(Bloomberg) -- The selloff in stocks deepened after weak consumer-spending data fueled worries about a recession, with the S&P 500 suffering its cruelest first half since Richard Nixon's presidency.

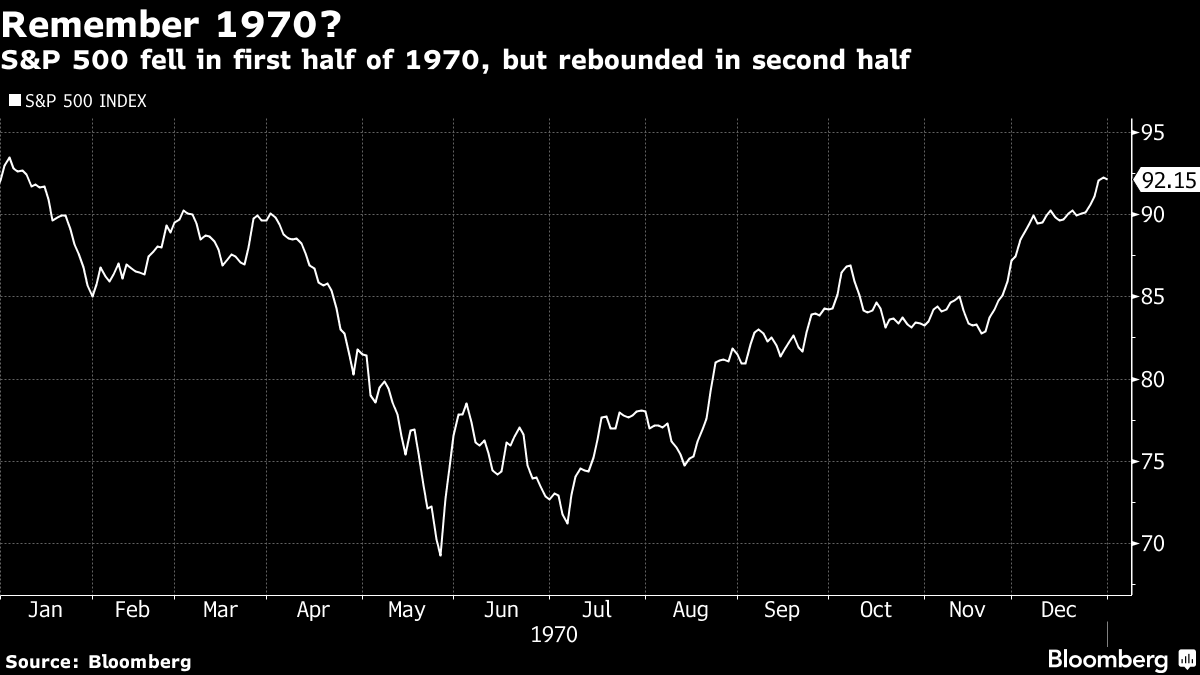

It was a rout for the history books, with the equity gauge down about 21% in the first six months of the year -- the most for such a span since 1970. The superlatives kept piling up across Wall Street. Treasury 10-year yields sank to 3% from a decade-high of 3.5% in mid-June while the dollar had its best quarter since 2016.

Read: Bears Picked Right Stocks to Short With Declines Twice the S&P's

US consumer spending fell for the first time this year, suggesting an economy on somewhat weaker footing than previously thought amid rapid inflation and Federal Reserve hikes. A view that central banks need to act fast because they misjudged inflation has roiled markets, with traders ramping up bets the recovery will buckle under aggressive tightening.

“The stagflation that has gripped our country right now is going to make it tough on the stock market over the intermediate term,” said Matt Maley, chief market strategist at Miller Tabak. “When demand is not the key reason why inflation is a problem, a slower economy is not going to help bring inflation down as much as some experts seem to think.”

Key segments of the world's biggest bond market -- such as the difference between five and 10-year yields -- have inverted, signaling bets that higher rates will hurt the economy. Inversions have generally preceded recessions by about six to 18 months, according to data compiled by Bloomberg.

Read: Economists Sour on US Outlook After Consumer Spending Stumbles

After a rough first half of the year, July will be pivotal for the future direction of markets amid corporate earnings, key inflation data and the Fed meeting, according to Greg Marcus, managing director at UBS Private Wealth Management. He says volatility will probably remain elevated until there's evidence that inflation is moderating, recession risks are receding and geopolitical threats are declining.

Over the past few months, a strategy that had worked well for a decade has been met with fresh lows in the market. Traders have shunned the “buy-the-dip” mantra while embracing the “sell-the-rally” mode. As a result, the S&P 500 entered a bear market for the second time since 2020, having plunged over 20% from its January peak.

But dismal performance is not an indication of what's to come. The US equity benchmark lost 21% in the first half of 1970, during a period of high inflation that the current environment has been compared with. It surged 27% during the last six months of that year.

“We're going to have a double-digit return between now and the end of the year,” Jonathan Golub, head of US equity strategy at Credit Suisse, told Bloomberg Television. “We don't have a profit problem as much as people say.”

Earlier this week, Goldman Sachs Group Inc. strategists noted that US profit margin estimates are way too optimistic, putting stocks at risk of more declines when Wall Street forecasters downgrade their expectations. Morgan Stanley's Lisa Shalett said Monday analysts need a reality check about their earnings projections for this quarter.

Elsewhere, oil suffered its first monthly slide since November as OPEC+ completed the return of output that it halted during the pandemic. Gold dropped for a third straight month. The nearly 60% drawdown in Bitcoin since the end of March was the largest since the third quarter of 2011.

What to watch this week:

- Eurozone CPI, Friday

- US construction spending, ISM Manufacturing, Friday

This week's MLIV Pulse survey looks at the outlook for earnings and stock prices. Click here to participate.

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.9% as of 4 p.m. New York time

- The Nasdaq 100 fell 1.3%

- The Dow Jones Industrial Average fell 0.8%

- The MSCI World index fell 1%

Currencies

- The Bloomberg Dollar Spot Index fell 0.4%

- The euro rose 0.4% to $1.0481

- The British pound rose 0.4% to $1.2173

- The Japanese yen rose 0.6% to 135.74 per dollar

Bonds

- The yield on 10-year Treasuries declined seven basis points to 3.02%

- Germany's 10-year yield declined 18 basis points to 1.34%

- Britain's 10-year yield declined 16 basis points to 2.23%

Commodities

- West Texas Intermediate crude fell 3.6% to $105.82 a barrel

- Gold futures fell 0.6% to $1,807.30 an ounce

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.