Lower taxes on cigarettes under the Goods and Services Tax regime will boost stock prices and lift earnings of ITC Ltd., according to brokerages.

Overall tax per cigarette stick drops 7-9 percent on an average if prices don't change, Credit Suisse analysts wrote in a note to clients. Basic excise duty, as well as additional excise duty, will no longer be levied, but National Calamity Contingent Duty will continue, the brokerage added.

ITC could increase trade spends on cigarettes, increase incubation expenses in other products like dairy, chocolates, or launch a low-priced cigarette, at lower profits or a marginal loss in the interim to drive volumes, to comply with the anti-profiteering law, according to Deutsche Bank.

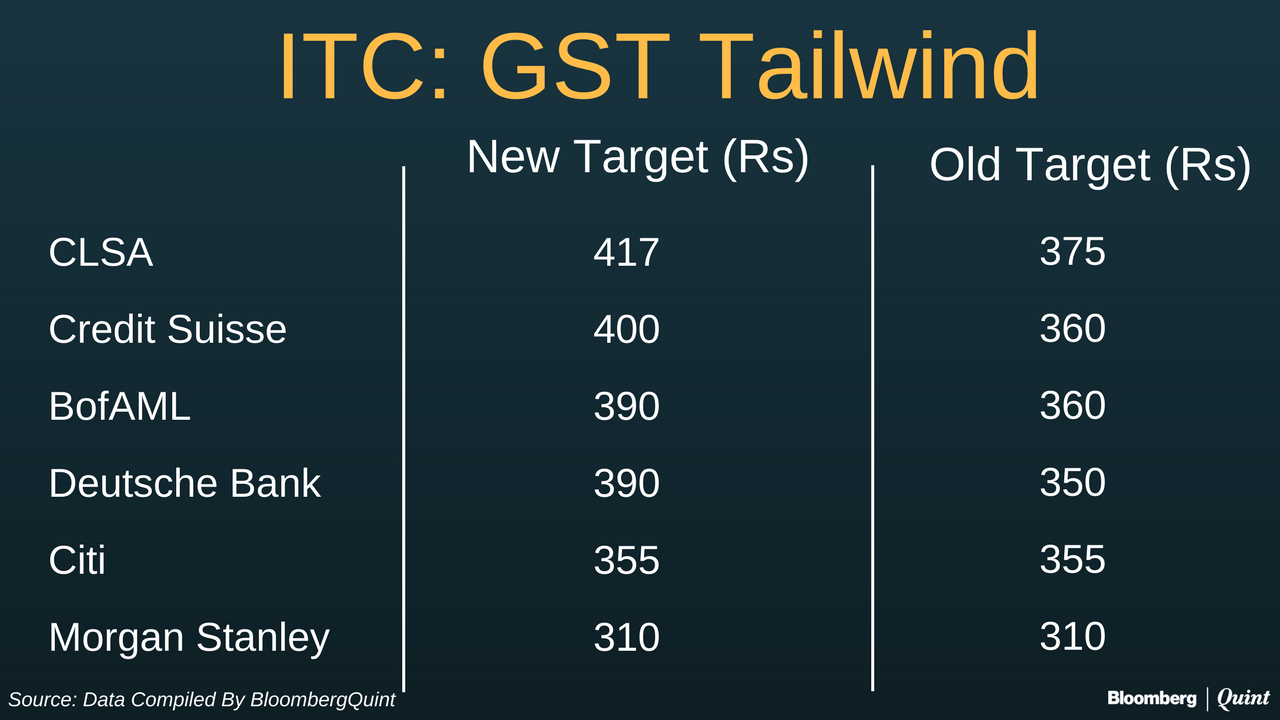

Brokerages including CLSA, Credit Suisse, Bank of America Merrill Lynch and Deutsche Bank raised their price targets on the ITC stock citing the benign regulatory regime and earings growth opportunities.

Here's more from what top brokerages had to say on ITC:

High-Teens Earnings Growth Expected

ITC is now likely to return to its historical trajectory of high teens earnings growth. We expect 3-4 percent volume growth in FY18 and 10-12 percent realisation growth, leading to around 15 percent growth in net sales in cigarettes. Our earnings CAGR over FY17-19 moves from around 14 percent to around 17 percent. Our operating estimates increase 5-6 percent, however reported estimates do not change as we adjust for the new accounting standards IND-AS.Arnab Mitra, Analyst, Credit Suisse

Predictability In Taxation

We expect ITC stock to rally in near-term as uncertainty regarding the final taxes in transition to GST is over. We increase target multiple to 33 times (from 30 times) as (1) the return of predictability in taxation could drive volume growth and better mix management, (2) opportunity to launch a lower-priced cigarette to drive growth in organized industry.Manoj Menon, Analyst, Deutsche Bank

Favourable Regime

The pendulum on legislative appears to be moving back in favour of the cigarette companies, after three years of brutal excise hikes. From an expectation that prices would be hiked substantially under the GST regime, the base case is definitely ‘status quo' on prices, while the bull case of price cuts is slowly emerging. We think this augurs well for the multiple on the stock, where expansion/compression is linked to prospective volume growth and also (indirectly) legislation. ITC remains a preferred pick in the large-cap FMCG space.Jamshed Dadabhoy, Analyst, Citi

Low-End Opportunity?

Over the past several years, consistent tax hikes have resulted in a large illicit market at the low end. We believe ITC should trim prices of its small-sized cigarettes to gain shares. ITC may also need to take some hit on channel inventory in the event of price cuts, but we do not see a big concern.CLSA's Note To Clients

Stocks Soar

The ITC stock surged as much as 9.6 percent to its lifetime high of Rs 354.8 in early trade. Stocks of other cigarette makers also surged:

- VST Industries Ltd. rallied as much as 8.6 percent to its record high of Rs 3,875.

- Godfrey Phillips Ltd. rose as much as 5.6 percent to Rs 1,330.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.