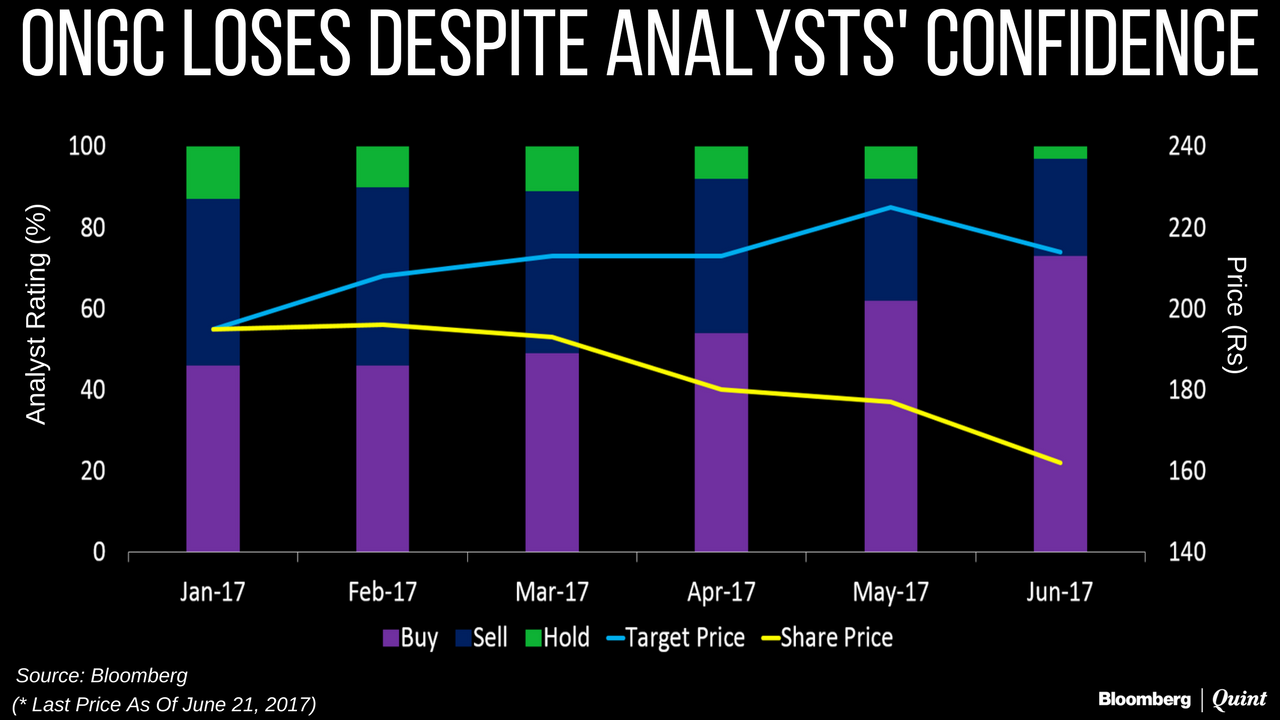

The worst first five months in the last six years and a potential buyout that may increase debt hasn't deterred analysts from maintaining their ‘buy' rating on India's largest explorer Oil and Natural Gas Corporation Ltd.

The gap between ONGC's current share price and the target price set by analysts has widened to more than 30 percent over the last 5 months. Yet, nearly two-thirds of analysts tracking the company continue to recommend a 'buy', according to Bloomberg data.

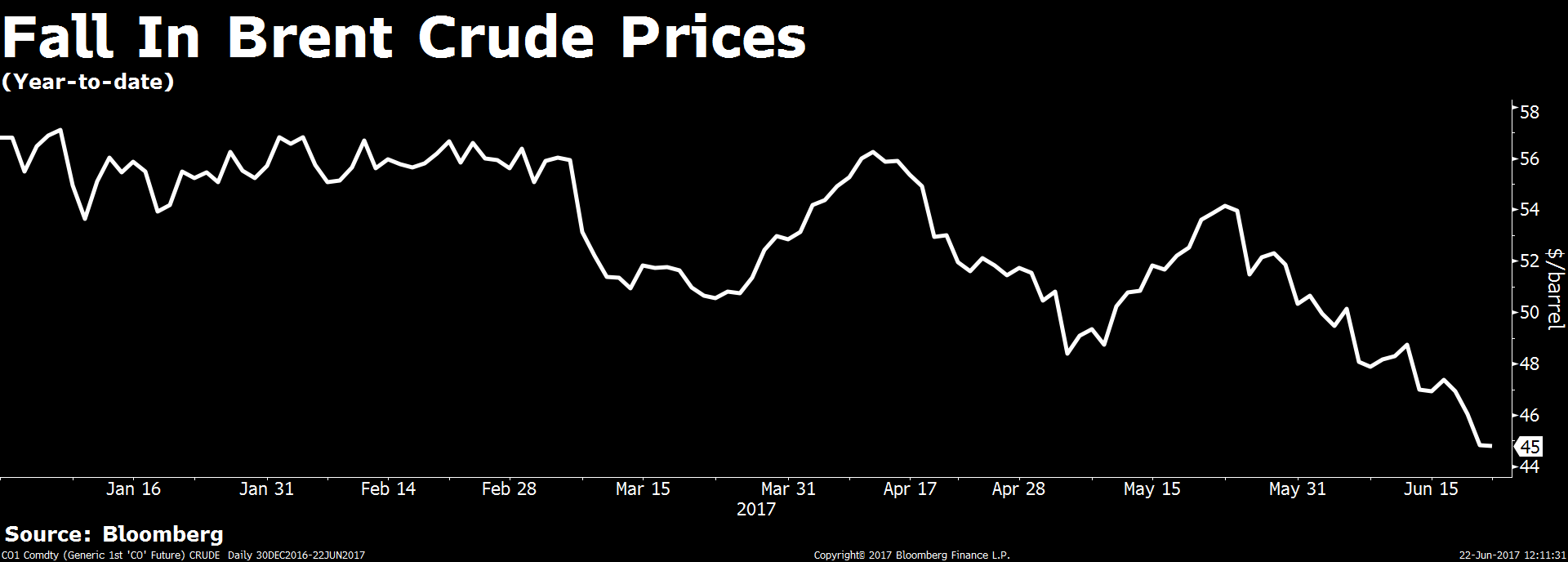

Falling Crude Prices

Nitin Tiwari, an analyst at Antique Stock Broking blames the ONGC stock price decline on the fall in global crude prices. An extension to the planned production cut by the Organization of the Petroleum Exporting Countries has failed to take crude prices higher, as the U.S. continues to ramp up shale gas production. Brent crude prices have fallen 20 percent year-to-date, hurting oil explorers' realisations.

Every $5 per barrel fall in oil prices hurts ONGC's earnings per share by 5-7 percent, said brokerage house Credit Suisse in a report.

Tiwari who has retained a 'buy' rating on the stock in his latest report on May 30, believes that the extension in production cuts will help take prices higher in the long run.

Dipping Margins In Gas Business

The government's new gas pricing rule has led to a drop of more than 50 percent to $2.48 per million British thermal unit. ONGC, which gets a large chunk of its revenue from gas, had earlier said that the government-mandated gas price is significantly lower than the cost of production.

At a media conference to announce the company's last quarterly earnings, Dinesh Saraf, chairman and managing director of ONGC, said natural gas is no more a profitable business.

Natural gas is no more a profitable business, as cost of production is significantly higher than current gas prices.Dinesh Saraf, Chairman and MD, ONGC

Sarraf said the company lost Rs 5,010 crore in revenue in the natural gas business, and about Rs 3,000 crore in profit last year due to lower gas prices.

ONGC-HPCL Buyout

Another overhang on the ONGC stock price is its potential buyout of the government's stake in Hindustan Petroleum Corporation of India Ltd.

The government's plan to create an energy giant by merging state-owned oil companies will increase ONGC's debt burden as the company would have to shell out more than Rs 28,000 crore to buy a 51.11 percent stake.

ONGC had cash worth Rs 16,648 crore, and a total debt of Rs 55,682 crore, as of March 31, 2017.

The transaction will have no impact on operations of HPCL, but ONGC will see a notable increase in debt for purchase of the government's stake.CLSA Reaport - Sector Outlook On Oil And Gas

Morgan Stanley, the only brokerage tracked by Bloomberg to have a ‘sell' rating on the stock cites lack of organic growth in the near future.

Overall consolidated production went up driven by contributions from acquisitions.Morgan Stanley Note - ONGC Q4 Earnings

The brokerage house also mentioned that gas production in India which is expected to grow is less profitable for the company, while the oil business, i.e., the more profitable segment growth is expected to largely remain flat.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.