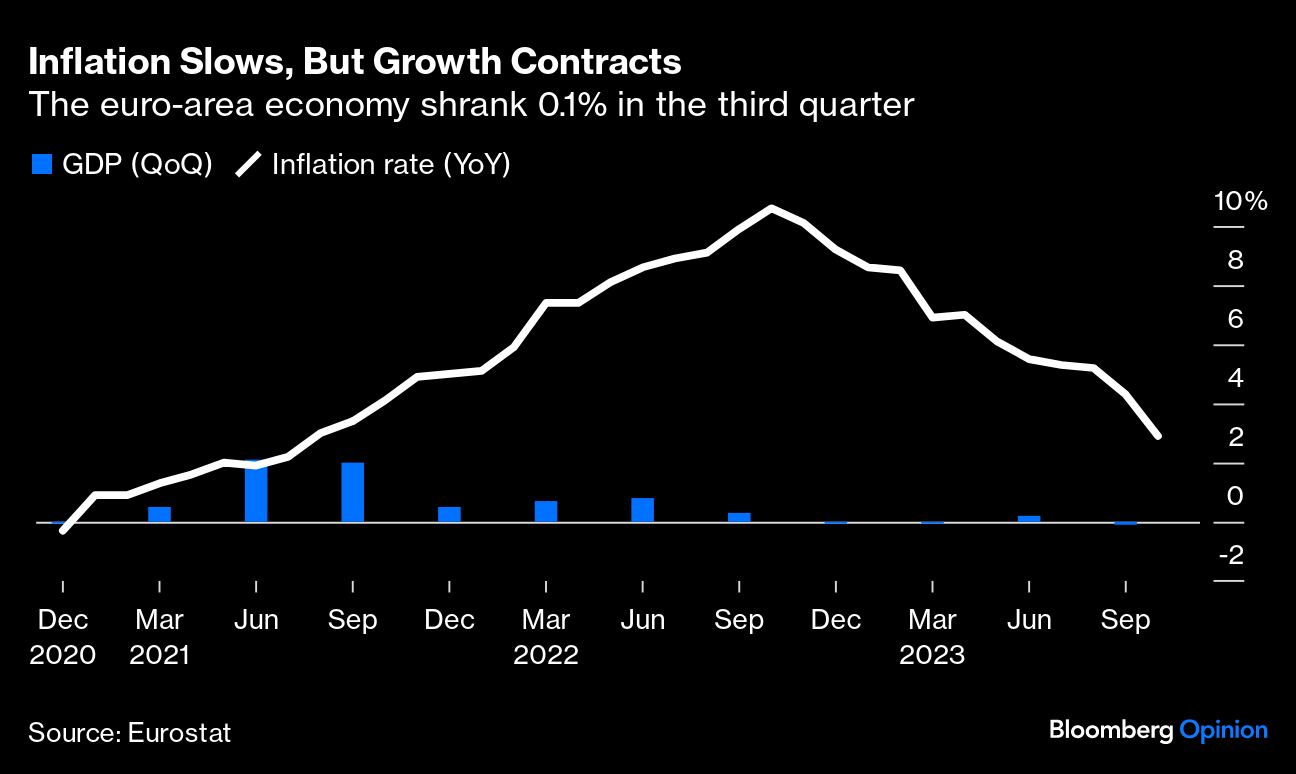

(Bloomberg Opinion) -- Recession looms for the euro area, with the latest batch of data showing momentum has evaporated. The economy contracted by 0.1% in the third quarter, most of the bloc's economies are flatlining, and Germany, its biggest engine of growth, is shrinking. Even supposedly good news, such as slowing inflation, just illustrates how quickly the outlook is deteriorating. It's time to improve coordination between fiscal and monetary policies, which worked wonders during the pandemic but risks being rendered pointless.

The European Central Bank should accept that its interest rate-hiking cycle is over. Inflation has declined to the slowest pace since Russia invaded Ukraine, as the base effects from the energy-price shock fall out. October consumer prices rose by just 2.9%, down from 4.3% in September. Higher for longer may be the current global central banker mantra, but before long it may dawn on the ECB that September's deposit rate increase to 4% was a step too far. While the inflation element of stagflation is under control, stagnation still stalks the region.

The Governing Council is adamant that it's not ready to contemplate lowering borrowing costs, with core inflation still running at more than double the ECB's 2% target. However, money-market futures have already fully priced in the first rate cut from April next year, with two additional quarter-point reductions anticipated by this time next year — a doubling of what was expected just two weeks ago. Expectations are changing fast and may well start to price in deeper cuts if the economy continues to worsen.

Third-quarter earnings from euro-area businesses highlight the gulf with the US. With nearly half of the Euro Stoxx 600's companies reporting so far, 57% have beaten estimates with earnings per share falling 8% annually, according to JP Morgan Chase & Co. analysts. This is some way behind the S&P 500 picture, where 78% of companies beat expectations and average EPS has grown 12%. The US economy has been consistently stronger than the euro area since the pandemic, but the gap widened in the past quarter. European equities are cheap for a reason.

Monetary tightening is starting to bite — “tight policy is showing effect,” prominent hawk Bundesbank chief Joachim Nagel conceded following the governing council's decision last week to pause on rates. Deputy President Luis de Guindos emphasized "the risks to the growth outlook are tilted to the downside," noting that the slowdown could be exacerbated if it turns out that the central bank's squeeze is even more effective than anticipated.

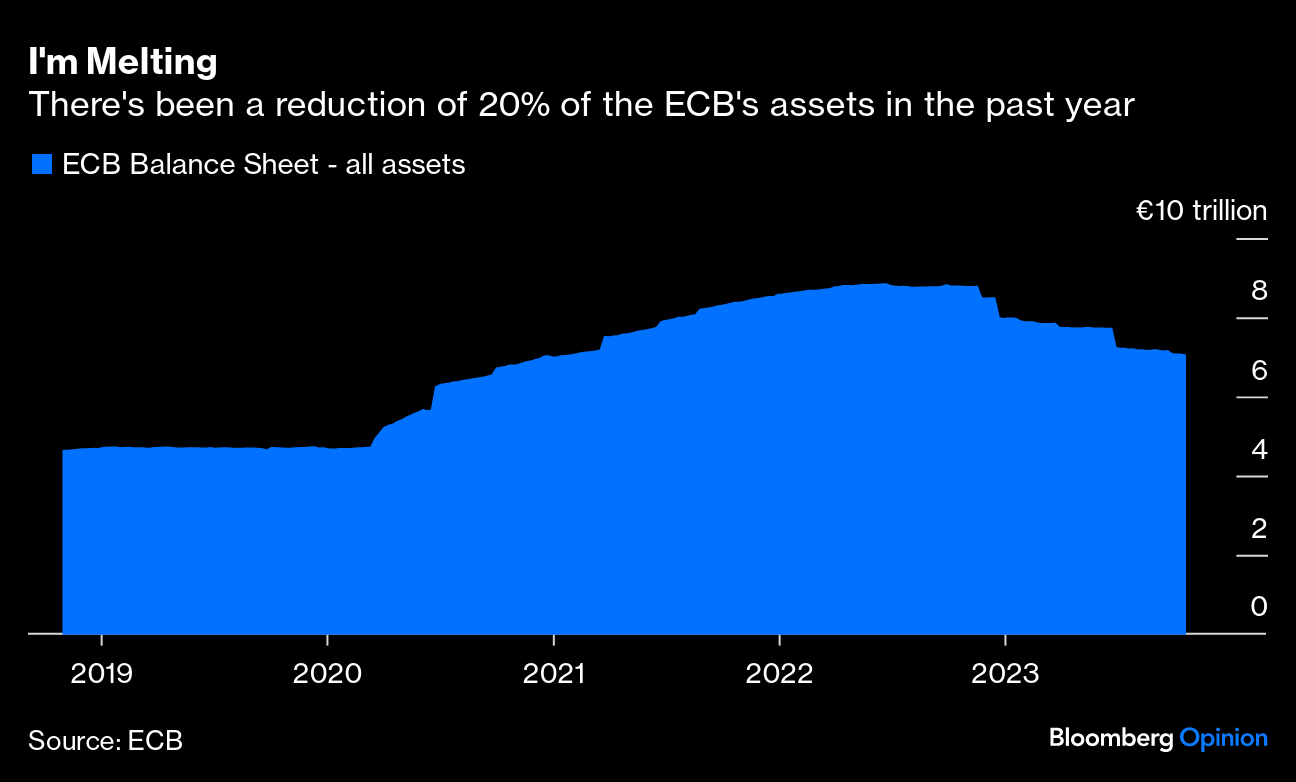

That's a clear and present danger. Following eight years of a negative rate regime, a sudden 450 basis points of tightening in little over a year is delivering a shock to the euro region. Furthermore, the monetary pinch isn't just about higher official rates. The ECB's balance sheet has shrunk by 20%, or nearly €7 trillion ($7.4 trillion), in less than a year. It's also withdrawn super-generous commercial bank loans, and has stopped paying interest on reserves that banks have to keep with it.

Italian debt, the region's weakest link, has weathered the surge in bond yields relatively well, with 10-year borrowing costs holding at around 200 basis points above German bunds. But there's no sense in tempting fate by accelerating the unwind of the ECB bond holdings.

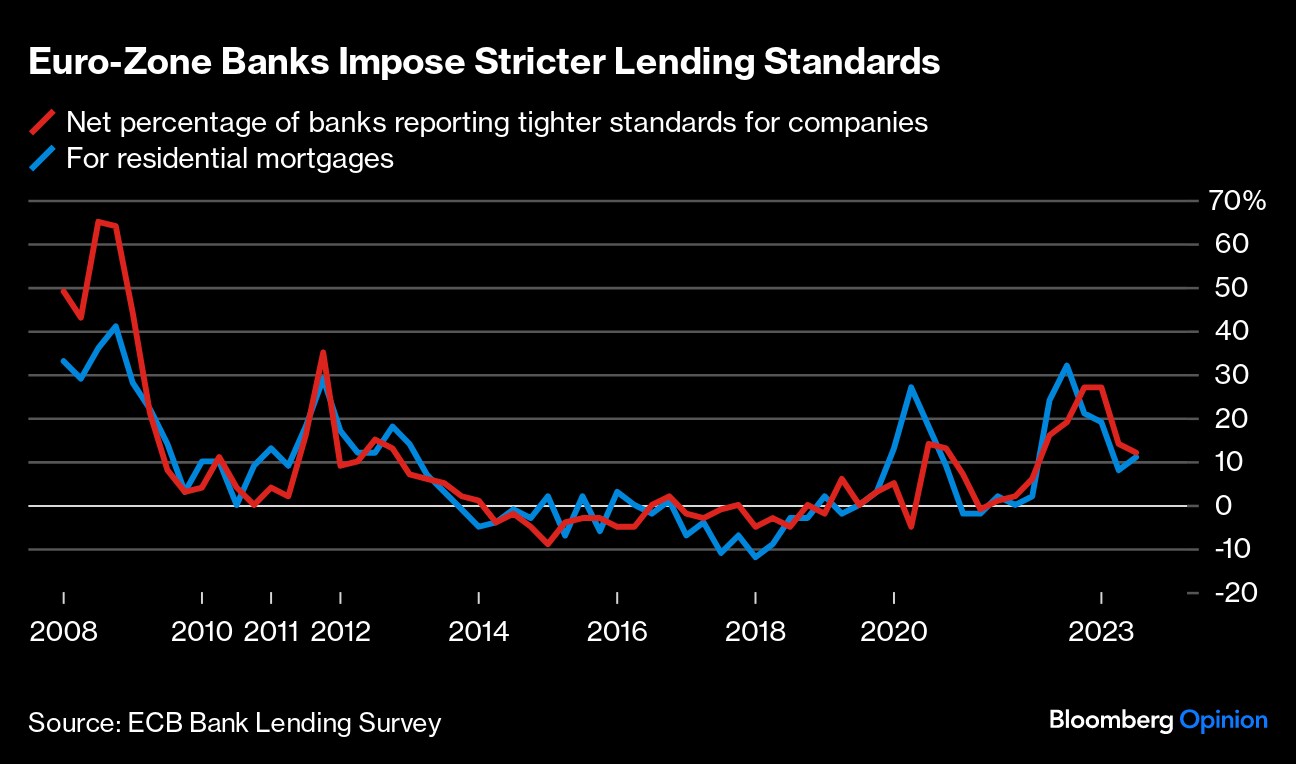

It's hard to be optimistic about the prospects for an economic recovery. Trade talks with the US, Australia and the South American Mercosur bloc have all foundered recently. The real economy is struggling as purchasing managers' surveys are looking pretty grim. Euro-area manufacturing is firmly into the contraction zone at 43 in October, and even the services sector at 47.8 is well below the 50 growth line. Money-supply aggregates have all turned negative. Moreover, the ECB's third-quarter bank-lending survey displayed a further tightening of credit standards. With corporate net demand for loans decreasing substantially, not only is the of credit waning but so is the .

Deutsche Bank AG economists expect the German economy, the region's largest, to contract by 0.5% this year. Though third-quarter growth was not as weak as expected, the International Monetary Fund expects Germany to be the weakest of the major economies this year. German manufacturing PMI hit a low of 38.8, which implies a deep recession.

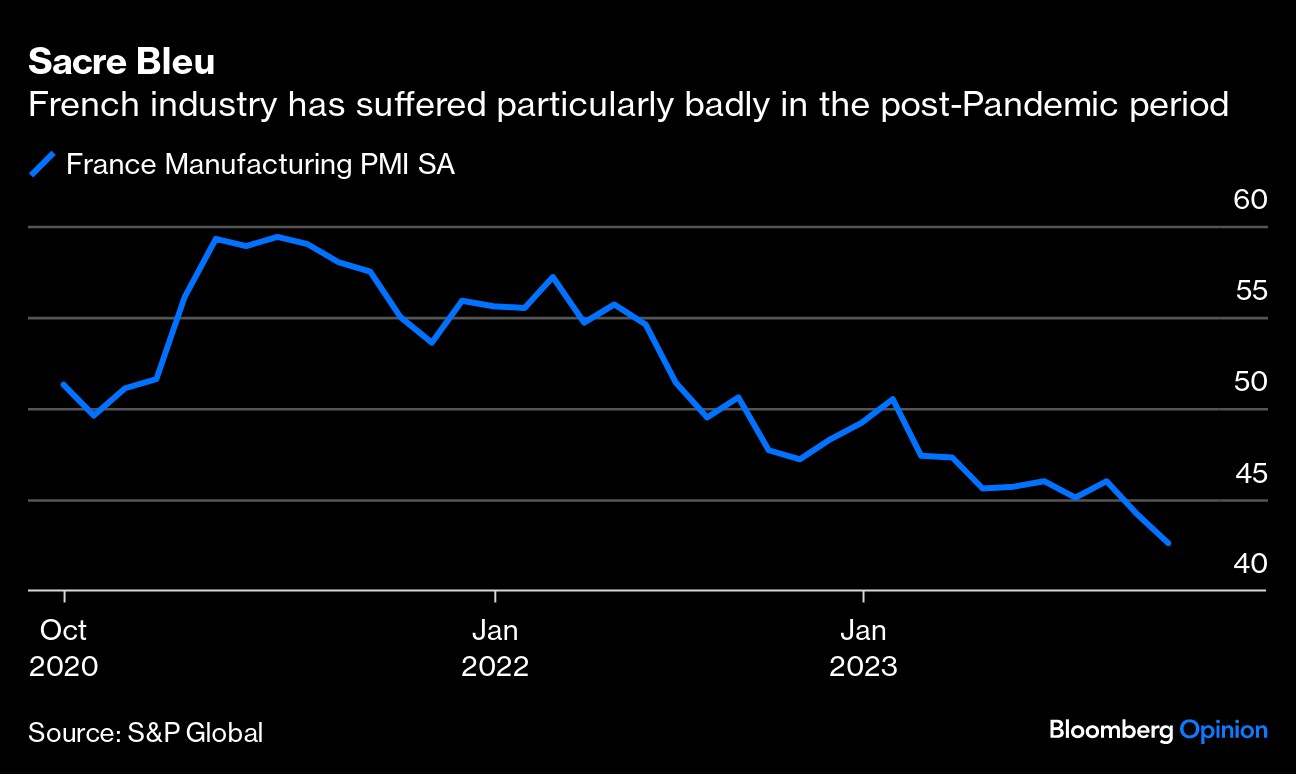

However, it is the speed with which the French economy has turned down that is even more concerning. October's manufacturing PMI came in at 42.6, down from 57.2 only 18 months ago. It's scant consolation that growth was 0.1% in the third quarter, with a boost from household spending still leaving it well off the pace seen earlier this year.

There are patches of relative strength, with Spain and Belgium showing a modicum of growth, but countries like Ireland, the Netherlands and Austria are already in or teetering on the edge of recession. More worrying evidence is coming from the labor market, with the German IFO Institute survey of companies' willingness to hire falling to the lowest level since February 2021.

This stagnation comes after the fiscal spigots have already been opened. The €800 billion pandemic recovery fund is in full deployment mode and several countries, notably Germany, have been effusive in upscaling domestic government expenditures. But this only serves to underscore the dilemma facing the euro area. There's little point in governments splurging in an attempt to jumpstart their economies if the private sector is being choked by the ECB's monetary strictures. More joined-up thinking is needed if the bloc is to avoid a deeply damaging recession.

More From Bloomberg Opinion:

-

BOJ Shuffles Away From YCC, But Don't Tell Anyone: Moss & Reidy

-

Americans Like Sharing Bad Economic News Too Much: Claudia Sahm

-

Italian Bonds Are at the Mercy of the ECB: Marcus Ashworth

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. Previously, he was chief markets strategist for Haitong Securities in London.

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.