(Bloomberg) -- The late Chinese Premier Li Keqiang built his reputation around trying to make economic growth the Communist Party's number one priority, with the expansion of private businesses and innovation as the main tools for achieving that.

It wasn't a position that always won him support in government, but it did have results.

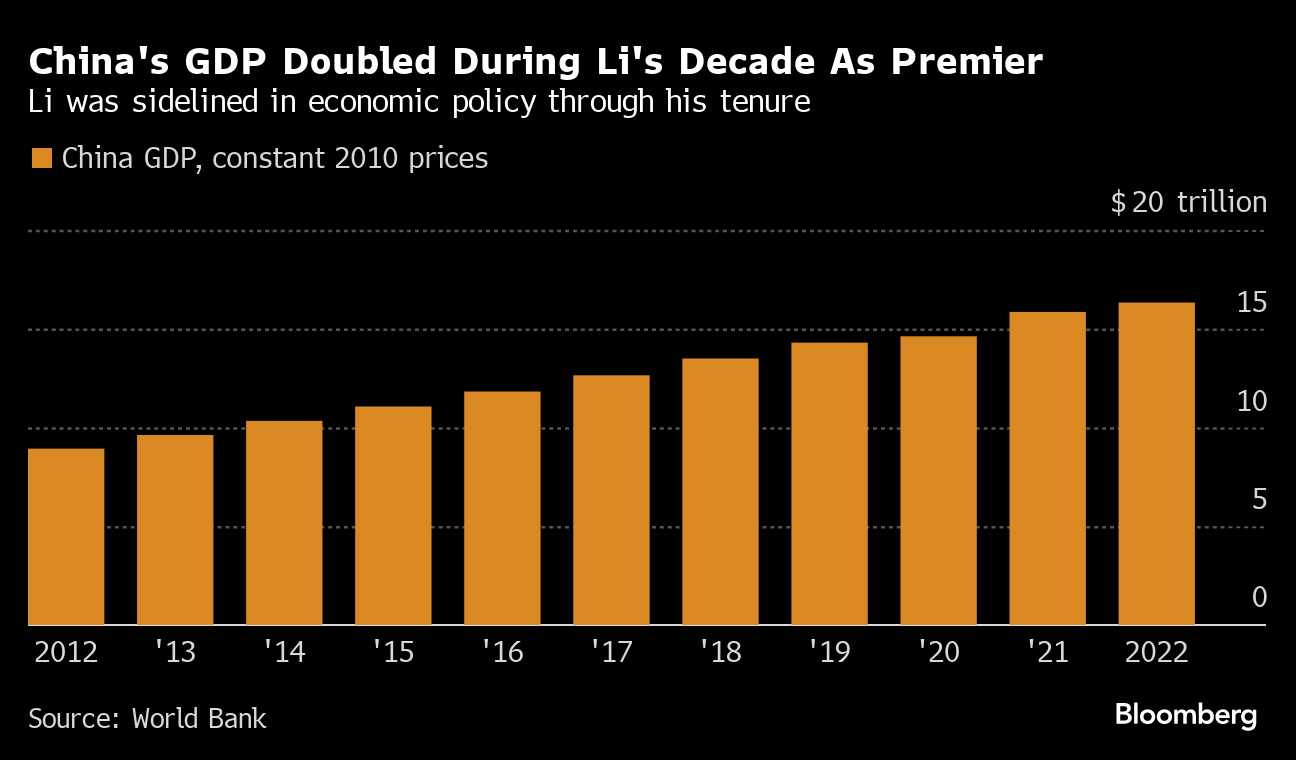

Li's tenure from 2013-2023 saw China's gross domestic product double, narrowing the gap with the US, helping tens of millions escape extreme poverty and winning him a reputation for being responsive to people's needs even as his influence was undercut by President Xi Jinping's tightening grip over the economy.

“Development remains the top priority for China,” Li — who died from a heart attack early Friday at age 68 — said in his last major speech as premier in 2022. In earlier addresses, Li repeatedly described economic development as “the key to solving every problem we face.”

That position marked a contrast with Xi, who despite repeating the development-first slogan in a key speech last year has more often referred to the need to “balance development and security.” Through his tenure, Li saw his influence over critical economic decisions erode as Xi handed greater control over policy to other aides.

Li's focus in his final decade of power was in part a reflection of his position as premier — a role in China that historically has more of an economic emphasis. But economists who interacted with Li said he stood out for his enthusiasm for small private sector businesses and private property rights, alongside a more effective regulatory state.

A protege of former President Hu Jintao, Li was an architect of a 2013 Communist Party statement on economic policy, which called for markets to have a “decisive role” in the economy.

That slogan “really reflects him,” said Bert Hofman, a former country director for China at the World Bank who met with Li, adding that “he was particularly keen on the balance between state and market.”

“Because the external environment changes and China's priorities shifted, so a more state-led, security focused model has emerged. But other key elements — an emphasis on innovation, stronger regulatory bodies — remained,” said Hofman, now head of the East Asia Institute at the National University of Singapore.

Born in central China's Anhui province as the son of a minor party official, Li's doctorate in economics was supervised by Li Yining — one of the architects of China's 1980s reforms, which led to the creation of a wave of small businesses in rural China that helped power growth.

Li Keqiang appeared to carry that spirit into the 2010s, leading a “mass entrepreneurship” campaign that cut red-tape and taxes on businesses, and offered subsidies to college graduates founding companies. The idea was that more start-ups and competition between them would promote innovation, increasingly needed as old growth-drivers waned.

“Li Keqiang was a reform-oriented economist and policymaker who realized that, as China develops, its economic and social policy should evolve,” said Louis Kuijs, chief economist for Asia Pacific at S&P Global Ratings.

China rocketed-up the World Bank's “doing business” rankings and annual new business registrations surged from around 11 million in 2013 to 25 million in 2021. The World Bank later suspended those rankings after a report concluded that China's position was artificially boosted partly due to pressure from Beijing, but there's little doubt the business climate had improved.

Li was also a champion of opening up China's capital markets — making it easier for investors to move money in and out of the country with the aim of increasing competition for funds and spurring efficiency.

“He was seen as an ally of reform-minded technocrats and supported their efforts to open up and introduce market discipline in various parts of the economy,” said Eswar Prasad, the former head of the China division at the International Monetary Fund who is now at Cornell University.

Li's public reputation was bruised by China's stock market crash in 2015 and a botched currency revaluation the same year, which led to massive capital outflows and led China's leaders to slam the door on further capital market opening.

A focus on small businesses creation as the key to innovation has become less favored by China's economists in recent years, amid an increased focus under Xi on state-coordinated industrial policy.

There were “a lot of critiques” of how the mass entrepreneurship policy “misled young people into entrepreneurship that eventually failed,” said Lin Zhang, an associate professor at the University of New Hampshire and author of a book on entrepreneurship in China.

“But the evaluation of him shifted toward a more positive direction in the past few years, especially following the big tech crackdown and the country's leftist turn under Xi,” she added.

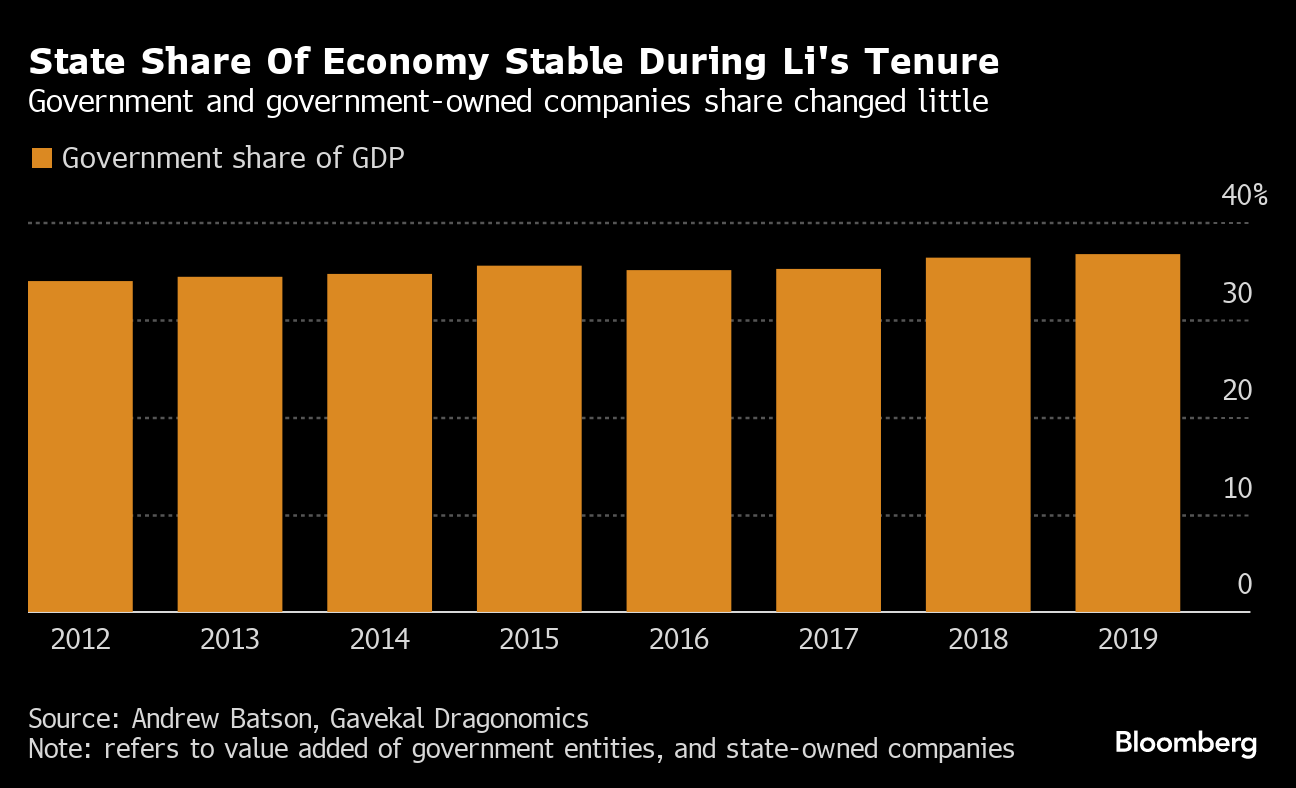

When it comes to the balance between private and public ownership, Li's legacy is mixed.

The share of state-owned companies, when measured by China's economic output, remained constant through Xi's tenure at about 35% of GDP, according to Andrew Batson, director of China research at Gavekal Dragonomics. That was largely due to a rapid expansion of China's financial sector, which is mostly state-owned.

As vice-premier in 2008, Li was instrumental in pushing through a stimulus package that helped China quickly rebound from the effects of the global financial crisis, but also led to a rapid expansion of bank assets and the creation of thousands of state-owned companies to finance infrastructure investment — entities now seen as a threat to financial stability.

Li's signature policy after becoming premier in 2012 was “new style urbanization,” which was meant to focus on growing towns rather than cities. But that policy would eventually be tied to an oversupply of apartments in less-populated areas, contributing to a crisis that China is still navigating through as builders such as Country Garden Holdings Co. and China Evergrande Group struggle.

After Xi came to power in 2012, economic policy making was gradually moved away from the State Council that Li headed and into a number of Communist Party groups where Xi's close aide, Liu He, held sway. That's where the focus shifted more toward reducing financial risks over boosting growth.

Li's economic influence waned more quickly after 2015, and he became increasingly known for his frankness in highlighting the shortcomings of China's economy — pointing out the huge number of people on low incomes during a 2020 speech, for example.

‘Common Touch'

“Premier Li was known for having a common touch,” said Duncan Wrigley, chief China economist at Pantheon Macroeconomics Ltd.

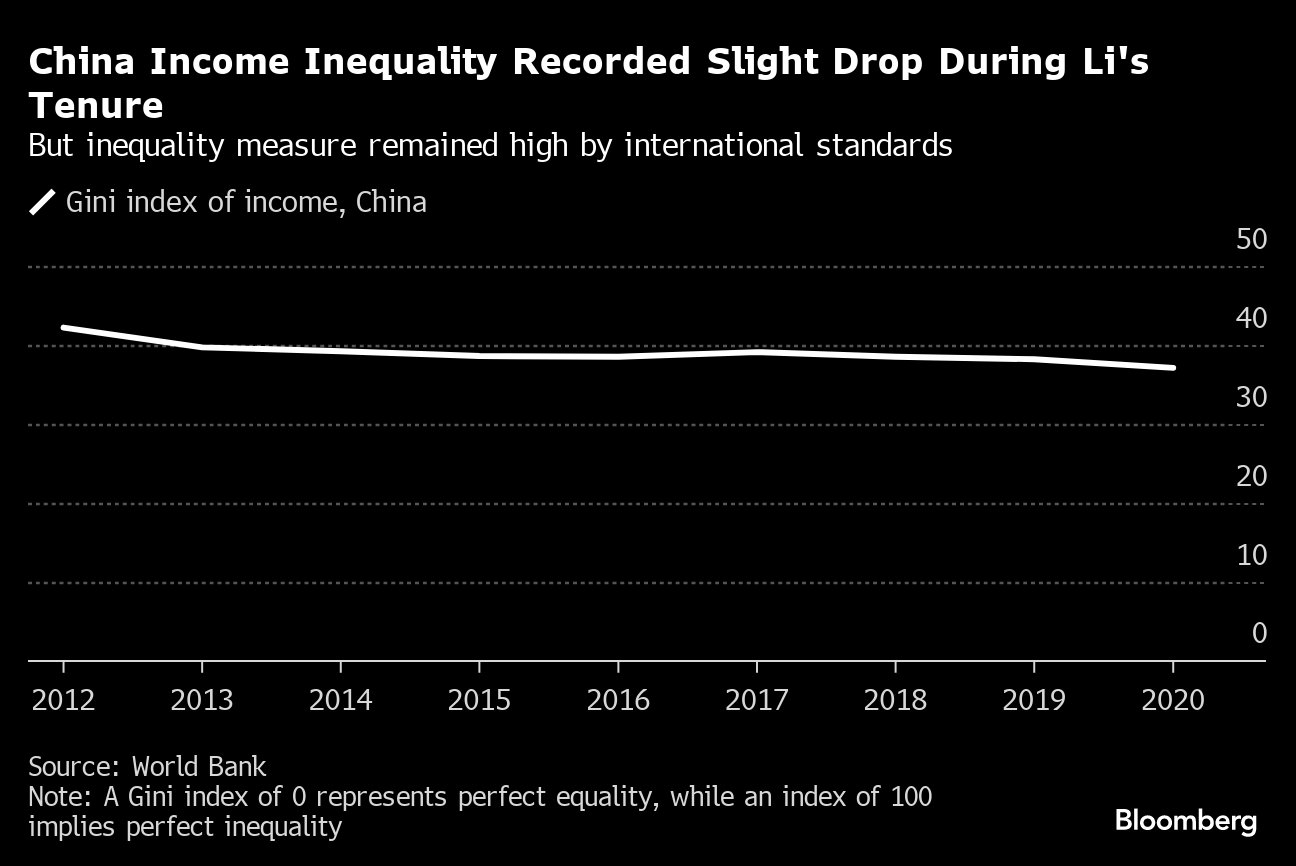

Yet Li's commitment to regular cuts to business taxes, without the creation of a progressive tax system based on income or wealth, arguably made it more difficult for Beijing to roll-out ambitious welfare policies.

Li's posthumous significance to the economy may be as a symbol of what China scholars have called “directional liberalism” — the idea, prevalent since the 1980s, that while policies may shift under the Communist Party, the overall direction is toward looser control over private business. That view has been increasingly questioned in recent years.

In tributes online after his death, a number of economists and economic journalists shared Li's saying that “the Yellow River and Yangtze River won't flow backwards” — a poetic reference to directional liberalism.

“He is a staunch supporter of China's reform and opening up policy,” said Zhang Zhiwei, president and chief economist at Pinpoint Asset Management Ltd. “He died too young. Hope he will rest in peace.”

--With assistance from Fran Wang and Yujing Liu.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.