India's consumer sector has been one of the worst affected by the government's decision to demonetise Rs 500 and Rs 1,000 currency notes. In the July-September quarter, volume growth remained tepid and earnings took a hit as a result of the cash crunch that ensued. And third quarter earnings could worsen on account of emerging headwinds from input cost inflation, Religare Capital Markets said in a report on Friday.

The brokerage expects aggregate sales to decline 0.9 percent in the quarter and adjusted profit after tax to fall 3.7 percent in the October-December quarter. Margin on earnings before interest, tax, depreciation and amortisation may contract 75 basis points. The moderation in advertising spend may cushion the hit on margins, but only to a limited extent.

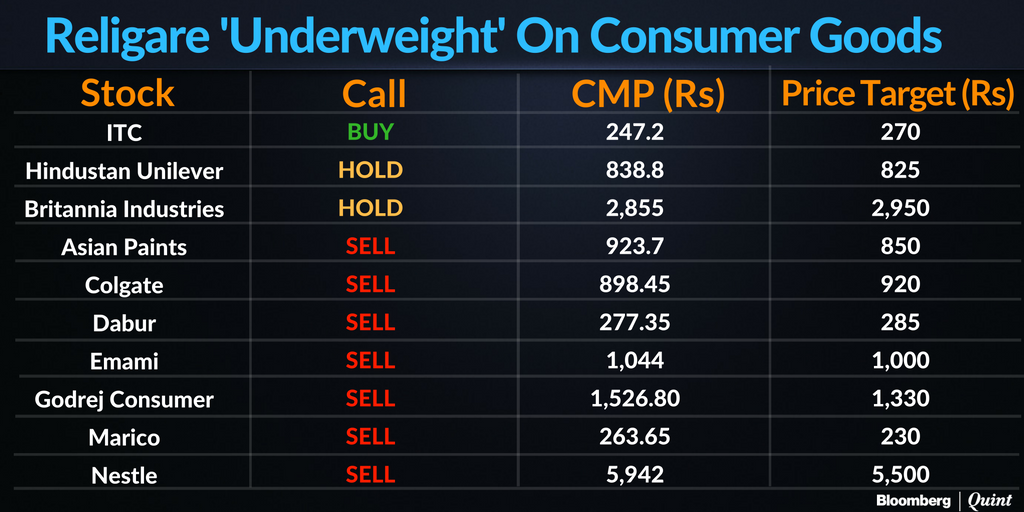

Religare continues to maintain a negative stance on the sector.

Also Read: Delayed Demand Recovery, Rising Input Costs To Hit Consumer Sector In 2017

Impact On HUL, ITC

Consumer major Hindustan Unilever Ltd. had a disappointing second quarter on the volume growth front. The company saw volumes decline by 1 percent compared to a 4 percent growth in the first quarter of financial year 2016-17.

Religare is pricing in a similar decline in volume growth for the third quarter as well. However, it maintains a ‘hold' rating on the stock with a price target of Rs 825 as a good winter season can offset the company's muted volume growth trajectory.

ITC displayed a steady set of numbers in its second quarter. Though margins remained on the flatter side, the company saw healthy growth in its cigarette volumes.

However, with a high base, sudden disruptions in value chains and a sharp cut in advertising spends is likely to result in margin contraction as well as decline in volumes by as much as 3 percent for ITC.

Despite the headwinds, a favourable risk-reward profile makes ITC the most favoured pick for Religare as well as the only consumer stock with a ‘buy' rating with a price target of Rs 275.

Also Read: Demonetisation Pushes FMCG Stocks To The Back Shelf

Advice To Investors: Stay Cautious

Consumer demand has remained tepid over the last two years. Poor demand, coupled with headwinds from demonetisation and GST, “could have a lasting disruptive impact on the indirect distribution value chain, pushing back recovery to the second half of financial year 2017-18”, the brokerage says.

Religare expects urban-focussed, retail franchise and direct to consumer players to be less affected. A shift to formal channels from the unorganised sector is likely to benefit the retail players, it points out.

Religare's Top Picks

ITC remains Religare's top pick. It is also the only stock where the brokerage has a ‘buy' rating. It has a ‘Hold' rating on HUL and Britannia and a ‘sell' rating on stocks like Asian Paints, Godrej Consumer, Colgate, Marico, and Nestle India.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.