(Bloomberg Businessweek) -- Two decades ago, Blackstone Inc. made a bet that India could be its next frontier. The firm set up an office in Mumbai in 2005 and soon pumped piles of cash into minority stakes in more than a half-dozen companies. Within two years, the investment giant was in retreat, forced to write some of its bets down to almost zero. “We were new to India, and we were learning,” says Amit Dixit, Blackstone's head of Asia for private equity. “The sector was finding its feet.”

Blackstone persevered, replacing its India boss and insisting on buying only majority stakes. After assiduously courting a new class of entrepreneurs and helping connect its Indian properties to companies it controls around the world, the firm has built a thriving business there. Today, Blackstone says India has become its third-biggest investment market, after the US and the UK, and its returns from India are better than those from any other country.

India has become a bright spot for private equity firms as its strong economic growth, a vast talent pool and regulatory changes have made it easier to do business there. And with flagging interest in China, foreign funds are steering more resources to the world's most populous nation—though they still face challenges such as complicated tax rules and roadblocks to purchases of publicly traded companies.

In the past decade, international firms have boosted their investment in India fivefold, according to consultants Bain & Co. Funds that once settled for a minority share in established family-owned companies are now buying majority stakes of the hottest startups. And a growing stock market has enabled fund managers to sell their holdings quickly, helping return cash to their investors.

Read More on the Topic

KKR Bets on Domestic Consumption, Private Credit in India Push

Carlyle Is Weighing Entry Into Private Credit Market in India

Until the 1990s, India was almost completely closed to foreign capital, and few private equity funds were involved in marquee deals. A relaxation of rules around the turn of the century unleashed a rush into the country, with most of the biggest global funds firmly established there by 2006. But despite some early successes by Warburg Pincus LLC, the market was tough to crack because remaining government restrictions made it difficult for foreigners to take majority stakes, giving them limited leverage over decision-making. And Indian entrepreneurs, unfamiliar with private equity, were reluctant to sell stakes in their companies to PE firms.

Over time, the cash-rich outsiders demonstrated they could profitably stage initial public offerings of their companies. And the notion that it's OK to delegate decisions to professional managers became more acceptable, says Gaurav Trehan, the Asia private equity chief at KKR & Co. “As more and more got done and as more and more success stories happened, people became comfortable that you can run a company in India without a founder,” Trehan says.

In recent years, PE firms have been adding staff in Mumbai, funding sectors across the entire economy. KKR has invested in eyewear maker Lenskart and school operator Lighthouse Learning Group, and it's plowed about $3 billion into roads, renewable energy and traditional power generation. Carlyle Group Inc. has a stake in VLCC, which develops weight-loss solutions. Sweden's EQT AB works with Indira IVF, a chain of fertility clinics. Blackstone holds stakes in more than 80 companies and has become the country's largest commercial landlord.

PE firms say India's growth potential means they rarely resort to the restructuring or job cuts that they often implement elsewhere. Instead, they can make their companies stronger by improving efficiency and expanding the scope of their business, says Vishal Mahadevia, head of Asia private equity for Warburg Pincus. “If we're going to improve a company's top-line growth,” he says, “it's because we've added a hundred more salespeople who can win market share and go into new markets.”

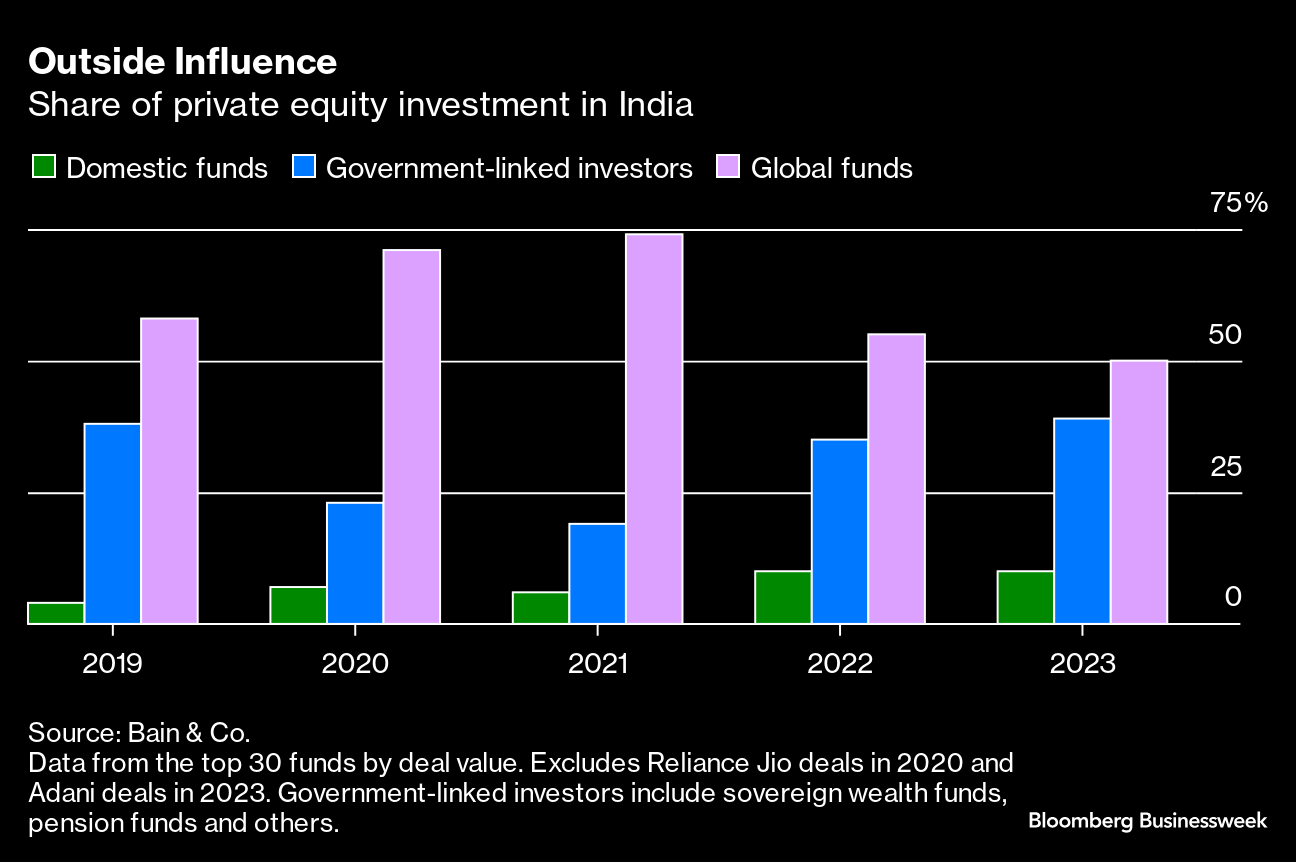

Although India has an expanding crop of homegrown private equity firms, they struggle to compete with the global giants, whose deeper pockets let them buy bigger, stronger businesses and better weather economic ups and downs. And the bigger firms' experience in and access to other markets helps them take their portfolio companies beyond India, pooling resources to boost their success. In recent years, international companies have accounted for as much as three-quarters of PE investments by top funds in India, Bain says. “India has become a two-track private equity market of haves and have-nots,” says Sunaina Sinha, global head of the private capital advisory group at Raymond James Financial Inc. “It is dominated by global funds.”

With their higher profile, the foreigners have sought a relaxation of rules in a regulatory environment that's long been wary of outside capital. A couple of years ago, when Prime Minister Narendra Modi met Blackstone Chief Executive Officer Stephen Schwarzman, they spoke about India's tough laws on taking listed companies private, according to people familiar with the matter. And several funds have asked regulators to ease requirements calling for disclosure of the identity of any foreigners participating in an investment, which they say impede capital flow into the country, say the people, who asked not to be identified discussing sensitive conversations.

Private equity managers want India's laws on mergers, acquisitions and bankruptcy to mirror those in more established markets. A deal that might be wrapped up in a few months in the US can take years in India, says Jonathan Gray, Blackstone's chief operating officer. Gray points to what he says are onerous taxes for real estate investment trusts and regulations that bar banks and insurers from investing in them and require others to hold their stakes for at least three years. REITs are “still regulated as if they're a different animal,” Gray told reporters during an April event in Mumbai.

Industry insiders say the growing interest in India is forcing PE firms to cough up more money as the surging stock market has made IPOs a more attractive option for target companies. Advent International LP had to almost double its offer to close a 2022 deal with snackmaker DFM Foods Ltd. Another snackmaker, Haldiram's, is exploring an IPO after disappointing negotiations with PE firms. “People are becoming more interested in India, and obviously that leads to higher valuations,” says Shweta Jalan, Advent's India chief.

Few fund managers predict India will displace China as Asia's largest PE market anytime soon, as its neighbor's economic heft means it can still absorb more capital. But India's share of Asia-Pacific deals jumped to 20% in 2023, from 15% five years earlier, Bain says. And the potential for growth in domestic consumption combined with India's strengths in information technology, pharmaceuticals and services all augur further growth. “Very few economies in the world can compare with India,” says Amit Jain, head of Carlyle India Advisors Pvt Ltd. “You come into the country, and your companies play at scale.”

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.