(Bloomberg Opinion) -- The bond market is selling off again, but Federal Reserve interest-rate cuts haven't been canceled — perhaps just delayed.

The latest market tantrum came after the Labor Department reported that its core producer price index increased 0.5% in January from a month earlier, exceeding the consensus estimate of 0.1%. In the fed funds futures market, the data brought the expected odds of a May rate cut down to about 1-in-3. In all of 2024, the futures market now expects about three rate reductions, down from the six (and at one point nearly seven) that were implicitly expected in January.

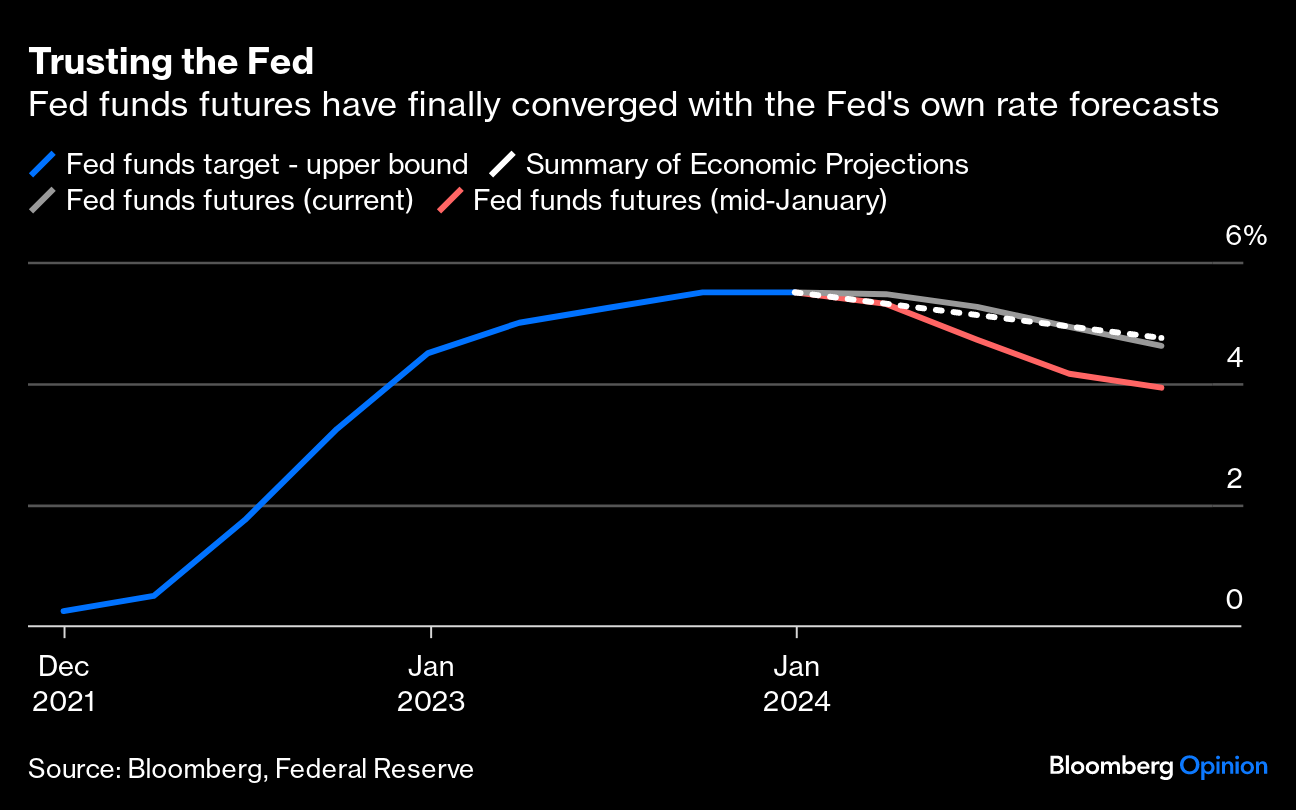

It's worth recalling that policymakers never told us to expect 150 basis points of easing this year. In the December Summary of Economic Projections, the median policymaker projected three moves in 2023, and the most sensible option was to simply take the projections at face value. Now, the market is finally doing just that.

As I wrote in January, month-to-month inflation data is inherently volatile (and sometimes outright fluky). Even in an environment of sustained disinflation, it was inevitable that we would get a few quirky reports from time to time that would force “data-dependent” policymakers to err on the side of caution. That's why I always thought it was crazy to expect the Fed to start cutting rates in March and then — as market pricing implied back in January — cut at almost every meeting thereafter. There were always going to be bumps along the way.

Friday's key example: portfolio management, which added about seven basis points to core PPI.

As Inflation Insights LLC President Omair Sharif wrote before the report, one of the key items that the portfolio management inflation index captures are management fees (calculated as basis points times fund value.) The long and the short of it is that portfolio “inflation” tends to be strong after the US stock market does well. The precise timing of the “inflation” depends on reporting conventions (some funds report monthly and others quarterly), but Sharif correctly projected that we'd see major portfolio inflation on the back of the S&P 500's strong fourth quarter. That doesn't seem like something the Fed should worry about!

The portfolio management head-scratcher comes on the back of Tuesday's higher-than-expected 0.4% month-on-month increase in the core consumer price index, half of which came from a hard-to-explain 18 basis-point contribution from the “owners equivalent rent of primary residence” category. Not only was this inconsistent with the clear cooling in market rents, but it was also extremely out of line with the trend in CPI “rent of primary residence” — a category that's conceptually very similar and has almost always tracked OER. That sure looks like noise, not signal.

What's more, I suspect there's a chance that some of the strength in other categories, including medical care services, may stem from excess seasonality. Government statisticians attempt to adjust for month-to-month seasonal patterns in their data, but doing so has been extremely hard in the volatile post-pandemic economy. It may be that some firms — including hospitals and insurers — may have used the first month of the new year to get in one last round of price hikes to recapture profit margins squeezed by past inflation. A last hurrah, if you will.

Evidently, not everyone agrees. Speaking in an interview on Bloomberg Television's with David Westin, former Treasury Secretary Lawrence Summers said that persistent inflationary pressures mean there are around 15% odds “that the next move [for the Fed] is going to be upwards in rates, not downwards.” Boy do those odds feel high to me!

Certainly, I take Friday's PPI and Tuesday's higher-than-expected consumer price index reports seriously, and I believe that policymakers will too. But Fed Chair Jerome Powell had already effectively taken March rate cuts off the table, leaving the next truly “live meeting” for April 30-May 1. By that time, policymakers will have two more months of data which may well show that January was a fluke.

It's also possible that the “excess seasonality” issue could drag on throughout the first quarter, leaving policymakers with a streak of less-than-great reports and delaying the first cut until, say, July. Even then, there would be plenty of time for policymakers to deliver the three cuts that they always told us to expect. The main problem is: many people didn't want to listen.More From Bloomberg Opinion:

- Inflation Selloff Is Wake-Up Call to Market: Mohamed A. El-Erian

- Stagnating UK Economy Cries Out for Rate Cuts: Marcus Ashworth

- Who's Afraid of a January Price Quirk? Traders: Jonathan Levin

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jonathan Levin is a columnist focused on US markets and economics. Previously, he worked as a Bloomberg journalist in the US, Brazil and Mexico. He is a CFA charterholder.

More stories like this are available on bloomberg.com/opinion

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.