Asian equities were mixed at the open, and gold and the yen maintained their gains as traders awaited further developments on the North Korea front.

The Singapore-traded SGX Nifty, an early indicator of NSE Nifty 50 Index's performance in India, gained 0.17 percent to 9,943 as of 6:45 a.m.

Here's a quick look at all that could influence equities on Tuesday.

Global Cues

- S&P 500 Index futures were modestly higher with the cash market closed on Monday for Labour Day.

- European stock markets dropped across the board, with the Stoxx Europe 600 index snapping a three-session winning streak.

Asian Cues

- Japan's Topix index swung between gains and losses, while South Korea's Kospi index rose 0.2 percent. Australia's S&P/ASX 200 Index slipped about 0.1 percent.

- Contracts on Hong Kong's Hang Seng Index were 0.2 percent higher.

- The MSCI Asia Pacific Index declined 0.1 percent. It slid 0.6 percent on Monday, the steepest drop since Aug. 11.

Commodity Cues

- Gold was trading at $1,333.48 an ounce, little changed after a 0.6 percent gain.

- West Texas Intermediate crude climbed 0.2 percent to $47.39 a barrel.

- ICE Sugar ended flat 13.75 cents a pound

Shanghai Exchange

- Steel trades lower; down 0.41 percent

- Aluminium trades lower; down 0.66 percent

- Zinc trades lower; down 0.17 percent

- Copper trades higher; up 0.42 percent

- Rubber trades higher for fourth day; up 0.61 percent

Earnings To Watch

- Aegis Logistics

- Ortel Communications

- Sharda Motors

- Skipper

Earnings Reaction To Watch

FIEM Industries (Q1FY18, YoY)

- Revenue grew 19.7 percent to Rs 325.5 crore

- EBITDA unchanged at Rs 31 crore

- Margin at 10.7 percent from 12.7 percent

- Profit fell 13 percent to Rs Rs 10 crore

Gandhi Special Tubes (Q1FY18, YoY)

- Revenue grew 6.9 percent to Rs 31 crore

- EBITDA up 11.1 percent to Rs 10 crore

- Margins at 35.7 percent from 34.6 percent

- Profit went up 1.1 percent to Rs 8.8 crore

Manali Petro (Q1FY18, YoY)

- Revenue down 4.7 percent to Rs 163 crore

- EBITDA fell 62 percent at Rs 6 crore

- Margins at 4.1 percent from 10.2 percent

- Profit declined 81.8 percent to Rs 2 crore

Stocks To Watch

- Reliance Housing Finance will be demerged from Reliance Capital. ICICI Direct valued Reliance Housing at Rs 115-119 per share. Edelweiss valued it at around Rs 137 per share.

- Gujarat Textile in focus as Gujarat government extends Textile Policy 2012-17 for one more year

- Shriram Transport says merger talks with IDFC still on

- Indraprastha Gas is said to win India's Karnal City Gas license, according to Bloomberg

- IRB Infra starts toll collection, construction at Udaipur tollway

- Karnataka Bank reduces one year MCLR by 5 basis point to 8.85 percent per annum

- Indian Overseas Bank allots 2.85 percent stake to government on a preferential basis

- LIC sells 2 percent stake in Bank of Baroda as per exchange disclosures

- American PE firm Marigold Capital agrees to acquire Leela Palace Chennai property for Rs 700 crore (Economic Times)

- Thomas Cook in race to acquire IFCI's 26.09 percent stake in Tourism Finance Corp (Mint)

Bulk Deals

- Career Point: Fidelity Asian Values sold 11.8 lakh shares (3.1%) at Rs 125.75 each

- Religare Enterprises: HDFC sold 11.35 lakh shares (0.6%) at Rs 44.71 each

- Apex Frozen Foods: BNP Paribas Arbitrage sold 2 lakh shares (2.3%) at Rs 211.95 each, while GIRIK Wealth bought 3.1 lakh shares (3.5%) at Rs 211.91 each

Rupee

- The rupee closed at 64.05 a dollar, down 0.04% from its Friday's close of 64.03.

Top Performers In Second Quarter

- Himachal Futurist Communication: Up 81.9 percent

- Bombay Dyeing & Manufacturing: Up 66.9 percent

- Future Consumer: Up 61.1 percent

- Sterlite Technologies: Up 57.9 percent

- Future Retail: Up 54.7 percent

Worst Performers In Second Quarter

- Religare Enterprises: Down 74.6 percent

- Nitin Fire: Down 55.9 percent

- JMT Auto: Down 39.4 percent

- JBF Industries: Down 35.9 percent

- J.Kumar Infraprojects: Down 35.5 percent

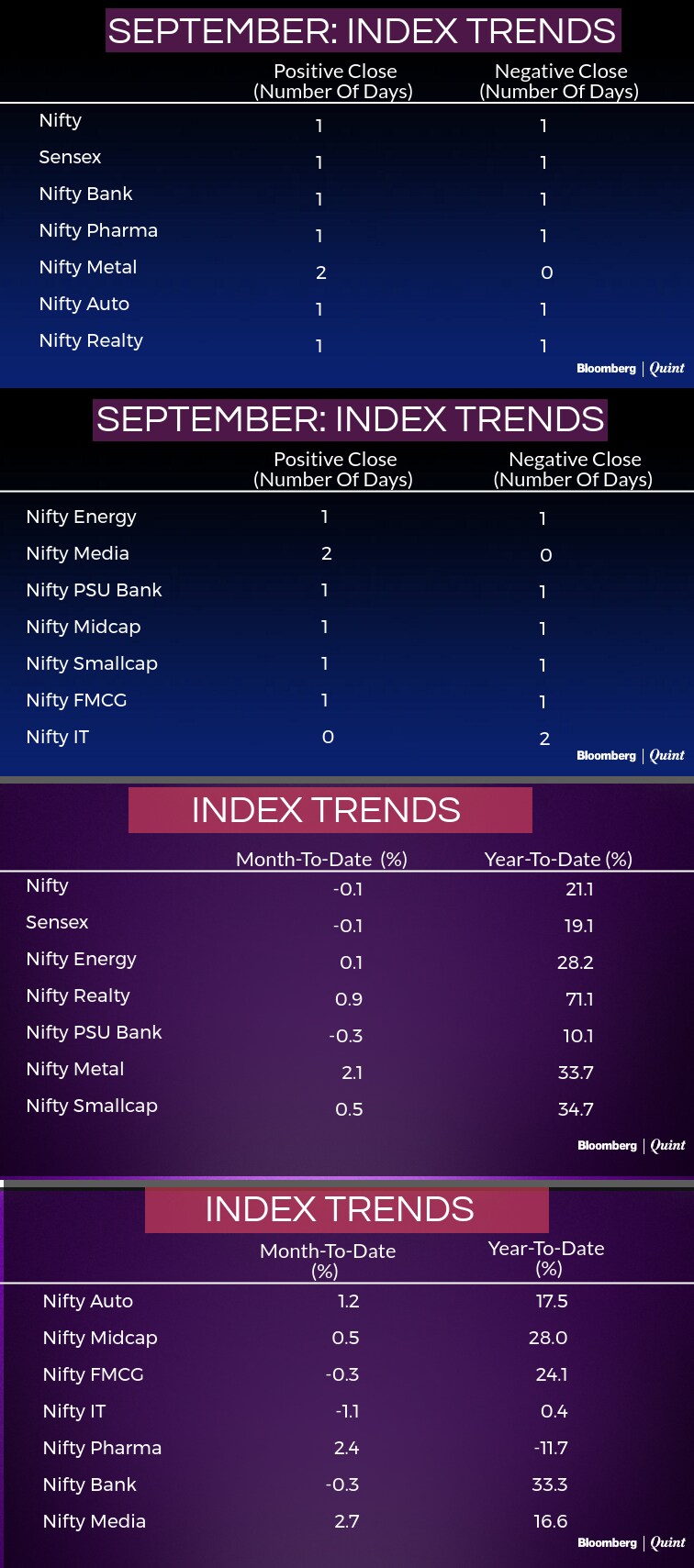

Index Trends

F&O Cues

- Nifty September futures closed at a premium of 14.6 points from 33 points earlier

- Nifty September futures closed at 9927.65, open interest up 3 percent

- India's volatility index surged 12.7 percent to close at 13.1

- September series' highest call base at 10000 (open interest at 44.6 lakh, open interest up 27 percent)

- September series highest put base at 9700 (open interest at 44.6 lakh, open interest up 11 percent)

- Call strikes 9,900, 10000, 10,100 see open interest addition

- Put strikes 9,600, 9700 see open interest addition & unwinding seen at 9900

F&O Ban

- In Ban: Indiabulls Real Estate, JSW Energy

- New In Ban: JSW Energy

- Only intraday positions can be taken in stocks which are in F&O ban, in case of rollover there is a penalty

Put-Call Ratio

- Nifty PCR at 1.30 from 1.38

- Nifty Bank PCR at 0.92 from 1.15

Stocks Seeing High Open Interest Change

- Oil India saw open interest addition of 21 percent on long side

- United Spirits saw open interest addition of 14 percent on long side

- Berger Paints saw open interest addition of 11 percent on short side

- IOC saw open interest addition of 11 percent on short side

- Tata Elxsi saw open interest addition of 9 percent on long side

- OFSS saw open interest addition of 9 percent on long side

- Cipla saw open interest addition of 9 percent on short side

- IndusInd Bank saw open interest shedding of 9 percent, long unwinding seen

Fund Flows

Brokerage Radar

CLSA on United Spirits

- Maintain Sell; hike target price to Rs 1,750 from Rs 1,600

- Upside from IPL drives 13-15 percent EPS upgrades to FY19-20

- Maintain Sell on earnings risk due to a tough regulatory environment

- Continue to value alcohol business at 22x EV/EBITDA and value the IPL at $380 million

Credit Suisse on Sun TV

- Maintained Outperform with target price of Rs 980

- Sun to witness strong FY19 with IPL and TN digitisation

- Tamil Nadu digitisation to give Sun Rs 20 per subscriber

- Subscription revenue to grow at 25 percent CAGR over FY17-19

- IPL to go from Rs 30 crore loss to Rs 130 crore profit in FY19

CLSA on Sun TV

- Maintain Buy; hike target price to Rs 965 from Rs 890

- Upgrade FY19 IPL revenues by 45 percent

- Sun TV to earn profit before tax of Rs 150-170 crore in FY19-20

- Strong subscription outlook with digitisation rolling in Tamil Nadu

- Subscription revenue to grow at CAGR of 20 percent over FY17-20

- Triggers:- Advertising growth, strong subscription revenue and IPL

Credit Suisse on Bharat Financial Inclusion

- Maintained Outperform; Hike target price to Rs 1,055 from Rs 920

- BFIL gained 60 basis points market share to 9.1 percent of micro-finance institution assets in India

- BFIL continues to enjoy best funding costs, employee productivity ratios and geographic reach

- BFIL remains one of the best capitalised players in the market

- FY19/20 EPS estimates hiked by 3/6 percent on better long-term outlook

Citi on Indraprastha Gas Management Meet

- Maintain Buy with target price of Rs 1,390

- Expect volumes to grow at CAGR of 10 percent in next 2-3 years

- Capex to rise to more than Rs 1,000 crore in next 2 years

- Expects access to rest of Gurgaon (current 25 percent) in next court hearing on October 4

- Citi expects ample scope of higher payouts given healthy financials

ICICIDirect on Reliance Housing Finance

- Expect Listing at Rs 115-120

- RHF management targets AUM to reach Rs 50,000 crore by FY20

- RHF management expects return on equity to sustain at 15 percent

- RHF networth seen at Rs 1,400-1,500 crore at time of listing

- Reliance Capital's market price can adjust lower by Rs 70-80 a share post demerger

Edelweiss on Reliance Housing Finance

- RHF valued at Rs 3,360 crore translating to Rs 137 a share

- Demerger will entail sharper focus and more efficient capital allocation

- RHF currently high growth average margins business

- Scaling business along with cost focus to improve cost and return ratios

- Return on assets to improve to 1.5 percent versus current 1 percent

KRChoksey on Jain Irrigation Systems

- Initiating Buy with target price of Rs 162; Potential Upside of 64 percent

- MIS opportunity in Maharashtra pegged at Rs 1,500-3,000 crore in next 2 years; Jain has 60 percent market

- Revenue/Net profit to grow at CAGR of 21/72 percent over FY17-19

- Net profit performance is due to lower finance cost post refinancing & conversion of debentures

- Net debt/EBITDA expected to fall to 2.4x by FY19 versus 3.8x in FY17

- Interest coverage to improve to 2.7x by FY19 versus 1.5x in FY17

- Better monsoon and increase Agriculture spending to further boost financial performance

Morgan Stanley on Reliance Industries

- Maintain Overweight with target price of Rs 1,823

- Unfortunate natural disaster hurricane Harvey pushed Singapore GRMs to $10.5 a barrel

- Every 10 percent rise in refining margins has an 8-12 percent impact on RIL's earnings

- RIL is likely to surprise in upcoming earnings season

- Midstream polyester margins to rise 25 percent in FY18 driven by supply cut

- Triggers:- Refining margins reaching highs, chemical margins recovering, clarity on telecom improving

HSBC on Tech Mahindra

- Maintain Buy with target price of Rs 460

- Focused on improving profitability and willing to go of low margin business in the near term

- Recovery in telecom cycle may help TechM outperform overall IT services industry

- Operating earnings are likely to pick up in FY19 after 4-5 years of no growth

- FY18 EPS estimates hiked by 9 percent on significant hedging gains

IDFC on IPCA Labs

- Maintain Neutral with target price of Rs 455

- Limited near-term upside given muted FY18E earnings and uncertainty on FDA resolution timelines

- Revenue/EBITDA/net profit to grow at a CAGR of 12/18/25 percent over FY17-19

- Margins to expand by 130 basis points over FY17-19 to 14.6 percent

- Underutilised fixed cost base could lead to pick-up in revenues from FY19

- Key Risk:- High operating leverage, an inability to achieve projected revenue

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.