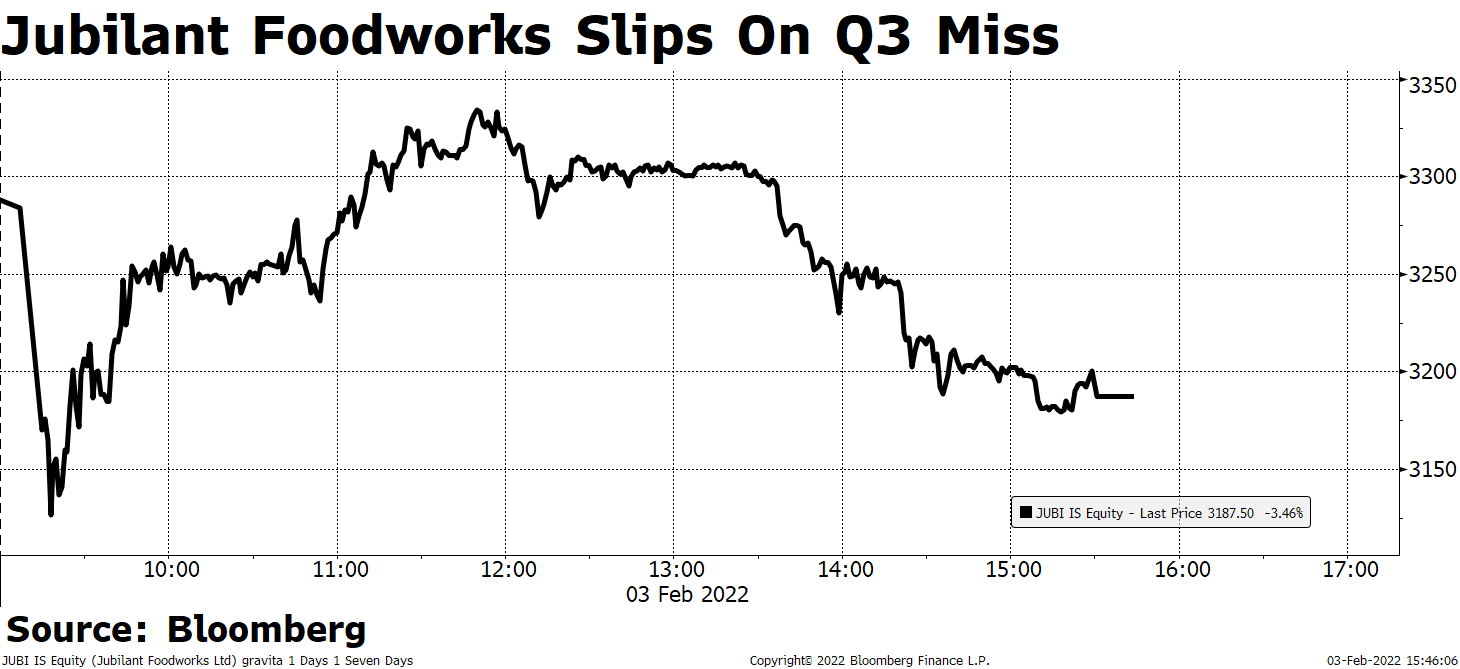

Shares of Jubilant FoodWorks Ltd. dropped as analysts cut price targets for the operator of Domino's Pizza and Dunkin' Donuts in India after its third quarter missed estimates.

Its net income rose 9.6% over the year earlier to Rs 137.33 crore in the three months through December, according to an exchange filing. That compares with the Rs 163-crore consensus estimate of analysts tracked by Bloomberg.

Q3 FY22 Highlights (Standalone, YoY)

Revenue up 13% to 1,193.50 crore, against the estimated Rs 1,270 crore.

Total costs rose 12% to Rs 1,021.31 crore.

Ebitda up 14% to Rs 317 crore, compared with the Rs 325-crore forecast.

Approved splitting each share into five. Record date will be intimated soon.

Analysts, however, remained optimistic on the medium-to-long term prospects of the company as the growth trajectory is likely to see an uptick as restrictions gradually ease.

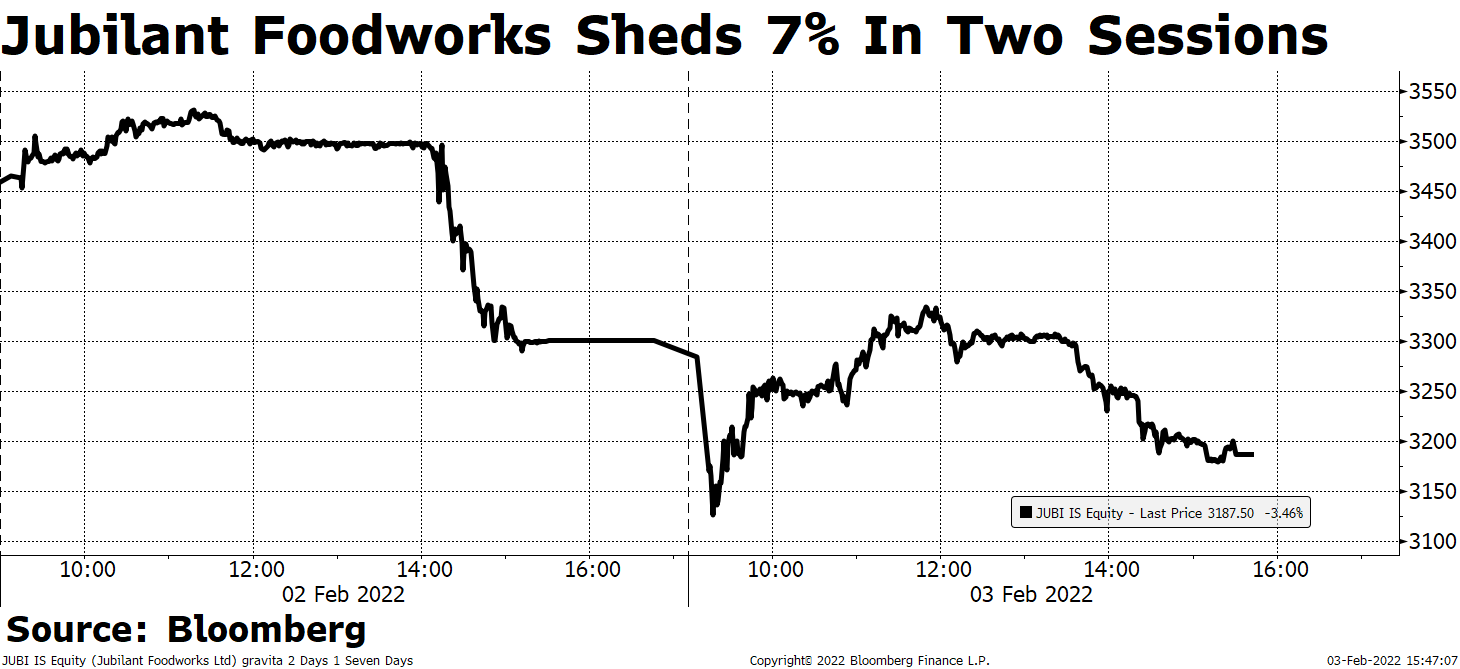

Shares of Jubilant FoodWorks fell nearly 6.5%, the steepest intraday decline in five sessions, to Rs 3,089.65 apiece around noon on Thursday. The stock, however, closed with 3.46% losses. Over the last two sessions, it has shed more than 7%.

Of the 31 analysts tracking the company, 20 rate a ‘buy', seven suggest a ‘hold' and four recommend a ‘sell', according to Bloomberg data. The 12-month consensus price target implies an upside of 21.6%.

The stock's trading volume was nearly five times the 30-day average volume at the time markets closed Thursday.

Here's what analysts have to say about Jubilant FoodWorks' Q3 FY22 results:

Emkay Global

Retains 'hold', cuts target price to Rs 3,600 from Rs 3,900—an implied return of 8.93%.

Revenue growth was driven by a rise in average store count.

Weaker revenue per store was attributed to 5% lower operational hours and cannibalisation impact of new stores overlapping with trade areas of existing stores.

The company expects Popeyes to be a medium-term growth driver.

Ebitda margin improvement driven by pricing hikes taken in the quarter, reduced promotional intensity.

Moderation in delivery/takeaway growth is the facing behind the 8-11% earnings cut.

Motilal Oswal

Maintains 'buy', but reduces target price to Rs 4,200 from Rs 4,575—still an implied return of 27.21%.

The company's decision to stop the same-store-sales growth disclosure is puzzling.

Any further deterioration in disclosures by the company could impact its multiples in future.

Investment case for Jubilant FoodWorks remains strong, driven by quick service restaurants, strong operating metrics, established track record of posting consistent SSSG.

Cuts FY22/FY23/FY24 EPS forecasts by 8%/14%/15% to account for the impact of further Covid restrictions in Q4 and pressure on SSSG and like-for-like growth over the next few quarters.

Edelweiss Securities

Maintains 'buy' but lowers target price to Rs 5,036 from Rs 5,045—an implied return of 51.39%.

Q3 miss is a one-off due to impact of Covid-19 restrictions due to emergence of the Omicron strain.

Growth trajectory is likely to see a strong uptick as restrictions ease.

The company remains well ahead on store guidance and managed to open the highest number of stores this quarter.

Moderation in discretionary spends, aggressive discounting done by other players in QSR and food delivery space remain key risks.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.