The government has stuck to its priority to boost growth over fiscal consolidation. The increase in the capital expenditure spending in the union budget, from Rs 5.5 lakh crore budgeted for FY22 to Rs 7.5 lakh crore for FY23, is substantial.

If the central, the state governments and the public sector companies are able to implement and spend those amounts in a timely and efficient manner, it could lead to a multiplier effect in the economy. This should enable a continued economic recovery and sustain growth over the next 2-3 years.

We had noted earlier that there are several tailwinds to the Indian economy and that we are on the cusp of a sustained economic revival. This increase in government capex spending, across sectors, should be able to revive private capex activity. Supported by export growth, increase in private investment is what drives sustained economic growth. We know from earlier, that a period of investments and growth does lead to broad based corporate earnings growth. This budget is supportive of that trend. This bodes well for Indian equities over the medium term.

The priority towards growth means that the bond markets will see a slower fiscal consolidation and will have to face a very high level of borrowing both from centre and states.

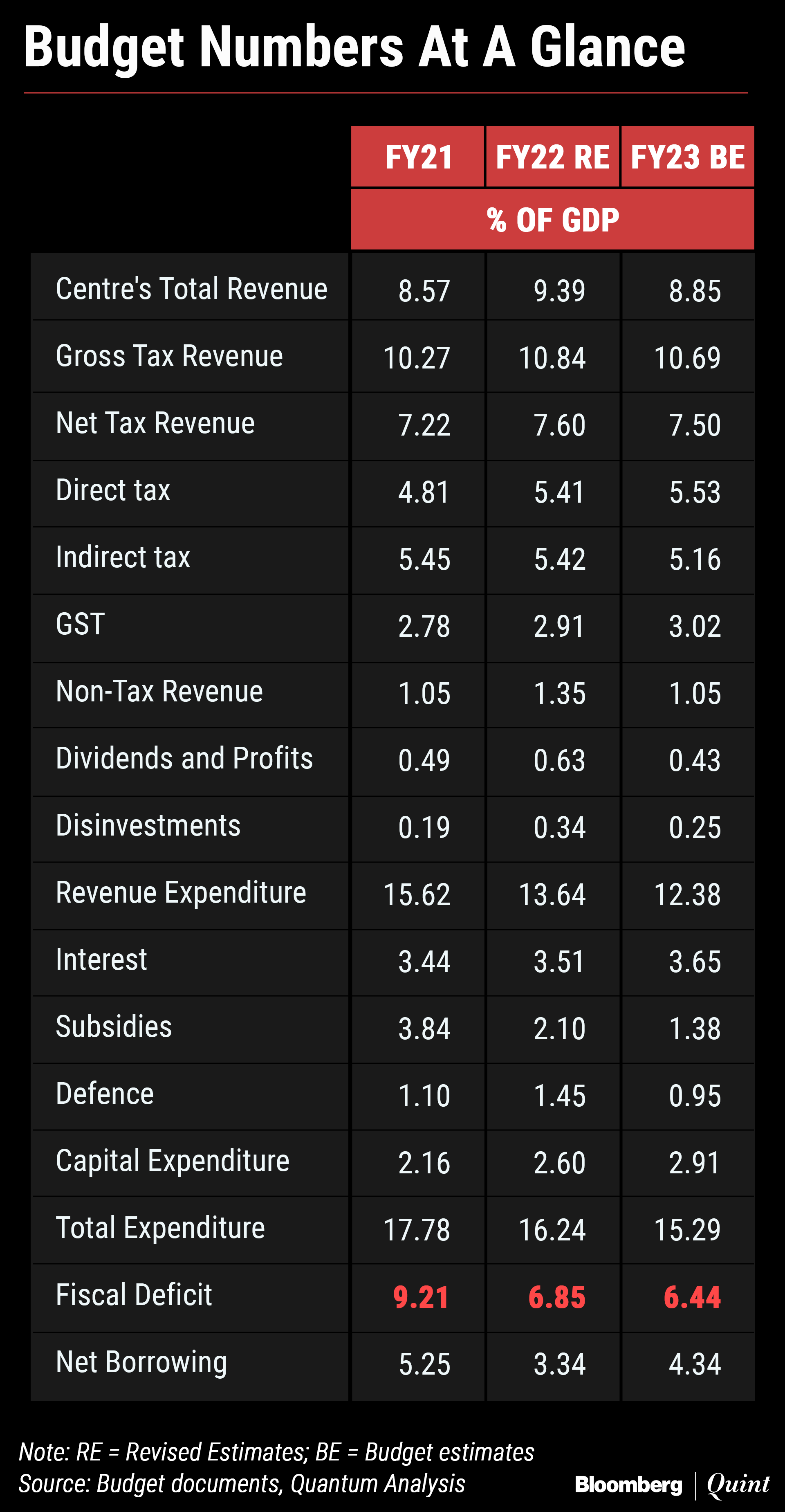

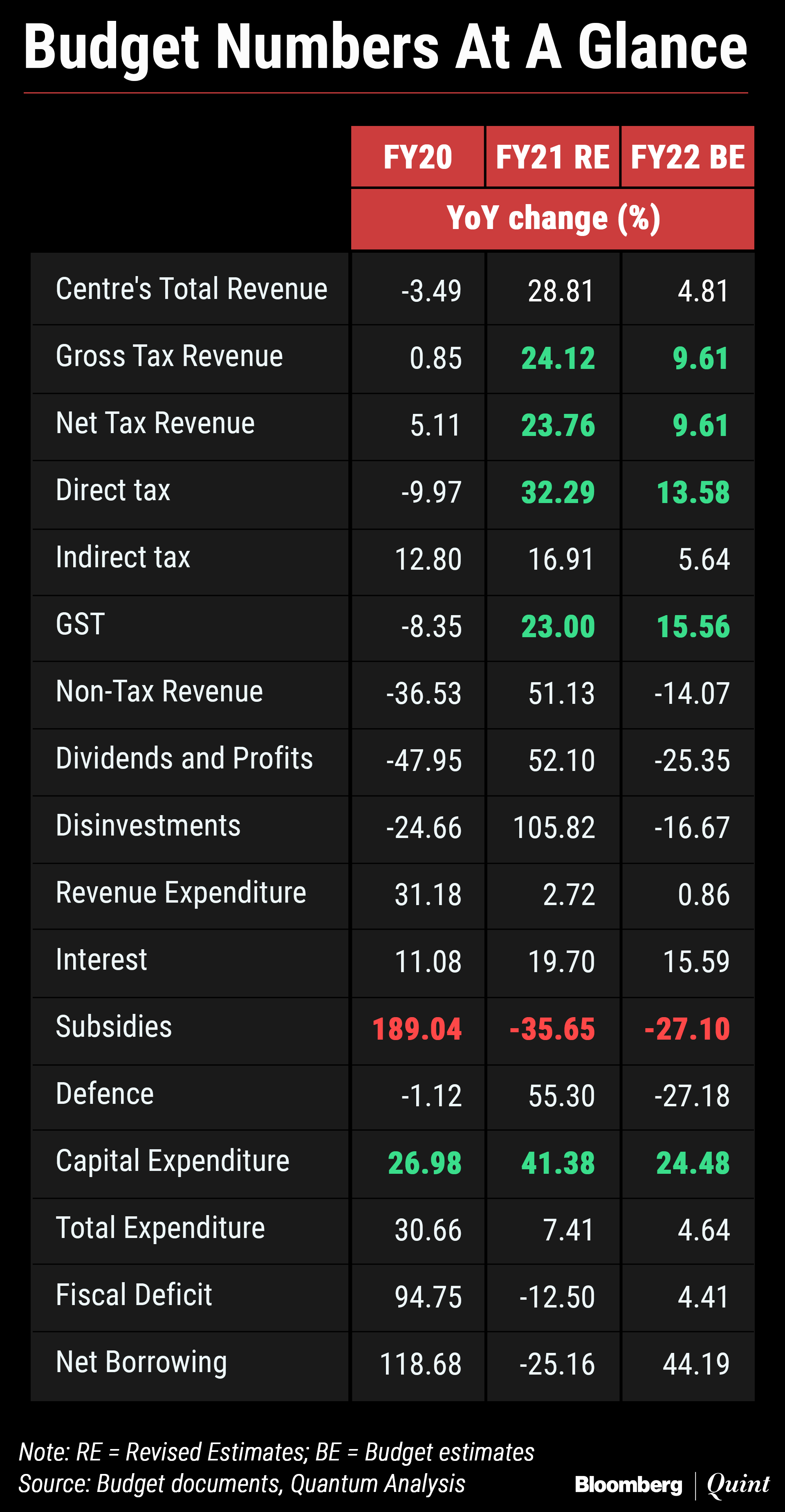

In the 2021 budget announcement, the government announced its intention to prioritise growth and move away from fiscal conservatism. The already slowing economy further crippled by the pandemic forced the government to set out a long path to fiscal consolidation. It committed to bring the fiscal deficit below 4.5% of GDP only by FY26. For FY22 (March 2022), the fiscal deficit is estimated at 6.9% of GDP. In FY23, the fiscal deficit will be cut only by 0.5% to 6.4% of GDP. On a growing nominal GDP, this slow pace of fiscal consolidation provides the government enough spending power.

RBI Should Now Prioritise Inflation

The RBI, thus, no longer needs to take on the mantle of supporting growth. The central bank should prioritise managing inflation over growth and should begin hiking its policy rates. We would expect atleast 100 bps increase in the repo rate from the current level of 4% in FY23.

In this backdrop of higher global oil prices, a hawkish U.S. Federal Reserve and the pressure on the RBI to tighten monetary policy, this higher borrowing will see bond yields rising.

Across the medium to longer tenor of the yield curve, over the course of the year, we will expect bond yields to rise by 20-30 bps for now and maybe by more later in the year. This will be a tough year for medium to longer tenor bonds. It will though be a good year for money markets and short-term fixed income as rate hikes will improve returns.

The lack of any announcement on the global bond index inclusion or any tax changes to facilitate that was also a disappointment. The bond markets clearly need an external demand source to be able to clear the supply without a major spike in yields. The announcement of issuing a Sovereign Green Bond is interesting. If done through an overseas Masala bond (Rupee denominated) structure, we would expect it to receive good demand from the ever growing appetite for green and sustainable instruments from institutional investors.

Would Have Loved To See Some Balance

For us, the major disappointment arising from the budget continued to be the government's focus on boosting supply side over demand. We would have loved to see some balance between boosting industry and supporting individuals.

The budget announcement also had no mention on rural employment, the impact on the informal enterprises and the continued divide between the formal and the informal economy. We do recognise that higher growth will trickle down over time, however there should have been some immediate relief to the economic segments which were impacted by the pandemic.

Think of the sacrifices the Indian consumer has made over the last 2 years. Lost livelihoods, lower incomes, health costs, higher oil and food prices, higher taxes on income and GST outgo. The government's response in terms of some continued income support or a lower tax burden has been missing.

The economy also faces some short term risks from higher global and domestic inflation. In this respect, the government's continued increase in import duties to boost domestic manufacturing in the back of improving growth will lead to a higher cost pressures in the economy. We would have liked to see the government take some measures to manage future cost pressures with duty cuts.

The growing gap between the formal and informal economy, the consumer and the corporate thus seems to be widening. This is bad for consumption, bad for the overall structure of the economy and bad for the prospect of continued recovery under some short term macro headwinds.

Given that the government has allowed the fiscal deficit to remain wide, a portion of that largesse should have been used to support income, livelihood and to lower the cost of living.

The good thing of the overall budget announcement was that there were no major negatives or ‘devil in the details'. The budget numbers also seem credible. The fall in food subsidies is an indication that the government will no longer provide the free food which it had started at the onset of pandemic. The fall in fertiliser subsidy is betting on urea and other prices to not rise.

The revenue numbers, as with the current year, are conservative. Since we expect the growth momentum to sustain, we would expect revenue estimates to be revised upwards. The government's inability to disinvest in a robust stock market period was indeed disappointing. Hopes rest on the IPO of Life Insurance Corporation but nothing major expected as reflected in the lower revisions and estimates.

There were a few other interesting aspects

The desire to relook at urban planning and development laws for the emerging needs of large cities.

The interlinked focus on all modes of transport and logistics infrastructure through the Gati-Shakti programme.

A transfer of Rs 1 lakh crore in an interest free 50-year loan as un-tied funds to states to fund capex and other activities.

The launch of India's digital currency by the central bank.

Arvind Chari is the Chief Investment Officer at Quantum Advisors.

The views expressed here are those of the author, and do not necessarily represent the views of BloombergQuint or its editorial team

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.