- LG Electronics India shares rose on CLSA's "Outperform" rating and Rs 1,830 target price

- CLSA sees LG India benefiting from rising appliance penetration and premium product demand

- Large appliances segment expected to grow double digits, driven by premiumisation trends

LG Electronics India Ltd shares are in focus on the back on the positive analyst commentary. CLSA has initiated coverage on LG Electronics India with an “Outperform” rating and a target price of Rs 1,830, arguing that the consumer durable major is well placed to benefit from India's long-term consumption growth story.

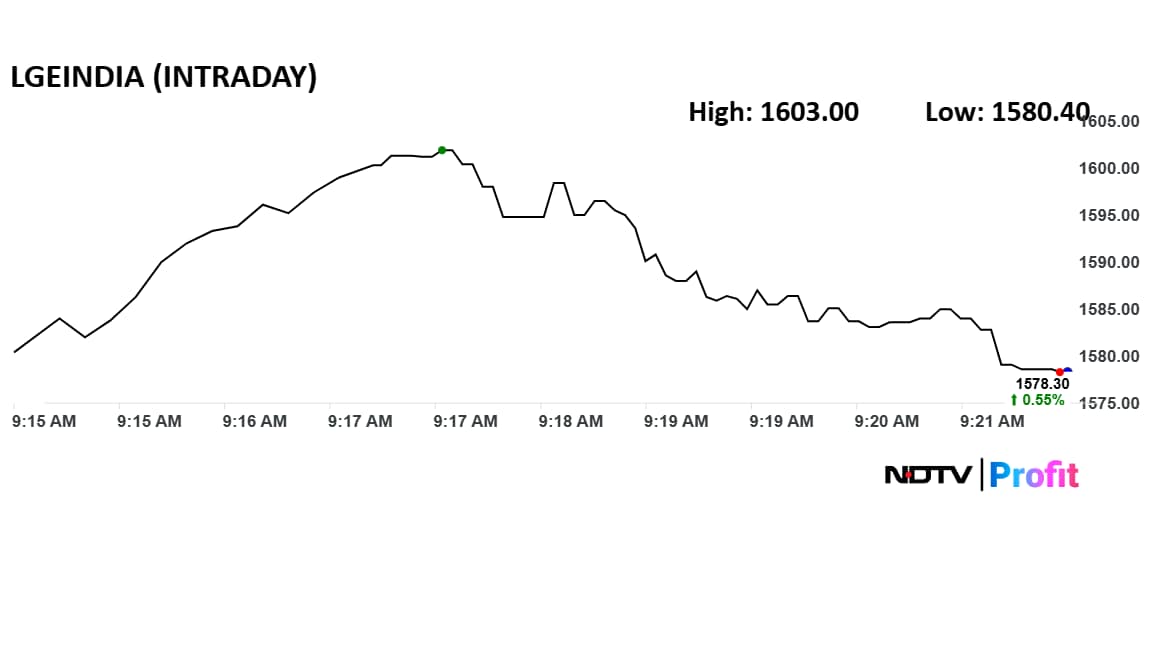

LG India shares had surged as much as 2.13% to a high of Rs 1,603 apiece. Of the 33 analysts tracking the stock, one have a hold call, one have a sell call, and 31 have buy calls.

The brokerage said the company is positioned to be a key beneficiary of India's durable consumption upcycle, supported by increasing appliance penetration and a growing preference for premium products.

Rising incomes, urbanisation and increasing electrification are encouraging first-time purchases of appliances, while existing consumers are increasingly upgrading to higher-end products.

CLSA expects the large appliances segment to deliver double-digit revenue growth over the coming years. Premiumisation is emerging as a key driver, with consumers increasingly opting for feature-rich and energy-efficient products across categories such as air conditioners, refrigerators and washing machines.

The brokerage highlighted LG India's strong brand recall and extensive distribution network as important competitive advantages. It noted that the company's presence across multiple product categories allows it to benefit from cross-selling opportunities and sustain its leadership position in the market.

Another factor supporting the investment case is margin expansion. CLSA expects operating leverage to improve as volumes grow, while increasing backward integration should help the company manage costs more efficiently.

The brokerage also pointed to LG India's local manufacturing capabilities and product innovation pipeline as strengths that could help it capture a larger share of India's growing consumer durables market.

CLSA forecasts revenue and profit after tax CAGR of 13% and 24%, respectively, between FY26 and FY29, outpacing many peers in the sector. It expects growth to be supported by a recovery in industry demand, market share gains, price increases and a gradual pickup in exports.

While remaining positive on the stock, CLSA flagged risks including a slowdown in consumer demand, market share erosion, higher royalty payments and potential contingent liabilities.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.