Shares of Shankara Building Products Ltd. have more than tripled since listing in April as the company is expected to benefit from the growing share of its higher-margin retail business after the Goods and Services Tax.

Shares of the home improvement and building products seller rose as much 3.5 percent on Friday, before erasing gains. It's returned 223 percent since making its stock market debut on April 5. The company had sold shares at Rs 460 a piece in its initial public offering.

“GST implementation will have a positive impact on Shankara because customers dealing with unorganised players will now shift to the organised market,” Amit Purohit, an analyst at brokerage Emkay Global, told BloombergQuint. The impact will be gradual, he said.

A chunk of the construction and building material retail market was unorganised. The nationwide tax is expected to push it towards a formal economy. Besides mandatory registration for businesses with a turnover of more than Rs 20 lakh a year, the new levy creates a trail of input tax credit. Pushing undeclared goods is difficult as it will break the input tax credit chain.

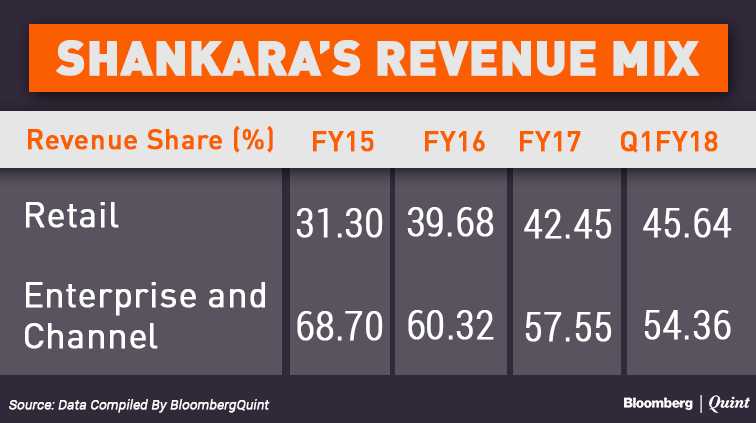

Shankara Building has three business segments – retail, enterprise and distribution channel. The company has been increasing the focus on the retail segment, which has higher margins.

Revenue from retail segment grew at a compounded annual growth rate of 26 percent over the last five years. That compares with a decline in the enterprise and channel category.

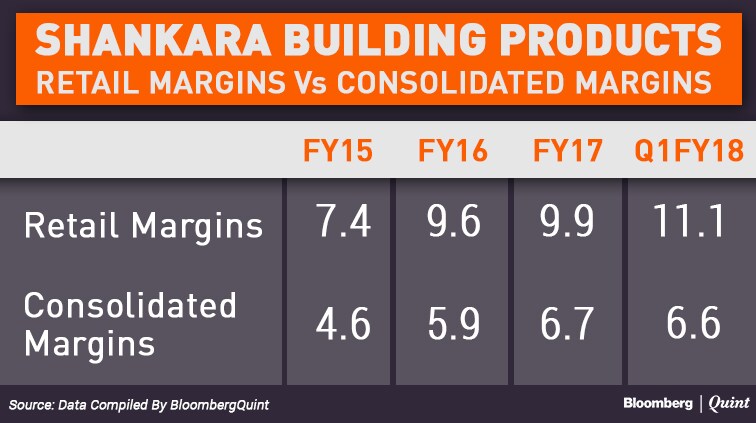

Shankara Building's earnings before interest, tax and depreciation and amortisation margin is around 6-7 percent on a consolidated basis. Operating margin from the retail business is four percentage points higher.

The company's same-store sales rose an average 18 percent over the last five years. It has 115 outlets and plans to add 20 every year.

Other Financial Highlights

- Net worth rose 2.5 times in last six years to Rs 394 crore

- Total debt-to-equity stands at 0.7 times

- Return on equity is 18 percent

- Return on capital employed at 25 percent

Brokerage Take

Emkay

- Buy with a target price of Rs 1,497

- Expects return on capital employed to improve to 30 percent by year to March 2020

- Same-store sales growth expected to stay at 18 percent level for the next three years

Edelweiss

Buy with a target price of Rs 1,575

- Expects revenue/net profit to grow at CAGR of 25/40 percent over three years to March 2019

- Debt-to-equity ratio to reduce over the next two years

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.