‘Housing For All' has been one of the big pitches of the Narendra Modi government. To that end, the government launched the Pradhan Mantri Awas Yojana in 2015, with the aim of building 2 crore houses over a seven year period till 2022. The scheme provided for an upfront subsidy for low cost housing along with a 6.5 percent interest rate subsidy for loans up to Rs 6 lakh.

In his new year's eve address to the nation, Prime Minister Modi extended that to say that under the scheme home loans up to Rs 9 lakh would receive an interest subvention of 4 percent while those up to Rs 12 lakh will be eligible for a 3 percent reduction in applicable interest rates. Both provisions will apply to loans taken in 2017, said the Prime Minister.

The additions could help boost one of the government's flagship schemes, which has so far had a slow start.

According to data provided by the Ministry of Housing and Poverty Alleviation in a written reply to parliament in November, between 2014 and 2016, about 12 lakh houses were covered under the scheme at various stages of implementation. This is just 6 percent of the overall target of two crore houses by 2022.

While the scheme was officially launched in 2015, it subsumed an earlier scheme called the Rajiv Awas Yojana and data for the two has been compiled in the response given to Parliament.

.jpg)

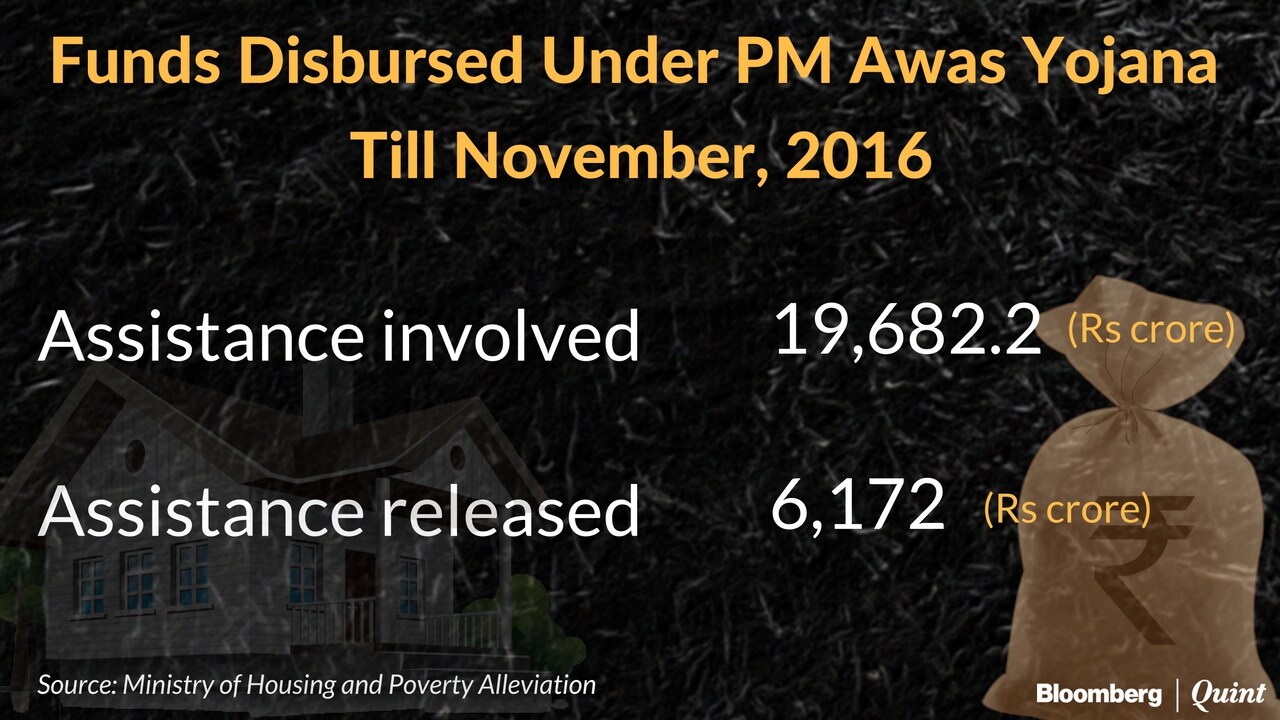

In the written response, the Minister of State For Housing said that central assistance of Rs 6,172.03 crore has been released as on November 10, 2016 across all states.

One reason for the limited activity under the scheme so far could have been the loan limit of Rs 6 lakh, which may be inadequate for meeting the costs involved, according to Gagan Banga, chief executive officer of Indiabulls Housing Finance Ltd.

“Given construction costs at Rs 2,000 - Rs 3,000 per square feet for the most basic house, the loan amounts and other constraining factors in the previous scheme did not result in meaningful transactions,” Banga said in response to a message from BloombergQuint.

Banga added that the prime minister's decision to announce additional slabs under the scheme, which provide interest subvention of three to four percent on loans up to Rs 12 lakh, could help the scheme work better.

In the budget, the government realigned the size of the house for affordable housing and now this increase in the slabs along with a decline in interest rates will ensure that rent amount being paid by people is more than the installment for a home loan of Rs 10-25 lakh and this should result in enhanced demand.Gagan Banga, Chief Executive Officer, Indiabulls Housing Finance

The average ticket size for Smart City Home Loans offered by Indiabulls Housing Finance is Rs 10-15 lakhs, according to Banga, much higher than the earlier cap of Rs 6 lakh for interest subvention on housing loans.

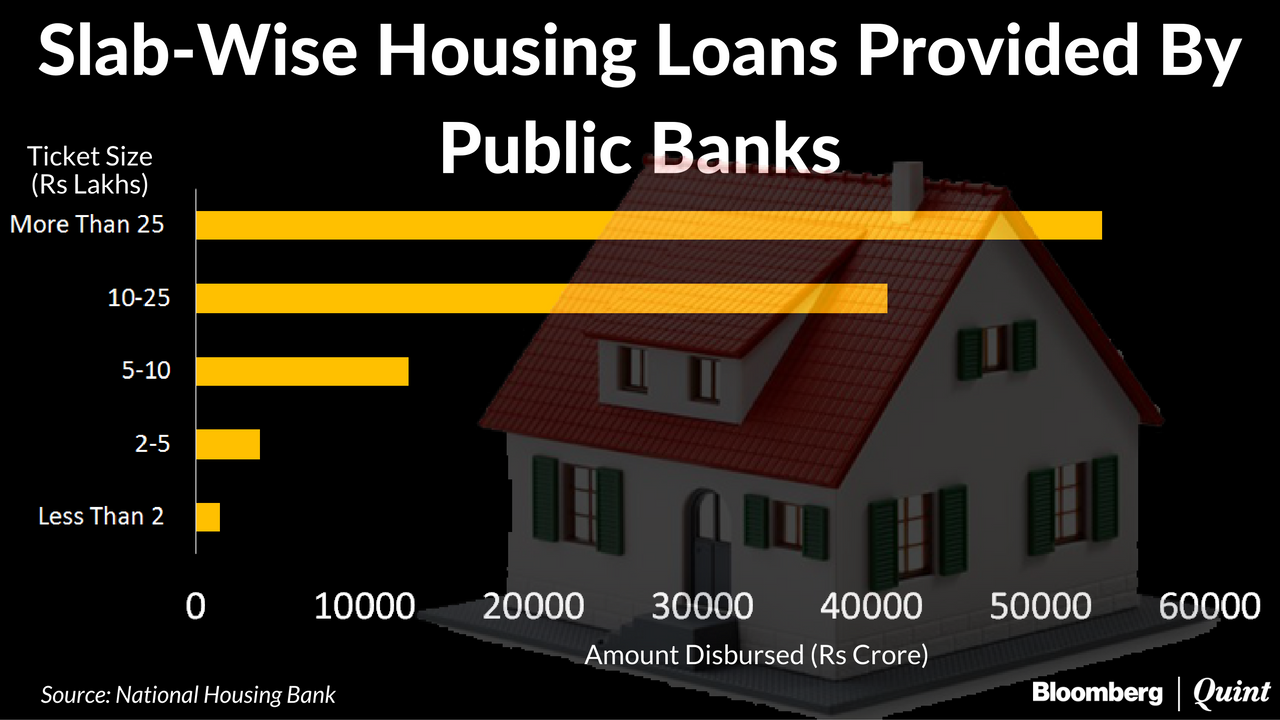

This can also be observed from data provided by the National Housing Board (NHB) in its progress of housing report released last year. In 2014-15, housing loans with a ticket size less than Rs 5 lakh by public sector banks formed a mere 4 percent of the total home lending. Meanwhile, loans between Rs 5-10 lakh constituted more than 11 percent of all home loans disbursed in 2014-15 by public sector banks. More recent data is not available on the NHB's website.

Who Benefits From The Scheme?

The segment most likely to benefit from this scheme is the low cost housing segment in tier 3 and tier 4 towns.

In smaller towns, the cost of land as well as construction is lower compared to high-end cities like Mumbai and Delhi, so the scheme could attract a lot of interest there after the added rebates, Pankaj Joshi, executive director of Urban Design Research Institute said in a conversation with BloombergQuint.

Joshi added that the nature of housing is such that banks look for guarantees in the form of collateral and long leases which aren't present in slums of Mumbai, for instance. Hence, the scheme will find fewer takers in the bigger cities but the impact could be positive in rural towns where land is available in plenty.

“The scheme is unlikely to work in cities like Mumbai where housing is much more expensive than Rs 12 lakh, so loans are unlikely to help the poorer sections but it might just work in smaller towns,” he said.

Will The Scheme Boost Economic Activity?

By pushing people to take loans within 2017, the new provisions could also boost economic activity, should the scheme take off.

In theory, the push to affordable housing could also prove fruitful for the economy as the housing construction sector accounts for 1 percent of the GDP. Moreover, for every one lakh rupees invested in this sector, 2.69 new jobs are created directly and another 1.37 are created indirectly, according to a report published by Ministry of Housing and Poverty Alleviation in 2014.

The report added that with every unit of housing created, household income rises by 0.41 units and by 0.71 units if induced effect is counted for.

“Every additional rupee invested in the housing sector will add Rs 1.54 to the GDP and with household expenditure considered, this is going to add Rs 2.84. For every rupee invested in creation of housing, Rs 0.12 gets collected as indirect taxes,” the report stated.

Whether those gains materialize depends on the eventual response to the scheme.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.