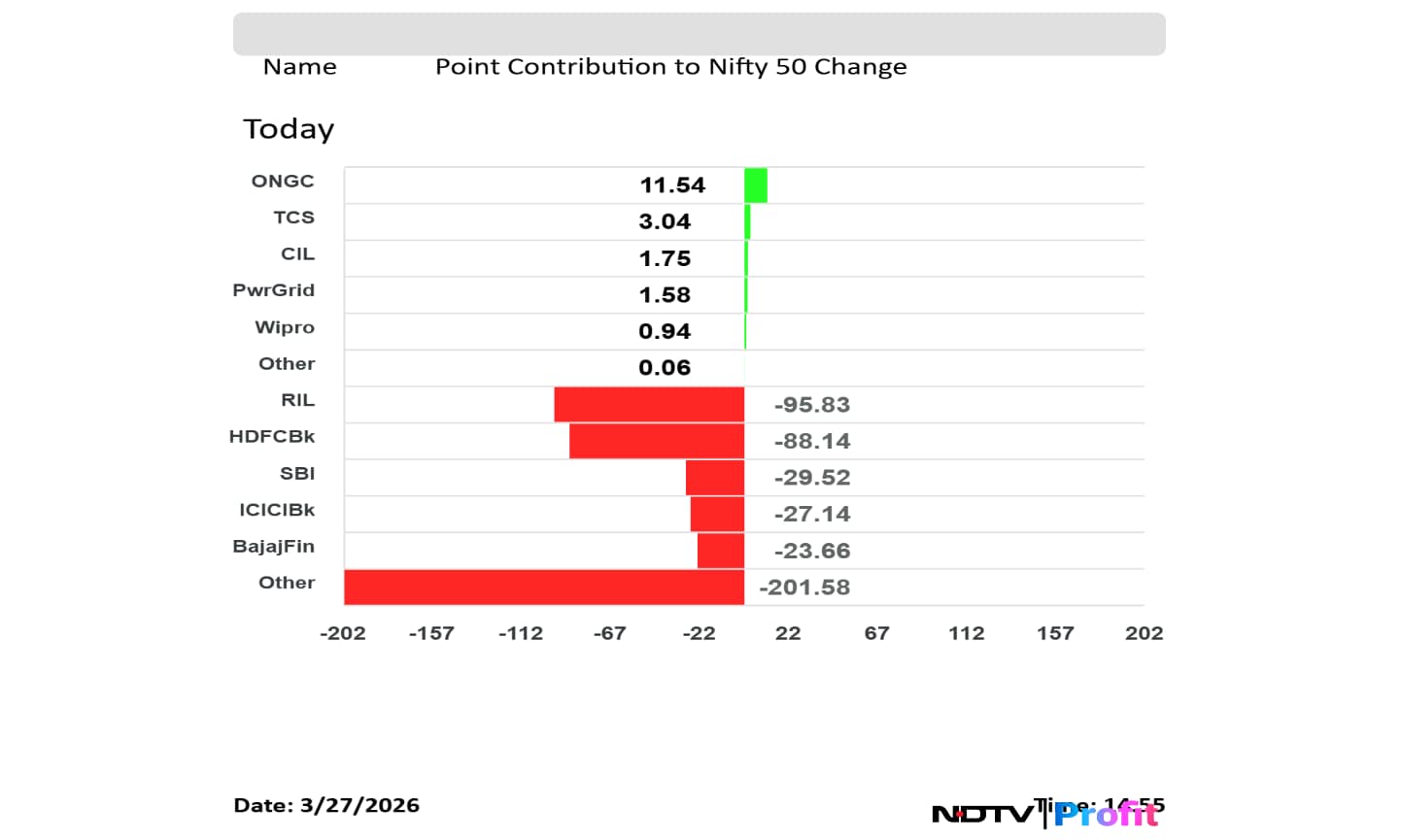

Stock Market Live: ONGC, TCS Lead Nifty Gainers; Reliance, HDFC Bank Weigh Most

- ONGC was the top positive contributor to the Nifty, adding 11.54 points. TCS, Coal India, Power Grid and Wipro also supported the index, contributing 3.04, 1.75, 1.58 and 0.94 points respectively.

-

Reliance Industries was the biggest drag on the Nifty, pulling down the index by 95.83 points. HDFC Bank, SBI, ICICI Bank and Bajaj Finserv also weighed on the index, with contributions of 88.14, 29.52, 27.14 and 23.66 points respectively.

Stock Market Live: Nifty Falls Below 22,850; Sensex Drops 1,652 Points

- Nifty fell as much as 2.04% to 22,831 in trade.

-

Sensex declined as much as 2.2%, or 1,652 points, to 73,621.17.

Stock Market Live: Nifty Falls Below 22,900; Sensex Drops Nearly 1,500 Points

- Nifty fell as much as 1.8% to 22,884 in trade.

-

Sensex declined as much as 2%, or 1,480 points, to 73,792.52.

Stock Market Live: Stoxx 600, DAX, CAC 40 And FTSE 100 Open Lower In Europe

- The pan-European Stoxx 600 fell 0.8% shortly after the opening bell.

-

Germany’s DAX opened 0.9% lower, while France’s CAC 40 dropped 0.5%.

-

The UK’s FTSE 100 also opened lower, down 0.35%.

Stock Market Live: Hang Seng, Shanghai Close Higher; Nikkei, Kospi And ASX 200 End Lower

- Hong Kong’s Hang Seng rose 0.38% to 24,951.88, while Shanghai gained 0.63% to 3,913.724.

-

Japan’s Nikkei 225 fell 0.43% to 53,373.07 and South Korea’s Kospi declined 0.40% to 5,438.87.

-

Australia’s ASX 200 also closed lower, down 0.11% at 8,516.30.

Stock Market Live: What Does Infosys Stand To Gain From Deals In US Healthcare Market? Expert Weighs In

Stock Market Live: IREDA Declares Interim Dividend Of Rs 0.60; Sets Record Date

Stock Market Live: ONGC, LIC Housing Finance See Long Build-Up; Tata Motors PV, Sona BLW In Short Build-Up

- Oil & Natural Gas Corporation and LIC Housing Finance saw long build-up in trade.

-

Oracle Financial Services Software and Sammaan Capital saw short covering.

-

NBCC (India) and PG Electroplast saw long unwinding.

-

Tata Motors Passenger Vehicles and Sona BLW Precision Forgings saw short build-up.

Stock Market Live: Singapore's DBS Group Joins Buzzing India Market With Mandate In Manipal Health IPO

Stock Market Live: Kaynes Tech Eyes Rs 500 Crore Boost From India's Reported $11 Billion Chip Fund

Stock Market Live: Dr. Reddy’s To Rename Semaglutide Drug Olymra After Olymviq Dispute

- Dr. Reddy’s Laboratories will change the name of its semaglutide drug from Olymviq to Olymra.

-

The update came after the earlier dispute over the Olymviq brand name.

Stock Market Live: Coal India To Set Up Eight Coking Coal Washeries For Rs 3,300 Crore

- Coal India will set up eight coking coal washeries at a cost of Rs 3,300 crore, according to an exchange filing.

-

The company expects the washeries to become operational by 2030.

-

Total coal washeries capacity will be 21.5 million tonnes a year.

Stock Market Live: Hardeep Puri Says Rumours Of Nationwide Lockdown Are False

- Union Minister Hardeep Singh Puri said rumours of a nationwide lockdown are false and added that no such proposal is under consideration by the government.

-

Puri said the government is monitoring developments in energy, supply chains and essential commodities in real time.

-

He said steps are being taken to ensure uninterrupted availability of fuel, energy and other critical supplies, and added that India is prepared to handle emerging challenges.

Stock Market Live: ACME Solar Jumps 8% After Incred Initiates Coverage

- ACME Solar rose as much as 8% to Rs 274.35 after Incred initiated coverage with a Buy rating and a target price of Rs 319.

-

Incred said ACME Solar is moving from a mid-sized solar developer to a firm and dispatchable renewable energy player. It said 49% of the portfolio is in firm and dispatchable renewable energy.

-

The brokerage said the case rests on positioning in firm and dispatchable renewable energy, execution, return improvement, pipeline visibility and valuation. It expects EBITDA to grow at a 63% CAGR over FY25-28.

-

Incred said ACME has about 5 GW under construction or development, with about 80% of that mix in firm and dispatchable renewable energy. It expects capacity addition of 450 MW in FY26, 1.5 GW in FY27 and 1.5 GW in FY28.

Stock Market Live: Goldman Sachs Cuts Nifty Target, Turns Cautious On Indian Equities

- Goldman Sachs has cut its 12-month Nifty target to 25,900 from 29,300 and downgraded Indian equities to market-weight from overweight.

-

The brokerage said higher energy prices could weaken India’s macro position and has lowered earnings growth forecasts by a cumulative 9 percentage points over the next two years. It also expects consensus earnings estimates to be cut over the next two to three quarters.

-

Goldman Sachs said it prefers banks, staples, telecom, defence and energy. It has turned cautious on autos, consumer durables, NBFCs and oil marketing companies.

Read the full report here.

Stock Market Live: Brigade, HEG, ONGC, Reliance Power, HDFC Bank See Heavy Volumes

- Brigade Enterprises rose as much as 13% to Rs 760, with trading volume at nearly 140 times its 20-day moving average.

-

HEG gained as much as 14.2% to Rs 574.70, while ONGC rose up to 4% to Rs 281. HEG’s volume was 40 times its 20-day average and ONGC’s was 67% above its 20-day average.

-

On the downside, Reliance Power fell as much as 6.5% to Rs 21.20 and HDFC Bank declined up to 3.1% to Rs 758.10. Reliance Power’s volume was 54% above its 20-day moving average, while HDFC Bank’s was 16% above its 20-day moving average.

Source: Bloomberg

Stock Market Live: Centre Raises Commercial LPG Allocation To States To 70% Of Pre-Crisis Level

- The Union Ministry of Petroleum and Natural Gas has raised non-domestic LPG allocation to states to 70% of the pre-crisis level.

-

The revised allocation includes the existing 50% supply and an additional 20% now being provided. The government said the 70% level also includes the extra 10% linked to steps taken by states to promote piped natural gas.

-

The additional allocation will prioritise labour-intensive sectors such as steel, automobiles, textiles, dyes, chemicals and plastics, especially industries that use LPG for specialised heating and cannot shift to natural gas.

-

The ministry has also asked states to push registration compliance, encourage PNG connections where applicable, and circulate the Natural Gas and Petroleum Products Distribution Order, 2026.

Stock Market Live: PCBL Chemical Arm Commissions 30,000 MT Brownfield Carbon Black Capacity In TN

- PCBL Chemical said its arm has commissioned additional brownfield capacity of 30,000 MT of carbon black, according to an exchange filing.

-

The added capacity has been commissioned at the arm’s unit in Tamil Nadu.

Stock Market Live: Market Expert Nischal Maheshwari Sees 5-7% More Downside, Advises Buying On Dips

- Market expert Nischal Maheshwari said investors can keep accumulating on every 200-300 point fall and added that the Nifty is unlikely to break 20,000.

-

He said the market could see another 5-7% downside from current levels and added that the Street has already priced in a cut in GDP growth.

-

Maheshwari said it is a good time to start accumulating from the market, but added that many traders may look to short at current levels. He also said he does not expect the RBI to raise rates in the near term and suggested avoiding the market for now.

Stock Market Live: Hang Seng, Shanghai Rise; Nikkei, Kospi And ASX 200 Slip In Asia

- Hong Kong’s Hang Seng rose 0.67% to 25,022.01, while Shanghai gained 0.63% to 3,913.754.

-

Japan’s Nikkei 225 fell 0.43% to 53,373.07 and South Korea’s Kospi slipped 0.40% to 5,438.87.

-

Australia’s ASX 200 was also lower, down 0.11% at 8,516.30.

Stock Market Live: Biocon Names Shreehas Tambe CEO As Siddharth Mittal Steps Down

- Biocon said Siddharth Mittal will step down as chief executive officer and managing director at the close of business on March 31, 2026, to move into another leadership role within the Biocon Group. He will also cease to be a key managerial personnel.

-

The board has approved the appointment of Shreehas Pradeep Tambe, currently chief executive officer and managing director of Biocon Biologics, as an additional director from April 1, 2026 and as chief executive officer and managing director for five years from that date, subject to shareholder approval.

-

Biocon also said interim chief financial officer Mukesh Kamath will step down from the role at the close of business on March 31, 2026 to take up another role within the Biocon Group. He will also cease to be a key managerial personnel and senior management personnel.

Stock Market Live: Nifty MidCap 100, Nifty SmallCap 100 Underperform Nifty 50

- Nifty MidCap 100 fell 1.91% to 54,276.20 in trade.

-

Nifty SmallCap 100 declined 1.90% to 15,594.85.

-

Both indices underperformed the Nifty 50, which was down 1.54%.

Stock Market Crash Live: Three Reasons Why Nifty, Sensex Are Down

India's stock market resumed its decline on Friday, snapping a two-day positive run, tracking global cues as the Iran war and higher oil prices weighed on sentiment. The Nifty 50 and BSE Sensex both fell 1.5% during the session.

The blue-chip indices are set to log their fifth consecutive weekly loss, the longest stretch since August. The conflict in the Gulf, high energy prices and a weaker rupee have taken a toll on Dalal Street.

Share Market Live: Morgan Stanley On Pharma Stocks

- Mankind Pharma – Initiate Overweight with TP of Rs 2500

- Torrent Pharma – Initiate Equal-weight with TP of Rs 4580

- Mankind and Torrent are long-term compounding franchises within India’s pharmaceutical market

- Structural growth remains supported by chronic therapies, pricing, and new launches

- Earnings recovery and BSV-led optionality, along with supportive valuations, lead us to prefer Mankind

Stock Market Live: Rupee Falls To 94.53 Against US Dollar

- The Indian rupee weakened further in trade.

- The currency depreciated as much as 56 paise to 94.53 against the US dollar.

Stock Market Live: TCS, Sammaan Capital See Long Build-Up; Tata Motors PV, Shriram Finance In Short Build-Up

- Tata Consultancy Services and Sammaan Capital saw long build-up in trade.

-

Oracle Financial Services Software and Oil & Natural Gas Corporation saw short covering.

-

Housing & Urban Development Corporation and Godrej Properties saw long unwinding.

-

Tata Motors Passenger Vehicles and Shriram Finance saw short build-up.

Stock Market Live: Royal Orchid Hotels Signs Regenta Hotel In Mundra, Gujarat

- Royal Orchid Hotels has signed a Regenta Hotel in Mundra, Gujarat, according to an exchange filing.

-

The hotel will have 103 keys.

-

The property is scheduled to open by the fourth quarter of 2027.

Stock Market Live: Dr Reddy’s Tells Court It Will Propose New Name For Generic Semaglutide Drug

- Dr Reddy’s has told the court that it will propose a new name for its generic semaglutide drug.

-

The update comes after the Delhi High Court on Wednesday directed the company to pause the launch and sale of Olymviq over similarity with Novo Nordisk’s Ozempic.

-

The court had said the name could lead to confusion and asked the company to clarify whether it would drop the brand name.

Stock Market Live: L&T Wins Significant Buildings Orders Across Gujarat And Andhra Pradesh

- L&T said its Buildings & Factories business has secured multiple orders across states in India.

-

The orders include a float glass plant in Gujarat and a manufacturing facility for a two-wheeler company in Andhra Pradesh. The company will execute civil, steel, mechanical, electrical, plumbing and related works under the projects.

-

L&T also said it has received add-on orders in existing projects. The company classifies a significant order as one valued between Rs 1,000 crore and Rs 2,500 crore.

Stock Market Live: Tata Motors PV Falls 5% As JLR Pauses Some UK Production Lines

- Tata Motors Passenger Vehicles fell as much as 5.3% to Rs 301.05, its lowest level since May 2023.

-

Jaguar Land Rover has temporarily suspended production on some vehicle lines at its Solihull plant in the UK due to a parts supply issue.

-

JLR said the disruption is linked to a supplier problem and is expected to be resolved in less than two weeks. The affected period also includes a pre-planned shutdown for the Easter holidays.

Stock Market Live: Zaki Zaidi Says India Unlikely To Join Middle East Negotiations

- Zaki Zaidi, foreign affairs expert and former researcher at IDSA, said India is unlikely to be involved in negotiations on the war in the Middle East.

-

Zaidi said Gulf Cooperation Council countries do not have a united position on the conflict and added that Iran is not under pressure to agree to the US position at this stage.

-

He said Iran will not give up its uranium stock and added that Donald Trump is now trying to end the war. Zaidi also said Iran’s warnings on infrastructure attacks are being taken seriously.

Stock Market Live: PB Fintech Arm Faces Order In Vendor Transactions Case

- PB Fintech said the Delhi Adjudicating Authority has confirmed the order of the Initiating Officer on its arm, according to an exchange filing.

-

The company said Paisabazaar was alleged to be the beneficial owner in transactions with certain vendors.

Stock Market Live: Nifty Drops Below 23,000; Sensex Falls Over 1,000 Points

- Nifty fell as much as 1.43% to 22,973 in trade.

-

Sensex declined as much as 1.4%, or 1,084 points, to 74,189.

Stock Market Live: HEG, Graphite India Jump On Heavy Trading Volumes

- HEG rose as much as 13.65% to Rs 571, while Graphite India gained as much as 9.8% to Rs 654.25.

-

Trading activity was strong in both stocks. Graphite India’s volume was nearly 12 times its 20-day average, while HEG’s volume was more than 20 times its 20-day average, according to Bloomberg data.

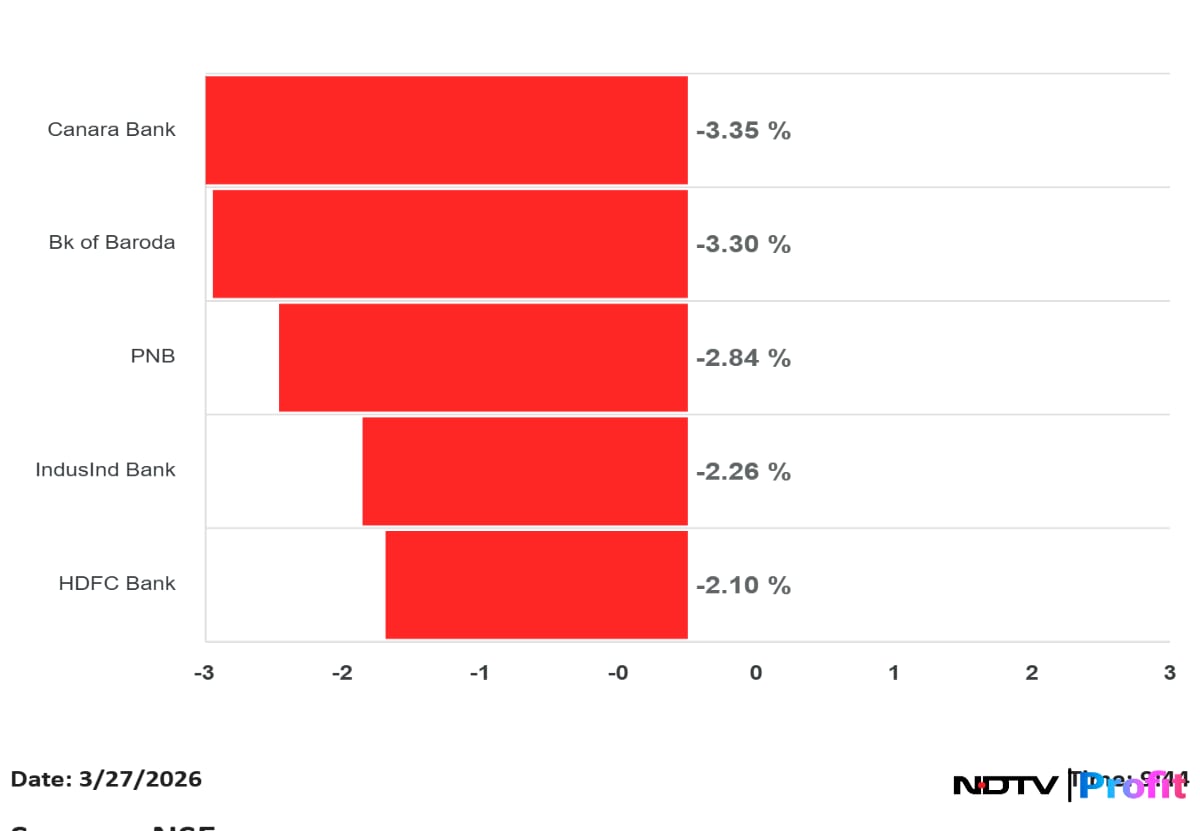

Stock Market Live: Canara Bank, Bank Of Baroda, PNB Drag Nifty Bank Lower

- Nifty Bank declined in trade, with Canara Bank, Bank of Baroda and PNB among the main losers.

-

Canara Bank fell 3.35%, Bank of Baroda dropped 3.30% and PNB declined 2.84%.

-

IndusInd Bank and HDFC Bank also weighed on the index, falling 2.26% and 2.10% respectively.

Stock Market Live: Brigade Enterprises Jumps 12.3% On Bengaluru Project Launch

- Brigade Enterprises rose as much as 12.3% to Rs 760 after launching a project in Bengaluru.

-

The company said the project has a revenue potential of Rs 700 crore.

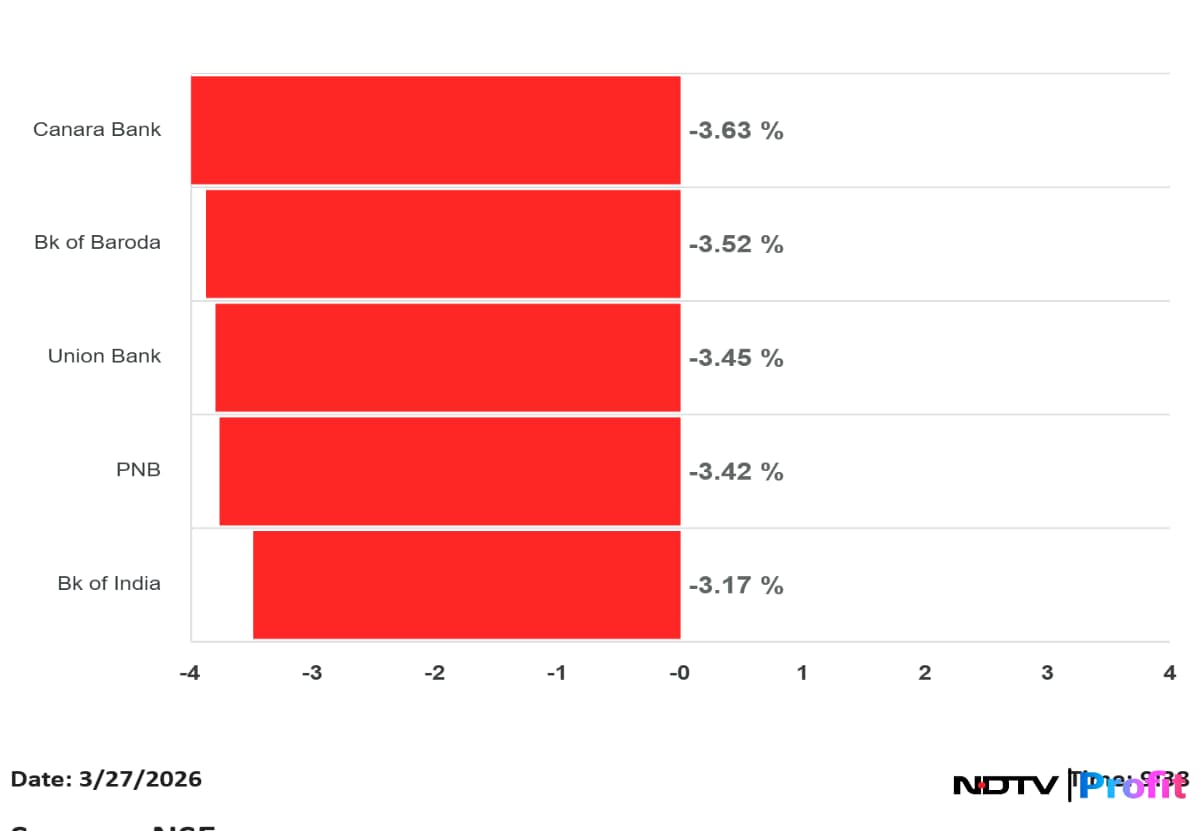

Stock Market Live: Nifty PSU Bank Turns Worst NSE Sectoral Performer; Canara Bank Leads Fall

- Nifty PSU Bank was the worst-performing sectoral index among the NSE gauges in trade.

-

Canara Bank led the decline, falling 3.63%. Bank of Baroda dropped 3.52%, Union Bank fell 3.45%, and PNB declined 3.42%.

-

Bank of India was also among the main losers, down 3.17%.

Stock Market Live: Infosys Gains On $560 Million US Acquisitions, Weak Rupee Support

-

Infosys rose as much as 1.2% to Rs 1,295 after announcing two acquisitions worth $560 million, or Rs 5,247 crore.

-

The company will acquire Optimum Healthcare IT for $465 million and Stratus Global for up to $95 million. The deals deepen Infosys’ presence in the US healthcare and insurance segments and are expected to close by Q1FY27. With these transactions, Infosys now has three acquisitions pending closure, including the earlier Versent deal.

-

The stock also found support from the rupee hitting a record low. A weaker rupee typically helps IT companies because they earn a large share of revenue in US dollars, while a significant part of their costs is in rupees.

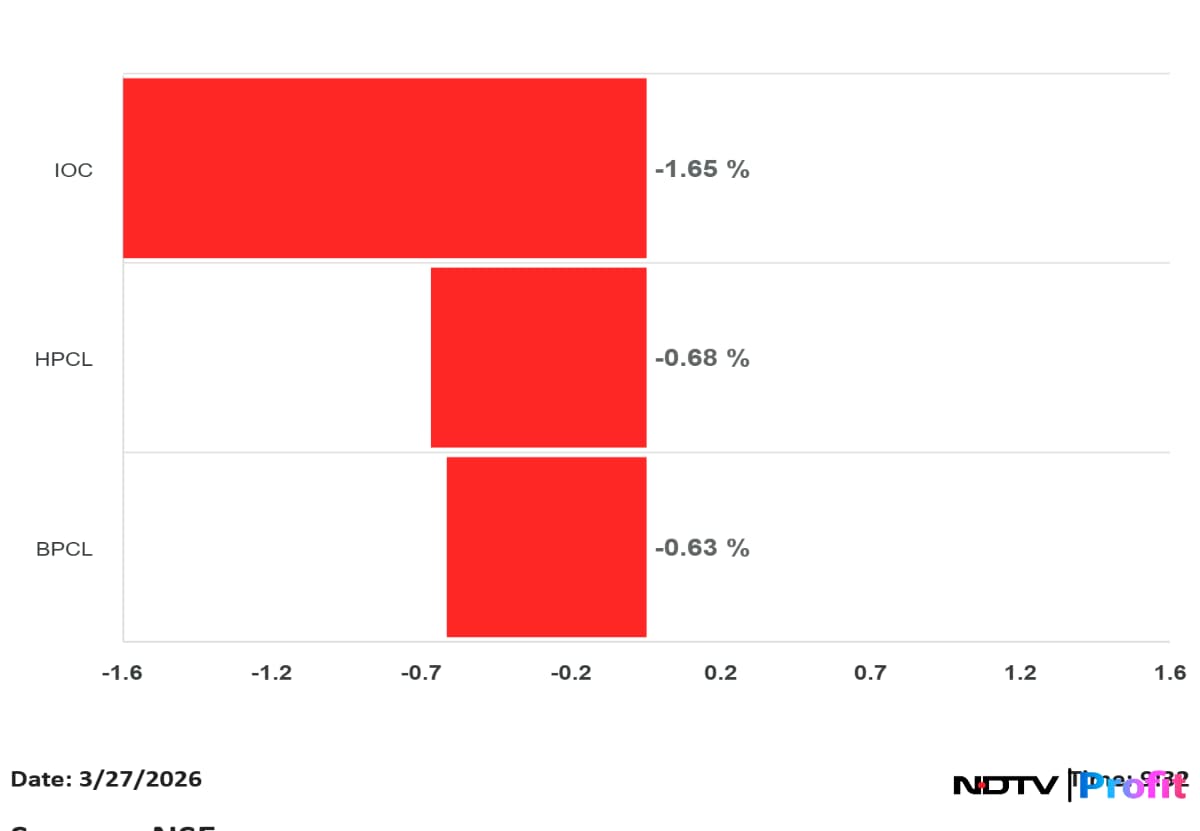

Stock Market Live: IOC, HPCL, BPCL Fall Over Excise Duty Cut, Brent Holds Near $100

- Oil marketing company stocks declined after the excise duty cut on fuel and as Brent crude hovered around $100 a barrel.

-

IOC fell 1.65%, HPCL was down 0.68%, and BPCL declined 0.63% in trade.

Stock Market Live: Hindalco Sees 58.1 Lakh Shares Trade In Block Deal

- Hindalco saw 58.1 lakh shares change hands in a block deal.

-

The buyers and sellers were not known immediately.

Stock Market Live: Bharti Airtel Sees 33.4 Lakh Shares Trade In Block Deal

- Bharti Airtel saw 33.4 lakh shares change hands in a block deal.

-

The buyers and sellers were not known immediately.

Stock Market Live: Nifty PSU Bank Leads Sectoral Fall; Nifty IT Only Gainer

- Fourteen of the 15 sectoral gauges compiled by the NSE traded lower in the session.

-

Nifty PSU Bank was the worst-performing sectoral index, falling 2.3%.

-

Nifty IT was the only sectoral gainer, rising 0.9%.

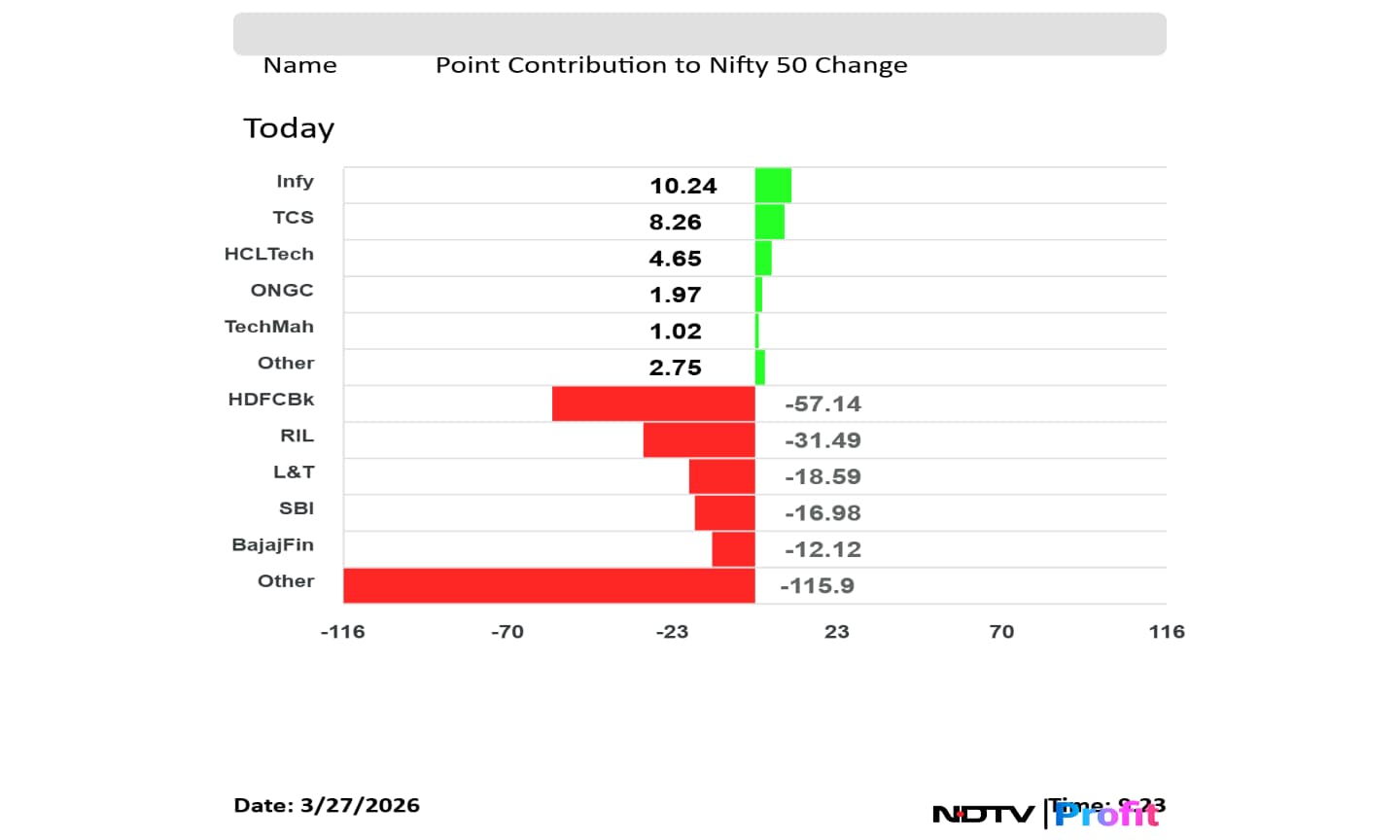

Stock Market Live: HDFC Bank, Reliance And L&T Drag Nifty

- HDFC Bank was the biggest drag on the Nifty, pulling the index down by 57.14 points. Reliance Industries, L&T, SBI and Bajaj Finserv also weighed on the index, with contributions of 31.49, 18.59, 16.98 and 12.12 points respectively.

-

Infosys was the top positive contributor, adding 10.24 points to the Nifty. TCS, HCL Tech, ONGC and Tech Mahindra also supported the index, contributing 8.26, 4.65, 1.97 and 1.02 points respectively.

Stock Market Live: Nifty Falls 1.1%, Sensex Drops 835 Points In Trade

- Nifty fell as much as 1.1% to 23,044 in trade.

-

Sensex declined as much as 1.1%, or 835 points, to 74,437.

Stock Market Live: Nifty Falls 0.7% In Pre-Market, Sensex Down 500 Points

- In pre-market trade, Nifty fell 0.7% to 23,149.

-

Sensex declined 0.6%, or 500 points, to 74,765.

Stock Market Live: Rupee Falls Below 94 Against US Dollar At Open

- The rupee weakened past the 94 mark against the US dollar in opening trade.

-

The local currency fell as much as 94.17 at the open.

Stock Market Live: Buyback Taxation Changes: Wipro Seen To Move First Among IT Majors After April 1

Stock Market Live: Delhi High Court Halts Dr Reddy’s Olymviq Launch Over Name Similarity

- The Delhi High Court said on Wednesday that Dr Reddy’s generic weight-loss product name, Olymviq, is similar to Novo Nordisk’s Ozempic.

-

The court directed Dr Reddy’s to pause the launch and sale of Olymviq till Friday.

-

The company has been asked to inform the court whether it will drop the name. The court said similar brand names could lead to confusion.

Stock Market Live: Former HPCL Chief Says Excise Move Aims To Support OMCs

- Former HPCL Chairman and Managing Director M K Surana said public sector oil companies cannot shut fuel stations even if crude supply is unavailable.

-

He said petrol prices for customers may remain unchanged despite the duty move.

-

Surana said the government’s step is aimed at supporting the sustainability of oil marketing companies, with the government and OMCs sharing the impact of the situation.

Stock Market Live: Aequs Signs Karnataka MoU For Rs 2,856 Crore Expansion

- Aequs has entered into a memorandum of understanding with the Karnataka government for expansion.

-

The MoU covers the expansion of manufacturing units in Karnataka.

-

The estimated investment for the project is Rs 2,856 crore, according to an exchange filing.

Stock Market Live: JSW Energy Implements Raigarh Champa Rail Infrastructure Acquisition Plan

- JSW Energy said the resolution plan for the acquisition of Raigarh Champa Rail Infrastructure Private has been implemented.

-

The resolution amount for the acquisition is Rs 700 crore, according to an exchange filing.

Stock Market Live: Zee Board Approves $23.90 Million FCCB Redemption, Clears Content Unit Transfer

- Zee Entertainment said its board has approved the redemption of foreign currency convertible bonds worth $23.90 million, according to an exchange filing.

-

The board has also approved the transfer of the licensing content business to its arm ZI-IPR.

-

Zee will invest Rs 500 crore in ZI-IPR through optionally convertible debentures and Rs 20 crore to acquire a 51% stake in CORE Pvt.

Stock Market Live: SEAMEC Gets Rs 330 Crore ONGC Award For Vessel Services

- SEAMEC said it has received a notification of award worth Rs 330 crore from ONGC for operations and maintenance services for a vessel.

-

The company said the award has been issued to a consortium of SEAMEC and Supreme Hydro, according to an exchange filing.

Stock Market Live: Infosys In Focus After Brokerages Assess Two US Acquisitions

- Nomura maintained its Buy rating on Infosys with a target price of Rs 1810. It said the two acquisitions worth $560 million could add 225 basis points to FY27 revenue growth and help Infosys add clients and strengthen capabilities in life sciences and healthcare. Nomura retained Infosys as its top large-cap Indian IT pick.

-

Morgan Stanley maintained its Equal-weight rating with a target price of Rs 1760. It said the Optimum Healthcare IT and Stratus deals could account for 1.2% of FY27 revenue and may be neutral to slightly dilutive to earnings due to lower EBIT margins and amortisation costs. It added that Optimum Healthcare IT is still awaiting regulatory approval.

-

Citi maintained its Neutral rating with a target price of Rs 1395. It said the two acquisitions could add 1.6% to annualised revenue, but flagged the need to assess profitability, the sharp jump in Optimum’s CY25 revenue after a decline in CY24, and integration risks.

Stock Market Live: Anand Rathi Initiates Vishal Mega Mart With 'Buy' Rating, Sets Rs 134 Target Price

- Anand Rathi has initiated coverage on Vishal Mega Mart with a Buy rating and a target price of Rs 134.

-

The brokerage expects revenue, EBITDA and profit after tax to grow at a CAGR of 19%, 21% and 25% over FY25-28.

-

Anand Rathi said the company’s valuation is supported by focused expansion, an asset-light model and cash flow. It added that a technology-led supply chain and hub-and-spoke distribution support execution.

-

The brokerage said Vishal Mega Mart plans to add 80-100 stores every year, with South and West India still underpenetrated. It also said private labels remain central to growth, while the company’s focus on lower- and middle-income consumers and its presence in tier-2 and tier-3 markets support growth.

Stock Market Live: Motilal Oswal Initiates Coverage On ICICI Prudential AMC With 'Buy' Rating, Sets Rs 3,500 Target Price

- Motilal Oswal has initiated coverage on ICICI Prudential AMC with a Buy rating and a one-year target price of Rs 3,500.

-

The brokerage expects revenue to grow at a CAGR of 15% over FY26-28, while profit after tax is seen rising at a 16% CAGR over the same period. It expects EBITDA margins to remain above 70%.

-

Motilal Oswal said the company is placed to benefit from growth in India’s mutual fund industry and expects mutual fund quarterly average assets under management to grow at a 17% CAGR over FY26-28.

-

It added that yields remain stable despite the telescopic TER structure and a larger asset base, supported by a steady equity mix, performance and distribution discipline.

Stock Market Live: India Cuts Special Additional Excise Duty On Petrol, Diesel

-

The government has reduced the special additional excise duty on petrol to Rs 3 per litre from Rs 13 per litre.

-

The special additional excise duty on diesel has been cut to nil from Rs 10 per litre.

Stock Market Live: Ola Electric Launches Campaign, Offers EVs At Rs 49,999

Ola Electric has launched a campaign and is offering electric vehicles at Rs 49,999.

Brigade Enterprises Launches Bengaluru Project With Rs 700 Crore Revenue Potential

- Brigade Enterprises has launched a project in Bengaluru.

- The project has a revenue potential of Rs 700 crore.

Stock Market Live: Power Mech Projects In Focus After Order Book Cut By Rs 1,563 Crore

Power Mech Projects is on the watchlist after its order book was reduced by Rs 1,563 crore.

Stock Market Live: Tolins Tyres, Shree Tirupati Balajee, Saatvik Green Energy, Gujarat Kidney And Gaudium IVF In Focus On Lock-In End

Tolins Tyres, Shree Tirupati Balajee, Saatvik Green Energy, Gujarat Kidney & Super Speciality and Gaudium IVF are on the watchlist as their lock-in period ends.

Stock Market Live: Infosys In Focus After $560 Million Acquisitions In US Healthcare And Insurance

- Infosys has announced two acquisitions worth $560 million, or Rs 5,247 crore. It will acquire Optimum Healthcare IT for $465 million and Stratus Global for up to $95 million.

-

The deals deepen Infosys’ presence in the US healthcare and insurance segments and are expected to close by Q1FY27. With these transactions, Infosys now has three acquisitions pending closure, including the earlier Versent deal.

-

Optimum Healthcare IT is a healthcare IT digital transformation company serving US hospitals and payers. Infosys said the deal will expand its healthcare presence, add new clients and bring more than 1,600 experts. Optimum reported CY25 revenue of $275.9 million.

-

Stratus Global serves property and casualty insurers and focuses on insurance technology. Infosys said the deal will strengthen its insurance business and support AI-led digital transformation. Stratus reported CY25 revenue of $42.8 million.

-

The two deals are expected to add to revenue growth, though both may be marginally dilutive to earnings per share in the initial years. Infosys’ three pending acquisitions are estimated to contribute 2.0% to 2.5% inorganic growth in FY27.

Stock Market Live: Reliance Industries Rejects Report On Iranian Crude Purchase

- Reliance Industries said reports about the purchase of Iranian crude oil are baseless, according to an exchange filing.

-

The company said the reports of buying Iranian oil are entirely baseless.

Stock Market Live: Morgan Stanley Says L&T Tech SWC Exit Supports Value

- Morgan Stanley maintained its Equal-weight rating on L&T Technology Services with a target price of Rs 4420 after the company divested its SWC business.

-

The brokerage said the business did not scale as management had expected at the time of the 2023 acquisition and had weighed on margins and cash flow.

-

Morgan Stanley said the exit fits management’s framework for non-strategic businesses and sees the transaction as slightly positive, adding 1.5-2% to market value.

Stock Market Live: Jefferies Flags Crowded Semaglutide Launches, Sees Edge For Sun, Lupin And Torrent

- Jefferies said more than 10 semaglutide brands have launched online in India after Novo’s patent expiry last weekend, with over 40 brands expected across injectable and oral forms.

-

The brokerage said injectable prices are in the Rs 1,290-4,500 a month range. Natco and Glenmark are at the lower end, while Dr Reddy’s and Torrent are priced higher. It added that Torrent alone is selling the oral form at smaller discounts.

-

Jefferies said most brands are sold out online due to supply mismatch and tighter regulation. It added that strict prescribing norms favour companies such as Sun Pharma, Lupin and Torrent.

Stock Market Live: Jefferies Says Bank Meetings Point To Stable Q4, Flags Risk If Conflict Lasts

- Jefferies said banks indicated business trends improved in Q4, suggesting stable results for the quarter.

-

The brokerage said if the conflict continues for longer, it could affect net interest margins, growth and asset quality, in that order.

-

It said working capital demand has risen, while some capex is slowing. Jefferies added there has been no move on moratoriums with the RBI so far, as the impact is not yet broad. It said collections in April will be important to watch and reiterated that Nifty Bank price-to-book is near lows, offering attractive risk-reward.

Stock Market Live: Jefferies Says AI, Currency Concerns Weigh On Capital Goods Sentiment

- Jefferies said market sentiment in capital goods is under pressure from AI-related concerns and currency moves.

-

The brokerage said one month of no work for L&T in the Middle East could mean a 6-8% hit to annual earnings per share.

-

Jefferies said NTPC and JSW Energy could see upside from a recovery in power demand and execution. It added that margin expansion could support Siemens Energy and Hitachi Energy, while Cummins offers visible FY25-28 earnings growth and return ratios.

-

In defence, Jefferies said Bharat Electronics remains a core holding, while some contra investing has started in Hindustan Aeronautics. It added that KEI stands out for its exposure to multiple end markets.

Stock Market Live: Goldman Sachs Cuts India To Market-Weight, Lowers Nifty Target

- Goldman Sachs has downgraded Indian equities to market-weight, citing higher-for-longer energy prices and a weaker macro setup for India.

-

The brokerage has cut its earnings growth forecast for India by a cumulative 9 percentage points over the next two years and said consensus estimates could see meaningful cuts over the next two to three quarters. It also lowered its 12-month Nifty target to 25,900 from 29,300.

-

Goldman Sachs said near-term investor sentiment could stay soft and prefers defensive sectors over cyclical ones. It is overweight on banks, staples, telecom, defence and energy, while downgrading cyclicals and downstream sectors such as durables, autos, NBFCs and OMCs.

Stock Market Live: Citi Stays Cautious On IT, Prefers Infosys And HCL Tech

- Citi said Indian IT is heading for a fourth straight year of subdued growth and expects Q4FY26 constant-currency organic services revenue growth of -1% to 1% quarter-on-quarter for the top five companies.

-

The brokerage said macro risks may rise in early FY27 and expects the recovery to remain slow and uneven. It said management commentary on Middle East impact, total contract value trends and AI will be in focus.

-

Citi said margin trends need monitoring, though a weaker rupee could help in the near term. It remains cautious on the sector and prefers Infosys and HCL Tech among large-cap names.

Stock Market Live: Shanghai, Hang Seng Trade Lower In Asia

- Shanghai fell 0.95% to 3,852.094 in trade.

- Hang Seng declined 0.35% to 24,768.66.

Stock Market Live: Chris Wood Adds HSBC, Drops HDFC Bank In Greed & Fear Portfolio

- Chris Wood has introduced HSBC with a 4% weighting in the Asia ex-Japan long-only portfolio, Global and International long-only equity portfolio. The move replaces HDFC Bank.

-

In the Asia Pacific ex-Japan relative-return portfolio, the weighting in Australia and India has been cut by two percentage points each.

-

The weighting in Taiwan has been increased by four percentage points.

Stock Market Live: Kotak Says Medium-Term Risk-Reward Has Improved Despite Recent Fall

- Kotak India Strategy said the sharp fall in stock prices points to a bleak scenario, but a short and sharp conflict would be manageable and may have a limited impact on earnings.

-

It said the reward-risk balance looks better for the medium term.

-

Kotak added Coforge, Embassy REIT, Eureka Forbes, Federal Bank, Home First, Jubilant Food and Vishal Mega Mart to its mid-cap portfolio. It added DLF, Godrej Consumer and Info Edge to its large-cap portfolio.

-

The brokerage reduced weight on Reliance Industries and increased weight on M&M.

Stock Market Live: Nomura Sees Further White Goods Price Hikes From April

- Nomura said white goods companies are preparing for a second round of price increases of 7-12% from April.

-

The brokerage said companies are passing on cost increases in phases, which should help ease near-term cost pressure.

-

Nomura said strong summer demand remains the key factor to track, as the outlook for demand and margins will depend on the season.

Stock Market Live: Brent Falls To $100.57, WTI Drops 1.5% As Tensions Ease

- Oil prices fell as tensions eased in the conflict that has lasted nearly a month.

-

West Texas Intermediate for May delivery dropped 1.5% to $93.07 a barrel.

-

Brent crude futures fell 0.7% to $100.57 a barrel.

Stock Market Live: Kospi, Nikkei, ASX 200 Fall In Asia; Hang Seng Futures Lower

- South Korea’s Kospi fell 4.16% to 5,233.06, while Japan’s Nikkei 225 declined 1.90% to 52,584.22.

-

Australia’s ASX 200 was down 0.79% at 8,458.10.

-

Hang Seng index futures were at 24,782, below the last close of 24,856.43.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.