Small Savings Schemes (SSS), backed by the Government of India, remain a popular choice among retirees in India. This is because risk-free and fixed returns help address cash flow needs as a primary source of income from investments. However, what is crucial is making a prudent choice among a plethora of options, considering liquidity needs, returns, and tax efficiency.

To earn a regular source of income, the Post Office Monthly Income Scheme (POMIS) – offered by India Post -- and the Senior Citizens Savings Scheme (SCSS) are meaningful options. But each of these has its salient features, including distinctions that need to be thoughtfully considered.

So, let's dive into the two small savings schemes and understand them in detail.

POMIS vs SCSS

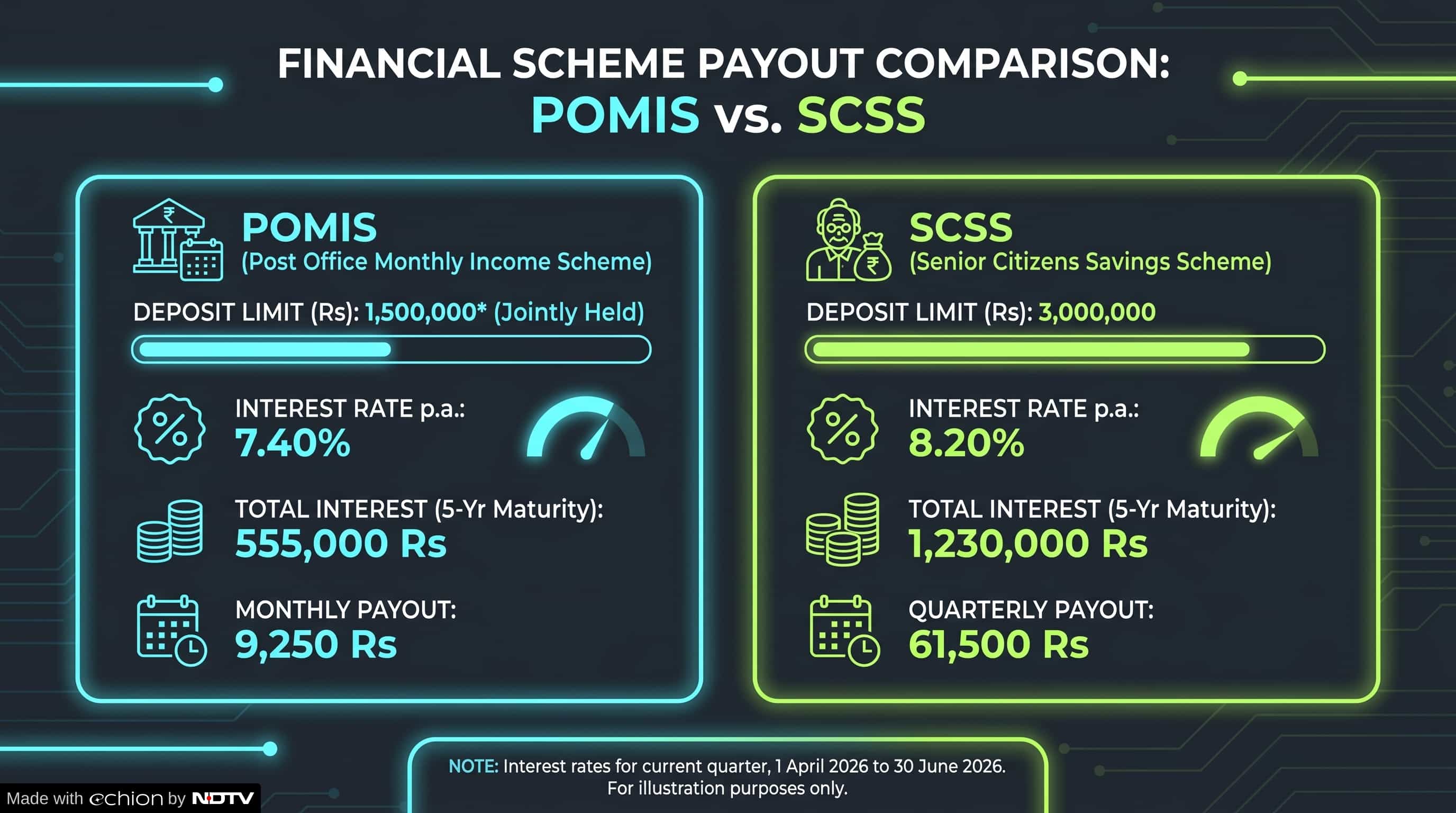

Deposits – A POMIS account can be opened with a minimum deposit of Rs 1,000 (and multiples thereof), with a maximum deposit of Rs 9 lakh for a single account and Rs 15 lakh for joint holdings. Multiple POMIS accounts are also permitted, but the aggregate deposits across all accounts cannot exceed the specified maximum limit.

The SCCS account, on the other hand, can also be opened with a minimum deposit of Rs 1,000 (and multiples thereof), but the maximum limit is Rs 30 lakh in all SCSS accounts opened by an individual. The account is opened in the joint name only with the spouse, but the entire deposit in the joint account is attributed to the first account holder only.

Both POMIS and SCSS accounts can be opened by a resident of India, but the SCSS is specifically for those who have attained the age of 60, or those who are 55 years or more but less than 60 years, and who have retired on superannuation or otherwise on the date of opening an account. Similarly, retired defence personnel (excluding civilian defence employees) can open the SCSS account on attaining 50 years of age, subject to the fulfilment of other specified conditions.

Maturity Tenure and Interest – Both POMIS and SCCSS accounts have a 5-year maturity period. However, the POMIS currently offers interest at 7.4% p.a. (simple interest), whereas the SCSS offers 8.2% p.a. (compounded quarterly). That's a difference of 80 basis points, which may seem small but does impact the returns that can be earned.

The interest payout for POMIS is paid monthly and is credited either directly to the Post Office Savings Account or via ECS to the depositor's bank account.

In the case of SCSS, the interest is compounded annually and paid quarterly – on the first working day of April, July, October, and January – and credited to the depositor's savings account.

The impact: higher interest on SCSS deposits, with annual compounding, enables you to earn more and better meet your cash flow needs.

Say you hold a POMIS account jointly up to a maximum limit of Rs 15 lakh. In this case, at the current interest rate of 7.40%, the maximum annual interest that can be received is 1.11 lakh, which translates to Rs 9,250 per month.

On the other hand, in the case of SCSS, assuming you utilise the maximum limit of Rs 30 lakh available for a single or individual holding, at the current interest rate of 8.2%, the annual interest that can be earned is Rs 2.46 lakh, i.e., Rs 61,500 per quarter or Rs 20,500 per month.

Tax Implications – The interest earned on a POMIS account is not subject to tax deduction at source (TDS). However, the interest earned is fully taxable as income from other sources. Moreover, the investments or deposits made into POMIS do not qualify for deduction under Section 123 (read with Schedule XV) of the new Income Tax Act 2025 (erstwhile Section 80C of the Income Tax Act, 1961).

In the case of SCSS, the deposits you make are eligible for a deduction of up to Rs 1.50 lakh in the financial year under Section 123 (read with Schedule XV) of the new Income Tax Act 2025. If there is taxable pension income and rental income, this deduction can help reduce the tax outgo.

But the interest earned is taxable. If the total interest payout exceeds Rs 1 lakh in a financial year, TDS (at 10% if PAN is provided or 20% if not provided) is applicable unless Form 121 (erstwhile Form 15G/H) is submitted to the post office or bank where the account is held.

So, there is clearly a tax benefit to opting for SCSS over POMIS.

ALSO READ: Invested in PPF? Here's All You Need To Know About Withdrawal Rules And Procedures

Premature Withdrawals – Considering that an emergency can strike at any age and, at times, money may be needed before the 5-year maturity period for whatever reason, liquidity is important. Keep in mind the following in case of premature withdrawals:

In POMIS, premature closure and withdrawal are not allowed before 1 year from the date of account opening.

If the account is closed before 3 years from the date of opening, an amount equal to 2% of the deposit shall be deducted, and the remainder shall be paid. And after 3 years, if the account is closed, an amount equal to 1% of the deposit shall be deducted, and the remainder shall be paid.

As regards SCSS, if the account is closed before 1 year, no interest shall be payable, and any interest paid on the deposit will be recovered from the deposit, and the balance will be paid to the account holder. If the SCSS account is closed after 1 year but before 2 years, an amount equal to 1.5% of the deposit shall be deducted, and the balance shall be paid.

If the account is closed on or after 2 years, an amount equal to 1% of the deposit shall be deducted, and the balance shall be paid. Premature closure or withdrawals from the SCSS account should be carefully considered in the interest of your financial well-being.

To Sum Up

POMIS and SCSS both have their pros and cons, as well as some similarities. While POMIS is a promising option for a monthly interest, retirees need to make a thoughtful allocation. At the current interest rate, POMIS may not be able to beat inflation and is a bit tax-inefficient, with no tax benefit from investing.

SCSS, on the other hand, is a tax benefit under Section 123 on investing. With meaningful deposits and by utilising the maximum limit, at the current higher interest rate, it could generate real returns and cash flows to address retirement expenses.

Retirees could consider SCSS for their core allocation, while POMIS may be considered a secondary bucket to sweep remaining liquidity.

Invest sensibly.

Happy investing!

ALSO READ: What Does 2026 Hold For Your Investments In Gold, Silver ETFs

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.