Reliance Industries Ltd.has reported its results for the fourth quarter of FY26.

Here is all you need to know about RIL's fineprint.

End of Coverage

The live blog has ended.

RIL Q4 Results Today Live Updates: Unchanged Fuel Prices Amid Iran War Led To Under Recovery

The company said that agile crude sourcing amid West Asia conflict to sustain throughput. It added that it kept retail fuel prices unchanged which led to under recoveries and that it faced headwinds due to higher crude, freight, insurance, fuel costs.

However, it pointed out that performance of telecom, retail operations somewhat offset energy weakness.

RIL Q4 Results Today Live Updates: OTC Segment

O2C revenue rose 14% to Rs 1,84,944 crore, but Ebitda fell 12% to Rs 14,520 crore. Margin contracted 7.85%, indicating pressure despite higher sales.

RIL Q4 Results Today Live Updates: Freight Charges And Oil Premiums Weight On Growth

Freight charges jumped 10-15x of normal and insurance cost increased from $25000-30000 to $1.5-2 million

Oil premium went as high as $20-30/bbl

For May 2026, premium has been kept at $20/bbl

Domestic LPG supply rose 4x from normal

(Source: RIL Con Call)

RIL Q4 Results Today Live Updates: Reliance Sees Traction In Telecom Bizz; Jio Platforms Listing Soon

RIL says that it sees traction building in telecom business going forward . RIL Chairman Mukesh Ambani said the company is advancing steadily towards listing of Jio Platforms.

RIL Q4 Results Today Live Updates: Segmental Overview

Segment Performance

- Digital revenue rose 3% quarter on quarter to Rs 45,945 crore, while Ebitda increased 4% to Rs 20,041 crore. Margin expanded to 43.62%, making it one of the stronger contributors in the quarter.

- Retail revenue increased 1% to Rs 98,457 crore. Ebitda was largely flat at Rs 6,921 crore, Margin contracted to 7.03%.

- O2C revenue rose 14% to Rs 1,84,944 crore, but Ebitda fell 12% to Rs 14,520 crore. Margin contracted 7.85%, indicating pressure despite higher sales.

- Oil and gas revenue increased 1% to Rs 5,867 crore, while Ebitda declined 14% to Rs 4,195 crore. Margin contracted to 71.50%.

- Other businesses posted revenue growth of 57% to Rs 27,976 crore, while Ebitda was flat at Rs 2,746 crore. Margin contracted to 9.82%.

RIL Q4 Results Today Live Updates: Retail Segment Performance

- Retail Rev up 1% at Rs 98,457 crore versus Rs 97,912 crore QoQ

- Retail EBITDA At Rs 6,921 versus Rs 6,915 crore QoQ

RIL Q4 Results Today Live Updates: Oil & Gas Performance

Oil & Gas Revenue up 1% At Rs 5,867 crore

Oil & Gas Revenue At Rs 5,867 crore Vs Rs 5,833 crore QoQ

Oil & Gas EBITDA down 14% At Rs 4,195 crore

Oil & Gas EBITDA At Rs 4,195 crore Vs Rs 4,857 crore QoQ

RIL Q4 Results Today Live Updates: Reliance Jio Sees Modest Uptick In Profit

Leading telecom giant Reliance Jio Infocomm Ltd. reported a 4% sequential increase in its consolidated net profit during the quarter ended March, according to the financial results announced by the oil-to-telecom conglomerate on Friday.

The telecom arm of billionaire industrialist Mukesh Ambani's conglomerate logged a bottom-line of Rs 7,935 crore, compared to Rs 7,629 crore in the March quarter of FY25. The average revenue per user (ARPU) increased by 0.1% to Rs 214, compared to Rs 213.7 in the previous quarter.

Read more

RIL Q4 Results Today Live Updates: Oil & Gas Margin Sees Sharp Contraction Amid Iran War Disruption

The EBITDA margin for the oil and gas segment saw a sharp decline of 1,177 basis points to 71.5% from 83.27%

RIL Q4 Results Today Live Updates: Oil Gas Revenue Sees Marginal Rise, Pressure On Operational Front Amid Iran War

The revenue for the oil and gas segment of RIL rose 1% sequentially to Rs 5,867 crore from Rs 5,833 crore. At the same time, EBITDA declined 14% to Rs 4,195 crore from Rs 4,857.

RIL Q4 Results Today Live Updates: Net Profit Slips, Revenue Rises And Margin Contracts

RIL Q4FY26 Highlights (QoQ)

- Revenue increased by 11% to Rs 2,94,059 crore from Rs 2,64,905 crore

- EBITDA decreased by 4% QoQ to Rs 44,141 Crore from Rs 46,018

- EBITDA Margin contracted to 15.0% from 17.4% in the previous quarter.

- Net Profit dropped 9% QoQ to Rs 16,971 Crore from Rs 18,645 Crore

RIL Q4 Results Today Live Updates: Should You Buy RIL's Stock?

Out of the 34 analysts tracking the company on Bloomberg, 33 have a buy call while only one recommends selling the stock.

RIL Q4 Results Today Live Updates: What To Expect From Jio?

Reliance Jio is expected to post steady performance, with Ebitda projected to rise 3% to Rs 18,269 crore. Average revenue per user or ARPU is estimated to edge up to Rs 216 from Rs 214, supported by customer upgrades, while subscriber additions are seen slowing to 52.2 crore, the weakest quarterly addition in fiscal 2026.

RIL Q4 Results Today Live Updates: Operation Strain Seen On Oil And Gas Exploration Segment

Oil and gas exploration Ebitda is projected to fall sharply by 12.5% to Rs 4,249 crore, the biggest drop in 16 quarters, due to lower volumes and higher costs.

RIL Q4 Results Today Live Updates: Oil To Chemicals Segment In Focus Amid Iran War Disruptions

The oil-to-chemicals segment's Ebitda is seen flat at around Rs 16,505 crore despite higher gross refining margins, weighed down by higher freight costs, insurance premiums, elevated gas costs, increased LPG output, and diversion of gas produced at the KG basin to priority sectors.

RIL Q4 Results Today Live Updates: Analysts Expect Revenue Decline For Revenue Business

Segment-wise, the retail business is expected to see a 10.6% drop in revenue to Rs 87,568 crore, though Ebitda may rise 2% to Rs 7,051 crore due to cost management, with growth constrained by a high base.

RIL Q4 Results Today Live Updates: How Reliance Did In Last Quarter

Reliance Industries Q3 Results (Consolidated, QoQ)

- Revenue up 4% at Rs 2.69 lakh crore versus Rs 2.59 lakh crore (Estimate: Rs 257038 crore)

- Ebitda up 0.3% at Rs 46,018 crore versus Rs 45,885 crore (Estimate: Rs 47,997 crore)

- Margin at 17.4% versus 18% (Estimate: 18.7%)

- Net profit up 2.6% at Rs 18,645 crore versus Rs 18,165 crore (Estimate: Rs 19,271 crore)

RIL Q4 Results Today Live Updates: Brokerage Target On Reliance Stock

All but one out of 34 analysts tracking Reliance Industries have a 'Buy' rating on the stock, and one suggests a 'sell', according to Bloomberg data. The average of 12-month price targets is Rs 1,736 and indicates a potential upside of 29%.

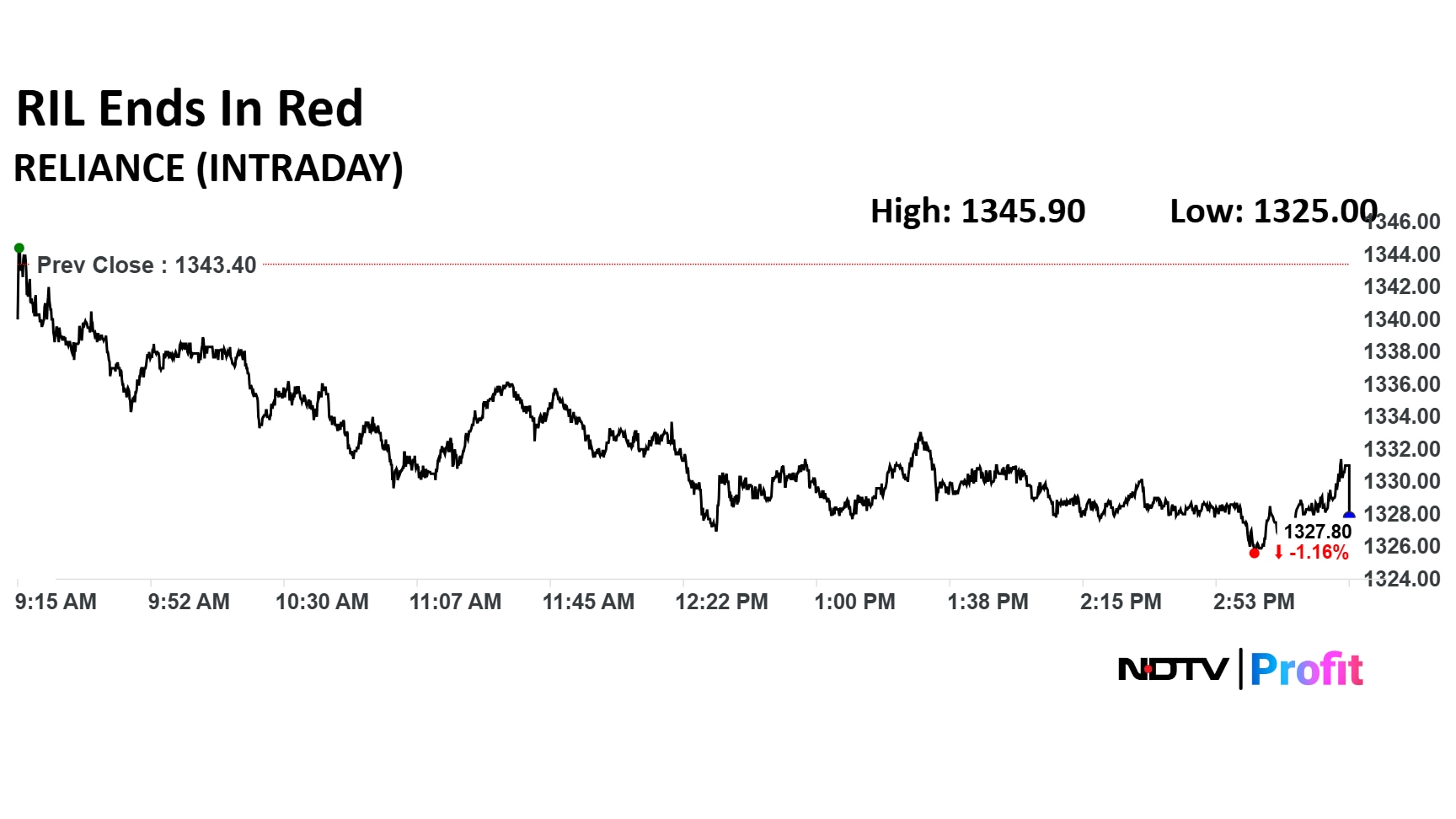

RIL Q4 Results Today Live Updates: Shares End In Red Ahead Of Results

The stock of Reliance Industries Ltd. ended over 1% lower at Rs 1,327.80 apiece on the NSE ahead of its fourth quarter results on Friday.

The decline compares to a 1.14% slump in the Nifty index.

RIL Q4 Results Today Live Updates: Petrochemicals Business Forecast

RIL's oil-to-chemicals segment's Ebitda is seen flat at around Rs 16,505 crore despite higher gross refining margins, weighed down by higher freight costs, insurance premiums, elevated gas costs, increased LPG output, and diversion of gas produced at the KG basin to priority sectors.

Oil and gas exploration Ebitda is projected to fall sharply by 12.5% to Rs 4,249 crore, the biggest drop in 16 quarters, due to lower volumes and higher costs.

RIL Q4 Results Today Live Updates: Reliance Jio Estimates

Reliance Jio is expected to post steady performance, with Ebitda projected to rise 3% to Rs 18,269 crore. Average revenue per user or ARPU is estimated to edge up to Rs 216 from Rs 214, supported by customer upgrades, while subscriber additions are seen slowing to 52.2 crore, the weakest quarterly addition in fiscal 2026.

RIL Q4 Results Today Live Updates: Reliance Retail Estimates

Reliance Industries' retail business is expected to see a 10.6% drop in revenue to Rs 87,568 crore, though Ebitda may rise 2% to Rs 7,051 crore due to cost management, with growth constrained by a high base.

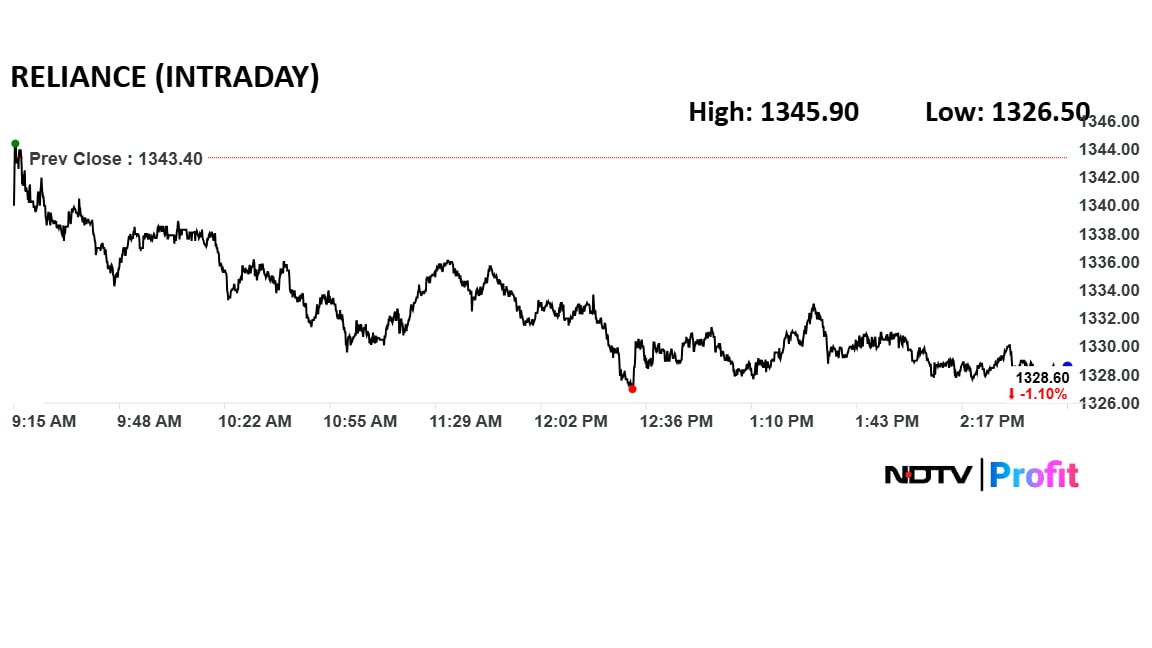

RIL Q4 Results Today Live Updates: Reliance Share Price Down Throughout The Day

RIL Q4 Results Today Live Updates: Reliance Industries Earnings Estimates

According to NDTV Profit estimates, consolidated revenue is seen rising 6.7% quarter-on-quarter to around Rs 2,82,748 crore, while operating income or Ebitda is estimated to increase 2.9% to about Rs 47,343 crore. Margin is expected to soften to 16.7% from 17.4% in the December quarter, and net profit is seen declining roughly 9% to Rs 16,944 crore.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.