Teller agents discuss the authenticity of a Five Hundred Rupee currency note tendered by a customer at its Connaught Place branch in New Delhi (Photographer: Amit Bhargava/Bloomberg News)

International broking firm Goldman Sachs expects to see an earnings turnaround for the Indian banking and financial services industry as their “confidence in green shoots” rises.

“We revise FY18-19E earnings per share estimates by 1-6 percent on average (as banks recover from downgrade cycle) driven by better NIMs/operating efficiency,” it said in a research note.

Goldman cited four key reasons for its bullish view.

- Expectations of credit growth improvement

- Most large NPL being already recognised

- Better fee income

- Gains in operating efficiency

Goldman's View

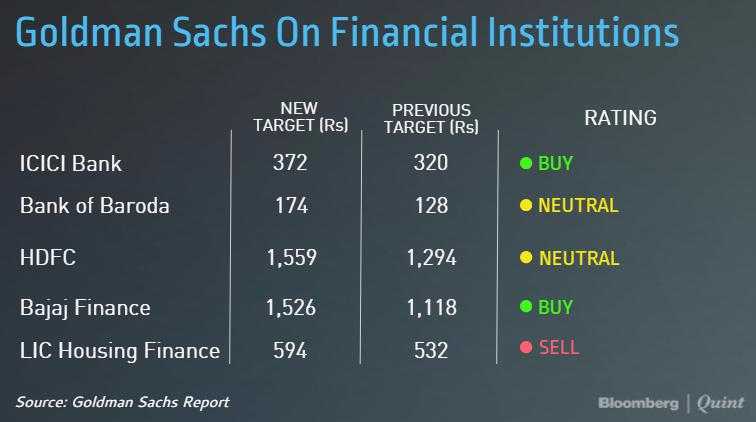

On ICICI Bank

- Rating: Buy

- Price Target: Raised to Rs 372 from Rs 320

- Expect non-performing loans (NPLs) to improve.

- See gradual recovery in the credit growth.

- Expect earnings to improve by FY19 as large part of the corporate stress has been recognised.

- Expect 16 percent compounded annual growth rate in earnings over the FY17-20 period.

- ICICI Bank better positioned compared to peers from capital standpoint.

On Bajaj Finance

- Rating: Buy

- Target Price: Raised to Rs 1,526 from Rs 1,118

- Raised FY19 earnings per share estimate by 10 percent on the back of higher growth and fee income estimates

- Expect 31 percent compounded annual growth rate in earnings over the FY17-20 period.

- Rising credit card transactions is a key positive.

- Diversified product portfolio with limited competition beneficial for the company.

- Expect Bajaj Finance to deliver in FY19 on operating efficiency and stable credit costs.

On Bank Of Baroda

- Rating: Neutral

- Target Price: Raised to Rs 174 from Rs 128

- Expect 12 percent compounded annual growth rate in earnings over the FY17-20 period.

- Capital raising in Q4 likey to strengthen the balance sheet.

- Expect operating performance and loan growth to pick up in FY19-20

- Weaker profitability remains concern.

- Expect impaired loan ratio to drop 7.8 percent by FY19.

On HDFC

- Rating: Neutral

- Target Price: Raised to Rs 1,559 from Rs 1,294

- Expect core earnings trajectory to improve in double-digits in near-term.

- Improvement in housing affordability would lead to rebound in loan growth.

- Expect lending spreads to remain tight over FY18-20

- Expect 16 percent compounded annual growth rate in earnings over the FY17-20 period.

- Marginally raised earnings per share estimates by 2-4 percent for FY18-19.

On LIC Housing Finance

- Rating: Sell

- Target Price: Raised to Rs 594 from Rs 532

- Expect 17 percent compounded annual growth rate in earnings over the FY17-20 period.

- Expect 10 basis points decline in NIMs to 2.5 percent in FY19

- Margins likely to remain capped due to intense competitiveness.

- Operating profit likely to decline 15 percent over FY17-20

- Higher than expected volumes on affordable housing could turn negative for the finance company.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.