(Bloomberg Businessweek) -- SPACs were one of Wall Street's hottest trades during the pandemic bull market that finally came to a crashing close in June. Special purpose acquisition companies, also known as blank-check firms, go public without having a business yet. Instead, they're formed to raise money so that they can buy another, still-private company to be chosen later. SPACs captured the imagination of a lot of ordinary investors who saw them as a way to get in early on promising startups before they went public.

The fad also attracted a range of Wall Street titans, athletes, and celebrities looking to get a piece of the pie by starting their own SPACs. But tumbling stock prices—especially those of more speculative, early-stage companies—have wiped out billions of dollars in value for shareholders who held SPACs after their acquisition deals. Some companies that went public via a merger with a SPAC have fallen so far that they've been bought by private companies or competitors at far lower prices. At the same time, a lot of blank-check companies that have yet to do a deal are coming up on big deadlines. If they don't find a deal soon, they'll have to return the money they raised to their shareholders.

This isn't the first time blank checks have flopped. An iteration in the 1980s rode the boom in penny stocks, but the business became notorious for fraud and was all but wiped out when Congress passed tougher rules. The latest SPAC era is coming to a close less dramatically, in a long, painful wind-down.

● The Boomerang KidsWhen a SPAC finds a private business to buy and then merges with it, what it's really doing is helping that company go public without some of the oversight and cost of a conventional initial public offering. The merged entity takes on the target company's name and business operations while inheriting the blank-check firm's stock listing. For example, the SPAC Healthcare Merger Corp. combined with the telemedicine provider SOC Telemed Inc. to bring that company onto the Nasdaq in November 2020. On its first day of trading under that name, it closed at $9 a share.

SOC was a public company for less than a year and a half. In April, it boomeranged back into private hands when it was bought out for just $3 a share by Patient Square Capital, a private equity firm. SOC's cameo appearance on the stock market wiped out more than $300 million in value for the shareholders who held on all the way through.

Auto insurer MetroMile Inc. has also taken a buyout offer, from publicly traded insurance company Lemonade Inc. MetroMile is currently trading for less than a dollar a share, far below the $17 it traded at after the INSU Acquisition Corp. II blank-check company finished merging with it early last year.

And then there's the very odd case of Redbox Inc., the company famous for renting DVDs from vending machines. It's accepted an offer to be purchased by Chicken Soup for the Soul Entertainment Inc. in a deal that assessed its total equity at $31 million, less than 5% of its value when Seaport Global Acquisition Corp. helped Redbox go public. But in a flashback from 2021, Redbox shares have since been embraced by social media-driven “meme” traders, sending the stock soaring far above the price shareholders will get if the deal goes through.

These deals could be just the beginning. The De-SPAC Index, which measures the performance of companies that went public via a blank-check company, is down 62% this year, about three times the loss of the S&P 500. That's likely to attract some bargain hunters while inspiring activist hedge fund investors to push for buyouts. “There's going to be restructuring, takeouts by private equity,” says Victoria Grace, a venture capital investor who founded Queen's Gambit Growth Capital, a SPAC that merged with Dubai-based ride-hailing company Swvl Holdings Corp. “But that makes sense for a lot of those that are not performing the way they need to, to be a proper public company.” Swvl recently traded at $6.40 a share, down about a third from its value after the deal that brought it to the Nasdaq in April. “We are in a challenging macro environment, and our focus is on running a sustainable business that will be profitable,” Grace says.

● A Wall of RedemptionsIn a raucous stretch in 2020 and 2021, more than 850 blank-check companies raised about $250 billion, creating a glut of management teams on the hunt to find something to buy. Generally, SPACs need to locate and complete an acquisition within 24 months, and there are now about 410 companies with $116 billion looking for deals by the end of March 2023, according to SPAC Research data analyzed by Bloomberg.

That could be tough. SPACs can't do a deal without their investors' approval, and with markets in a spin, shareholders are likely to be extra skeptical. When SPACS run into their deadline, they have to give investors their money back—typically $10 per share, the initial price of most blank checks—plus interest. Management teams can get short extensions, but they usually have to pay shareholders for this as well as getting their approval.

Part of the idea of a SPAC is that talented managers can use their industry insights and connections to locate especially good companies and then help them grow. But with so many SPACs under pressure to find deals, those managers may stretch further from their areas of expertise. Tuscan Holdings Corp. II bailed on its initial plans to merge with a cannabis firm, and instead is striking a pact with Surf Air Mobility Corp., a membership-based operator of private planes with plans to rely on electric engines. That came after almost three years of hunting for a deal and multiple extensions.

SPAC managers, also known as sponsors, have a strong incentive to make deals: In some cases, they can get 20% of the newly public company while risking a comparatively small amount of their own cash to pay for things like fees to underwriters and others. “One of the criticisms of SPACs is, between the underwriters and the sponsors, you have too many middlemen taking a piece of the pie,” says Jay Ritter, a University of Florida finance professor who studies SPACs and IPOs.

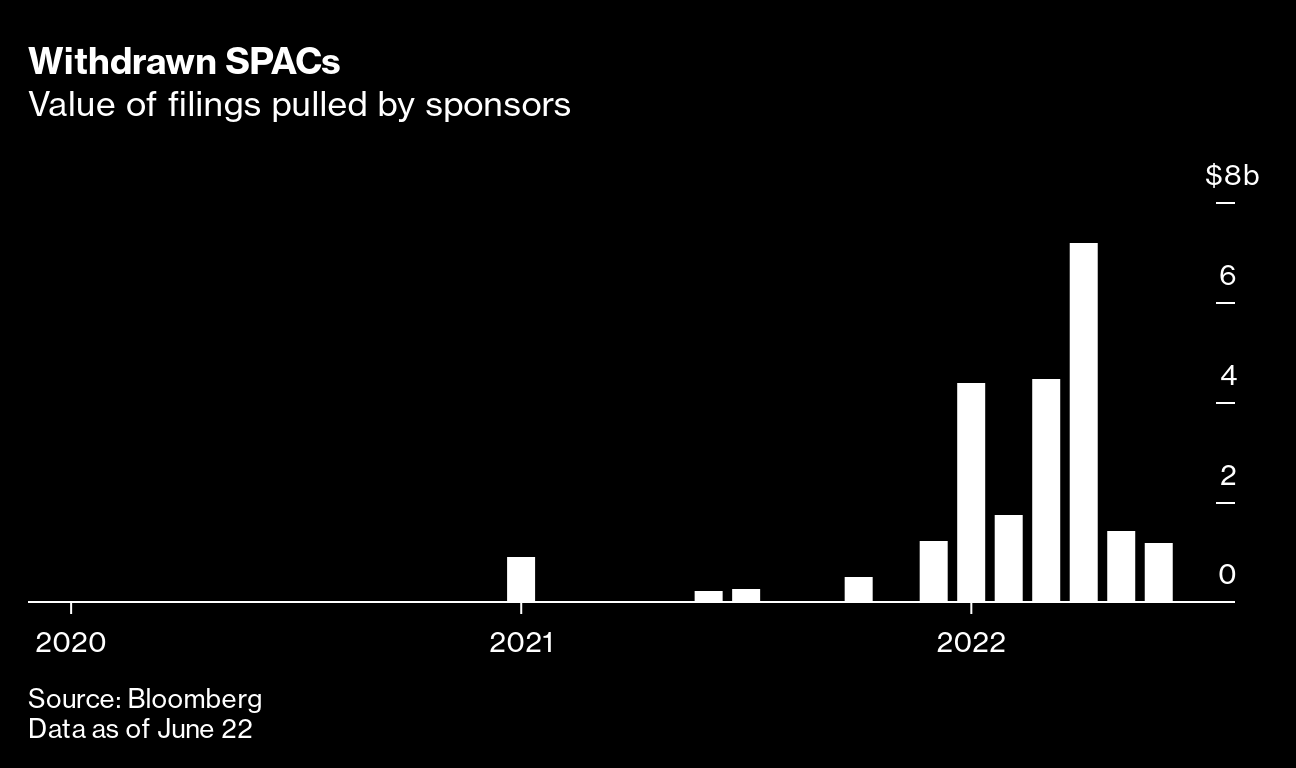

Even so, the industry's choppy performance has driven some seasoned sponsors to withdraw or abandon plans for SPACs that would've raised more than $29 billion this year alone. Teams led by well-known sponsors including Paul Singer's Elliott Management Corp. and James Murdoch, son of media mogul Rupert, have bowed out. Other SPACs that are trading have seen key backers hand over the reins to other managers. As the pace of deals slows to a crawl, Ritter estimates close to 80% of SPACs will call it quits and return their money to investors.

SPACs could enter a mature phase where only managers who are serious and committed to the vehicle will be successful, says Anderson Lafontant, senior adviser at Miracle Mile Advisors. “It will allow teams to slow down, conduct the proper due diligence, and not rush to get a deal done because they are afraid of losing it,” she says.

But SPACs have drawn criticism from the US Securities and Exchange Commission, which is talking about tighter regulations. “Even without the SEC's proposed rules, we were on track for a natural down cycle, with too many SPACs and not enough targets,” says Usha Rodrigues, a professor of law at the University of Georgia who has researched blank checks. “This might be the death of SPACs.”

● The Remaining WinnersFor all that, some savvy investors have managed to make money off SPACs. Hedge funds including Millennium Management, Citadel, and D.E. Shaw & Co. were among the biggest investors at the end of the first quarter, owning more than $4 billion each, according to SPAC Research. Hedge funds typically aren't long-term investors. When a merger is announced, the hope is the stock will spike, and they'll cash out before the deal closes.

Institutional investors who bought in early often had another edge. If they invested in a SPAC at its IPO—when it raised money for a future acquisition—they'd pay $10 a share for the stock but also get some warrants. These are options to buy shares of the merged company later at a set price. Selling the stock while hanging on to the warrants can snag a nice profit even if the acquisition is a dud in the long run. Elizabeth Warren and other Senate Democrats sent a letter to six prominent SPAC operators last September outlining a number of concerns about big institutions benefiting from SPAC deals at the expense of ordinary investors. They also called out hedge funds for cashing in on warrants, which they said were “effectively lottery tickets,” albeit ones with a far better chance of paying off.

One hedge fund manager, Boaz Weinstein, started loading up on SPACs in the second quarter of last year and purchased $5.5 billion of them over the next 12 months, according to an investor in his Saba Capital Management. Since the investment in a SPAC earns interest while the company looks for a deal, for Saba it's basically a safe place to park cash, with a potential kicker from warrants. The fund uses the money it makes on the SPACs to pay for its bearish bets on corporate bonds. It's a nice deal if you get it—but as blank checks dry up, it may disappear, too.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.