Scan to Download

The National Stock Exchanges Ltd. declared Nov 20 as market holiday on account of Assembly Election of Maharashtra, the bourse said in a release today.

At 3:44 pm, Futures contract of Dow Jones was at 43,880.00, down 0.07%, S&P 500 was at 6,003.25, down 0.01%, and that of Nasdaq was at 21,205.50 down 0.09%.

UK: Bank of England Chief Economist Huw Pill will speak Monetary Policy Report — 5:45 p.m. IST

US: University of Michigan Consumer Sentiment — 8:30 p.m. IST

US: University of Michigan Inflation Expectation — 9:30 p.m. IST

US: Federal Reserve Governor Michelle Bowman will speak at at the University of Mississippi School of Business Banking and Finance Symposium — 9:30 p.m. IST

US: Federal Reserve Bank of St. Louis President Alberto Musalem will deliver pre–recorded opening remarks — 1:00 a.m. IST

Europe: European Central Bank President Christine Lagarde will speak at the Green Swan Conference, in Basel — 09:05 p.m. IST

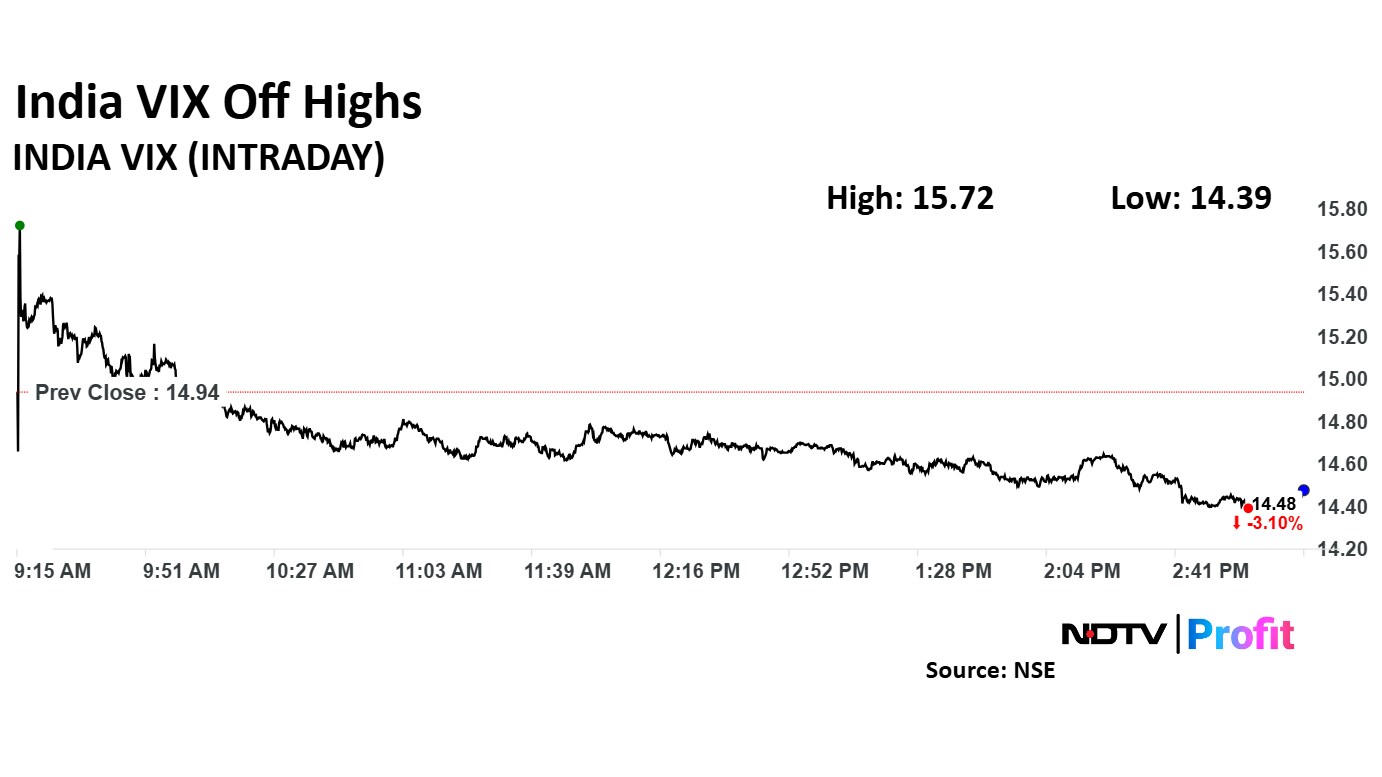

The NSE Nifty 50 and BSE Sensex extended losses to a second session.

On a weekly basis, the benchmark indices erased gains as global events spiked volatility in the Indian markets

ICICI Bank Ltd., Reliance Industries Ltd., and State Bank of India were top draggers.

Infosys Ltd., Mahindra & Mahindra Ltd., and HDFC Bank Ltd. were top contributors to the Nifty 50 index.

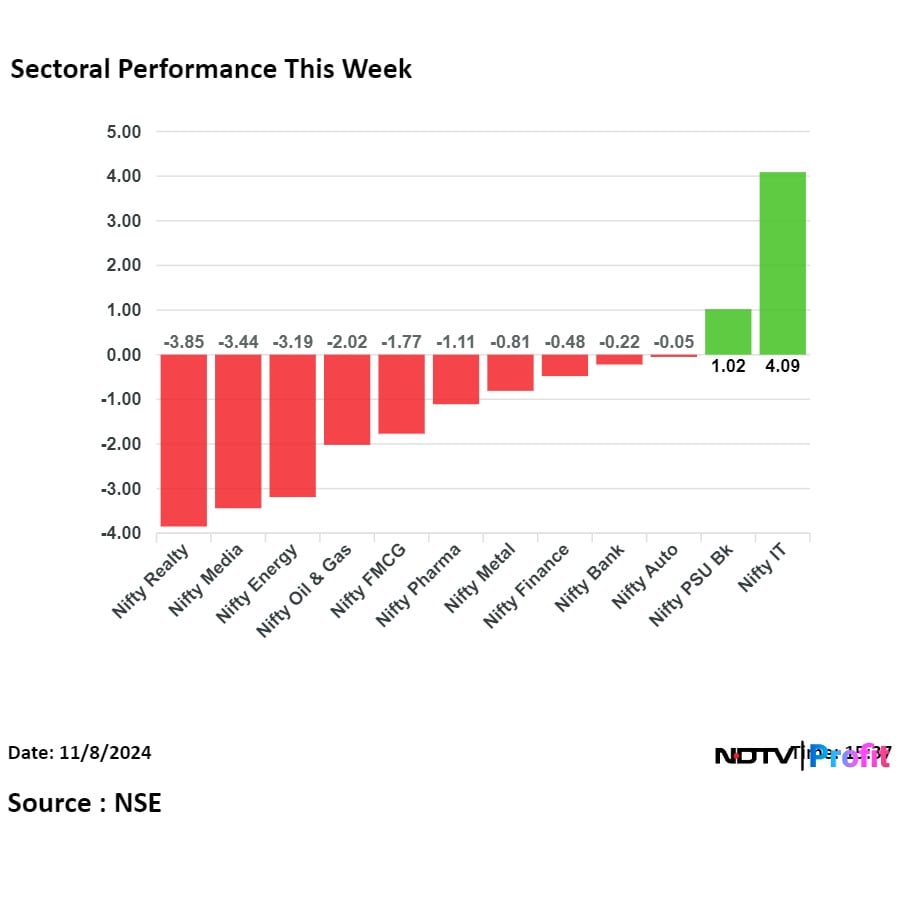

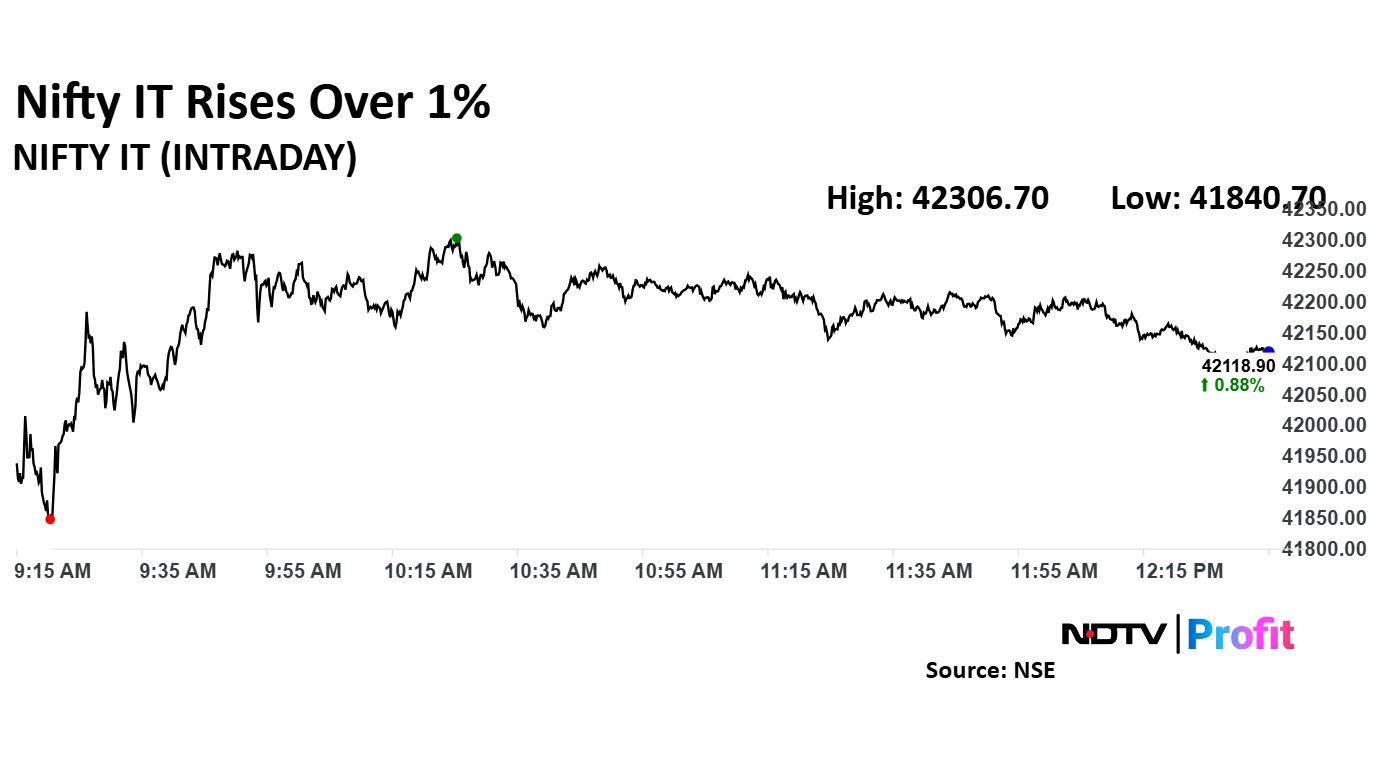

The Nifty Realty was the worst performing sector and The Nifty IT is the top performing sector.

The NSE Nifty Midcap 150 ended 1.48% lower at 20,919.90.

The NSE Nifty Smallcap 250 ended 1.76% down at 17,634.25.

Bharat Electricals Ltd. secured additional orders over Rs 500 crore since Oct 7, it said in an exchange filing.

Aluminium production up 3% at 609 kiloton

Mined metal production up 1.6% at 256 kiloton

Refined metal production up 8% at 262 kiloton

Saleable silver production down 1.7% YoY at 184 million tonne

Vedanta Key Highlights: Cost of Production

Aluminium COP down at $1734/tonne vs $1814/tonne a year ago

Refined Metal COP down at $1071/tonne vs $1137/tonne a year ago

Revenue down 3.4% at Rs 37,634 crore versus Rs 38,945 crore.

Ebitda down 14.4% at Rs 9,828 crore versus Rs 11,479 crore.

Ebitda margin at 26.1% versus 29.5%.

Net profit of Rs 5,603 crore versus a loss of Rs 915 crore.

Other income in Q2 doubles to Rs 1,300 crore.

Revenue up 23.7% at Rs 458 crore versus Rs 370 crore.

Ebitda down 24.5% at Rs 47.9 crore versus Rs 63.5 crore.

Margin at 10.5% versus 17.2%.

Net profit down 25.4% at Rs 29.7 crore versus Rs 39.8 crore.

Net profit up 28% at Rs 18,331 crore versus Rs 14,330 crore (YoY)

Bloomberg estimated net profit at Rs 16,112 crore

Gross NPA at 2.13% versus 2.21% (QoQ).

Net NPA at 0.53% versus 0.57% (QoQ).

NII up 5% at Rs 41,620 crore versus Rs 39,500 crore (YoY).

Ashok Leyland Q2 Results: Profit Jumps 37% On Exceptional Gains, Beats Estimates

Revenue down 18% at Rs 1,032 crore versus Rs 1,264 crore.

Ebitda loss at Rs 163 crore versus Ebitda of Rs 4 crore.

Net loss at Rs 339 crore versus loss of Rs 86 crore.

Mahindra Lifespace Developers Ltd.'s unit approved a joint development agreement with GKW for a 36.9-acre land parcel in Mumbai, the company said in an exchange filing.

Granules India Ltd.'s Unit V receives US Food and Drug Administrations' Establishment Inspection Report report with 'No Action Indicated', it said in an exchange filing.

Premium Plast IPO: Check Latest GMP And Day Three Subscription Status

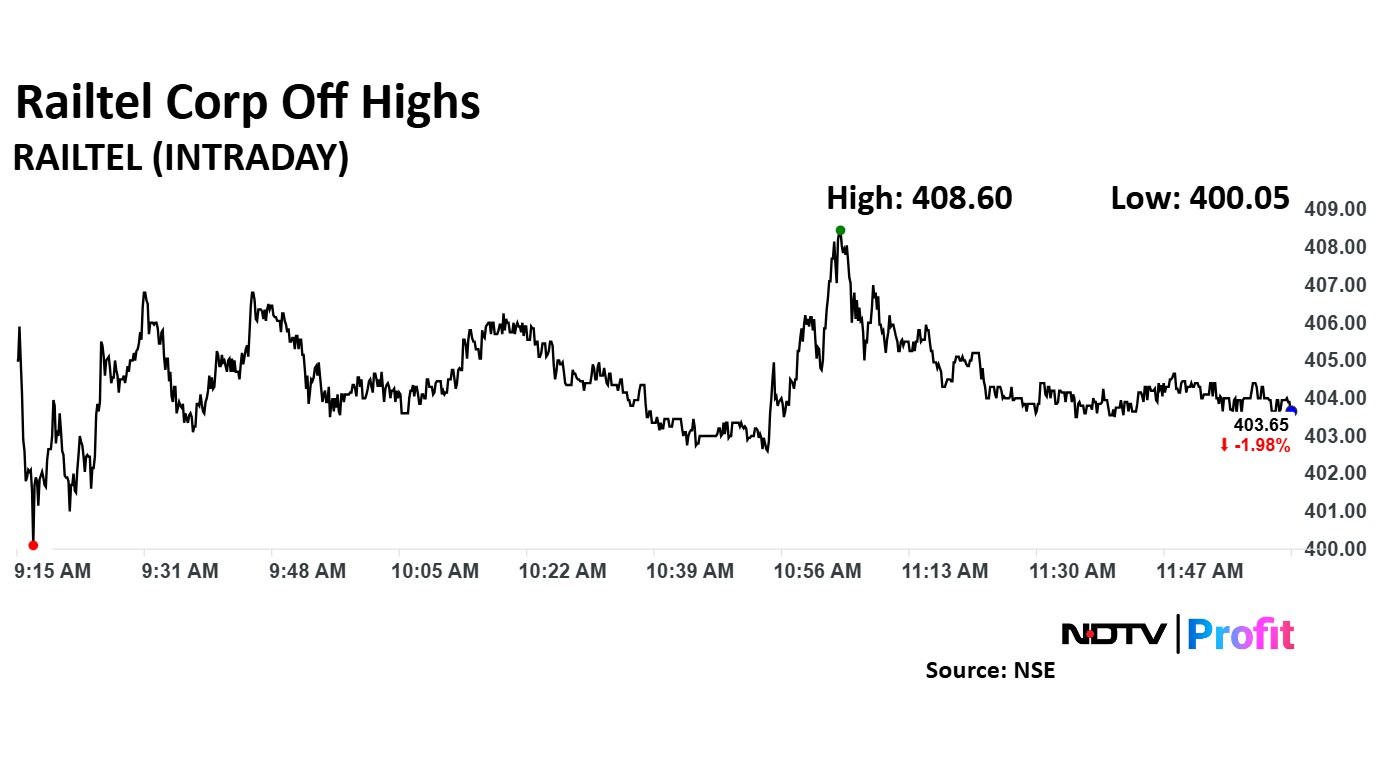

Ircon Share Price Tumbles After Second-Quarter Earnings Slip

Gold Prices In India, Abroad Recover After US Fed Rate Cut

NHPC Share Price Falls Nearly 5% As Profit Declines More Than Estimates

SAIL, NALCO, Tata Steel And Other Mining Stocks Trade Mixed On SC Ruling On Royalty

Market breadth was skewed in favour of sellers. Around 1,794 stocks declined, and 1,092 stocks advanced, and 117 stocks remained unchanged on BSE.

At pre–open, the NSE Nifty 50 was trading 8.35 points or 0.04% higher at 24,207.70, and the BSE Sensex was trading 0.09% higher at 79,611.90.

The yield on the 10-year bond opened flat at 6.81%. It closed at 6.82% on Thursday, according to data on Bloomberg.

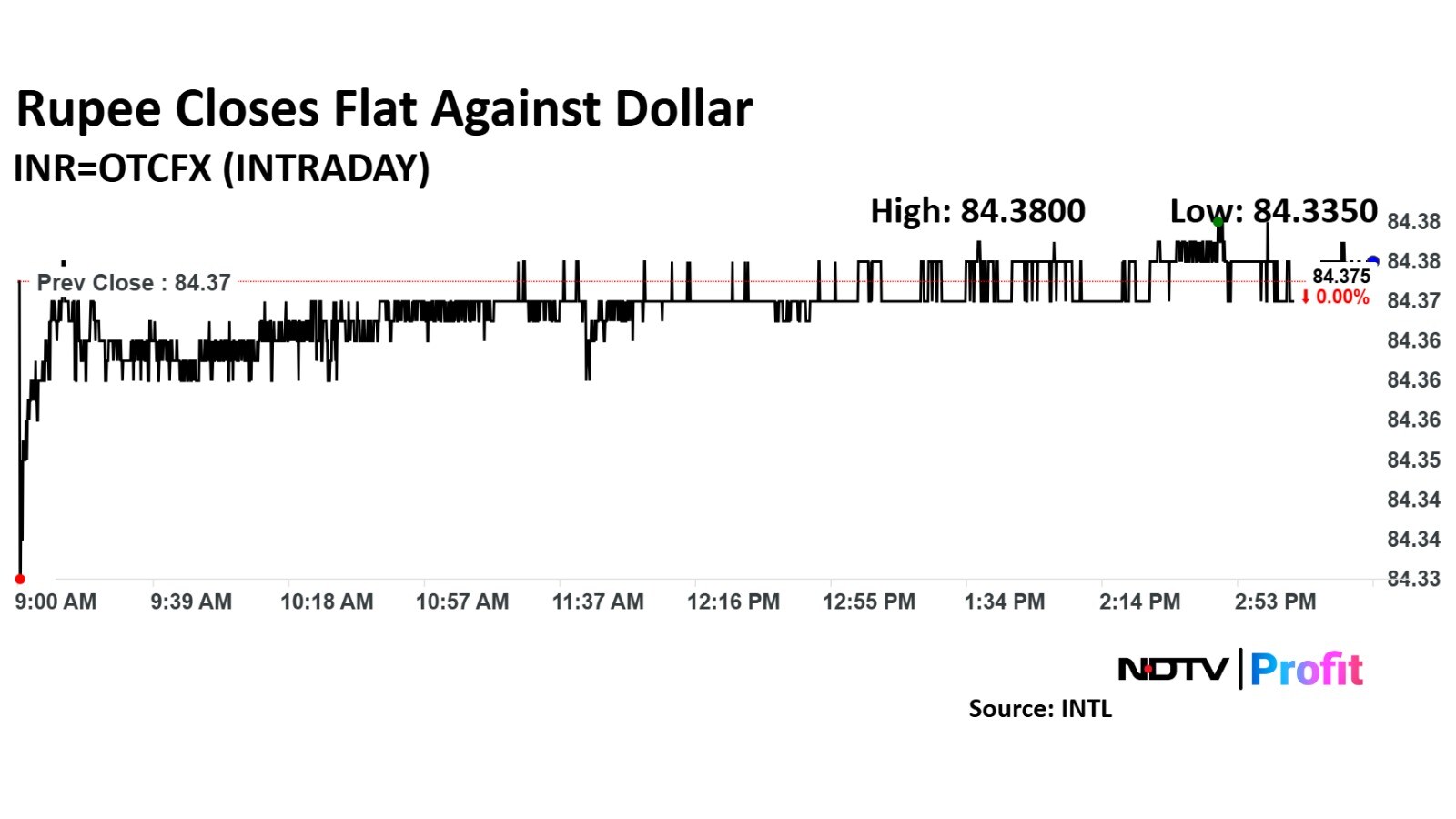

Rupee opened two paise stronger at 84.36 against the US dollar. It closed at 84.38 on Thursday, according to data on Bloomberg.

Most Asian currencies rose against the greenback as the dollar index shed some of the gains in last two sessions after the Federal Open Market Committee cut interest rates in line with market expectations.

The dollar index, which measures the strength of the greenback against six major currencies, fell 0.86% to 104.19 on Thursday following the out come of FOMC. The index was trading 0.03% higher at 104.54 as of 08:38 a.m.

The Philippine peso was the top gainer against the US unit as of 08:36 a.m. It was up 0.54% against the greenback.

The Taiwanese Dollar and Indonesian Rupiah were trading 0.51% and 0.50% higher against the US dollar.

Retain Buy with TP 920,Upside

Recovery in the US business up 57% YoY drives operating performance

Consistent performance in Indian business up 16% YoY

Operating profitability improved by 470bp led by shift in ~45-50% of US manufacturing operations to India

Strong Op leverage with employee expense as % of sales decreasing 570bp YoY to 17%

Expect strong H2 led by growing Indian business and restocking by US customers

Raise our EPS estimates for FY25/FY26 by 36%/10%

Maintained FY25 revenue growth guidance to 16-20%

Oil future prices erased gains in Friday's session. The prices rose on Thursday as the demand outlook improved after the US Federal Reserve cut rates in line with market expectations.

Unwinding of tight monetary conditions in the world's top oil consuming country, raises hope for the demand for the commodity in near term. According to International Energy Agency data, US is the top oil consuming country after China.

The January future contract of the brent crude was trading 0.40% down at $75.33 a barrel as of 7:57 a.m.

Downgrade M&M to Reduce from ADD with TP 2700 vs 3000 earlier, Downside 10%

Though M&M may outperform in near term, expect muted ~4% PV growth in FY25E-27E

Led by persistent industry challenges and best of the SUV launch-cycle is now behind

The second quarter was inline but margin down by 70bps QoQ to 14.3% on lower GM, higher other expenses

The company maintains 15-18% SUV outlook

Slight guidance revision in tractors, now 6-9% YoY growth in Nov-Mar vs 5% earlier

Estimates remain unchanged but lower P/E multiple to 24x Sept FY26

The yield on the benchmark 10–year US Treasury note rebounded in Asian trade session on Friday. It fell sharply Thursday after the US central bank reduced the interest rates.

The yield declined 12 basis points from the four–month high to 4.31%. It ended 10 basis points lower at 4.33% on Thursday.

So far today, the safe–haven asset rose 3 bps to 4.35%. As of 7:42 a.m., it was trading at 4.33%, according to data on Bloomberg.

Maintain Buy rating, with a target price Rs 785, which implied a 15% upside

Expect acceleration of double-digit revenue growth guidance in H2FY25

Hotel segment growth 1.0-1.5% higher on base quarter Cricket World Cup

Better margins on operating leverage and lower losses in international portfolio

Revised revenue estimates by +1.6%/+1.9% for FY25/26

Headline inflation could rise to ~6.3%YY in Oct-24

Vegetable prices could see another month of above trend increase in Oct-24

Edible oil prices might remain elevated

Price momentum in food grains was subdued in Oct-24

The 60-80bps upside risk to RBI December quarter forecast would likely rule out December rate cut

Asian Stocks Echo Wall Street Rally On Fed's Quarter-Point Cut

US Stocks Climb On Powell’s Bullish Economic Signal: Markets Wrap

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.