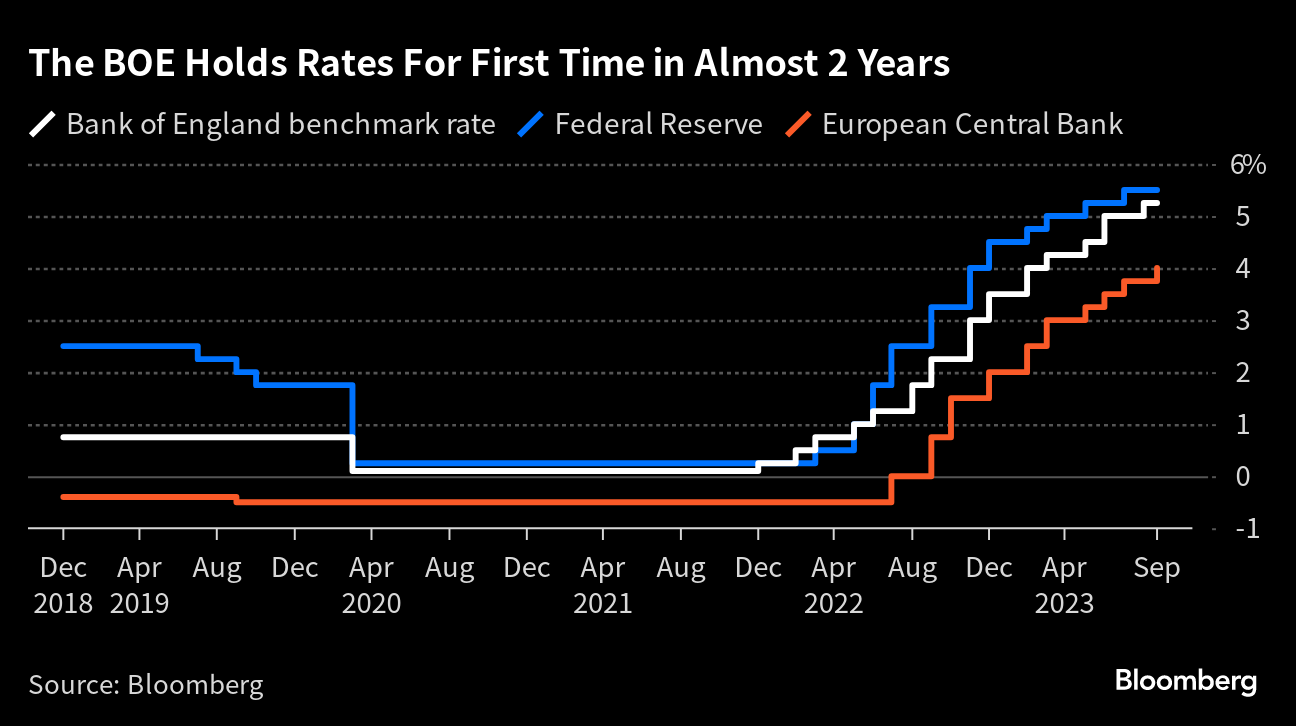

(Bloomberg) -- The Bank of England is likely to hold the line on its “Table Mountain” strategy to keep interest rates at the highest level since 2008 after mounting evidence that the UK economy, labor market and inflation are weakening.

Economists and investors expect the Monetary Policy Committee to leave the benchmark lending rate at 5.25% for the second consecutive meeting, with new forecasts from the BOE thrust into the spotlight instead.

Investors are leaning toward the next move in the key rate being a cut, probably in the second half of next year. Traders will be looking for any hint of an easing in monetary policy ahead in new forecasts that are set to show a rising risk of recession with weaker growth and inflation expected in the near term.

Governor Andrew Bailey has pushed back against speculation over cuts, saying that discussion is premature while inflation remains well above the 2% target. The US Federal Reserve on Wednesday left open the prospect of a further hike despite growing bets the next move there will also be a reduction. The European Central Bank also put its hiking cycle on pause last week with President Christine Lagarde calling any speculation over a rates reduction “totally premature.”

For Prime Minister Rishi Sunak, high rates to tackle stubborn inflation are a headache ahead of an election expected next year after he pledged to boost the economy and cut price rises in half this year. The BOE's decision is due at 12 p.m. London time, with a press conference led by Bailey following a half hour later. Here's what to watch:

Decision and guidance

There's been little in the data since September's meeting that could shift views on the MPC. Chief Economist Huw Pill, speaking in Cape Town at the end of the summer, described a “Table Mountain” path for rates in its guidance in reference to the landmark looming over the city. That's a heavy hint that rates will remain elevated for a prolonged period.

The MPC could repeat much of September's guidance, noting that policy will stay “sufficiently restrictive for sufficiently long” to get inflation back under control.

What Bloomberg Economics Says ...

“The lack of alarmingly hot data releases since the Bank of England last met in September, points to rates staying on hold for a second straight meeting. The decision will likely be accompanied by a warning from the central bank that tightening will recommence if progress in its inflation fight either stalls or goes into reverse.”

—Dan Hanson and Ana Andrade, Bloomberg Economics. Click for the PREVIEW.

Should the BOE project that inflation will fall below its 2% target in the coming years, investors may make more bets on a rate cut. That could spark a rally in gilts and also dent the appeal of the pound.

Martin Weale, a former ratesetter and now professor of economics at King's College London, said he remained concerned about wage growth and that “there are still material risks” of an inflation overshoot.

Guidance After September Decision

“Monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.”

—Bank of England minutes of Monetary Policy Committee meeting on Sept. 20.

Vote Split

The meeting is likely to once again expose divides at the BOE's nine-member rate-setting panel. The MPC voted 5-4 for no change in September.

Since the meeting, the MPC has lost one of the hawkish dissenters with the departure of Deputy Governor Jon Cunliffe, who has been replaced by internal pick Sarah Breeden. She is seen as likely to vote with Bailey and the other internal policy makers on her first outing on the MPC. She also previously signaled her concerns over the potential impact of hikes on financial stability.

Forecasts

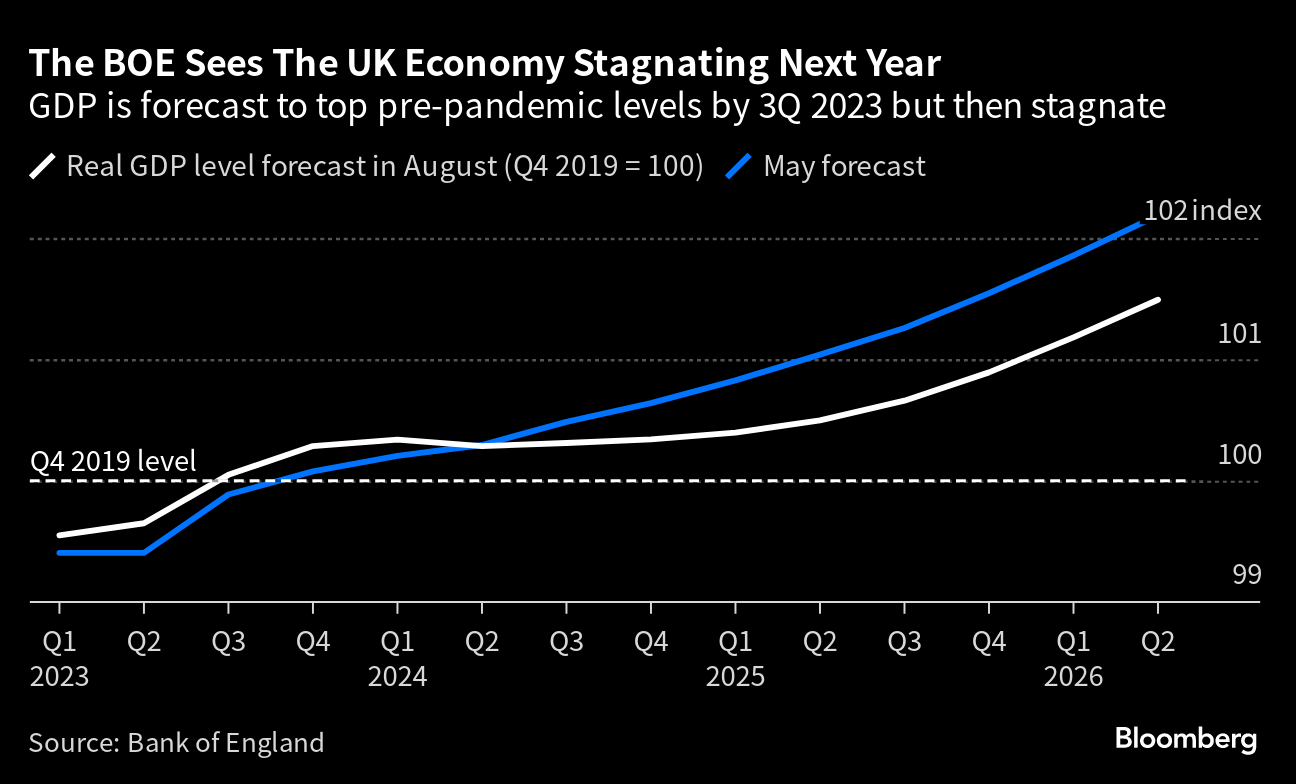

The BOE's latest forecasts are likely to warn of a darkening near-term outlook, with many City of London economists braced for a recession.

Rising unemployment and the drag of higher interest rates are likely to depress the economy. In September, the BOE warned it now expects third quarter growth to be 0.1%, down from the 0.4% expansion projected in August. Recent surveys suggest the weakness also spilled over into the final quarter of the year.

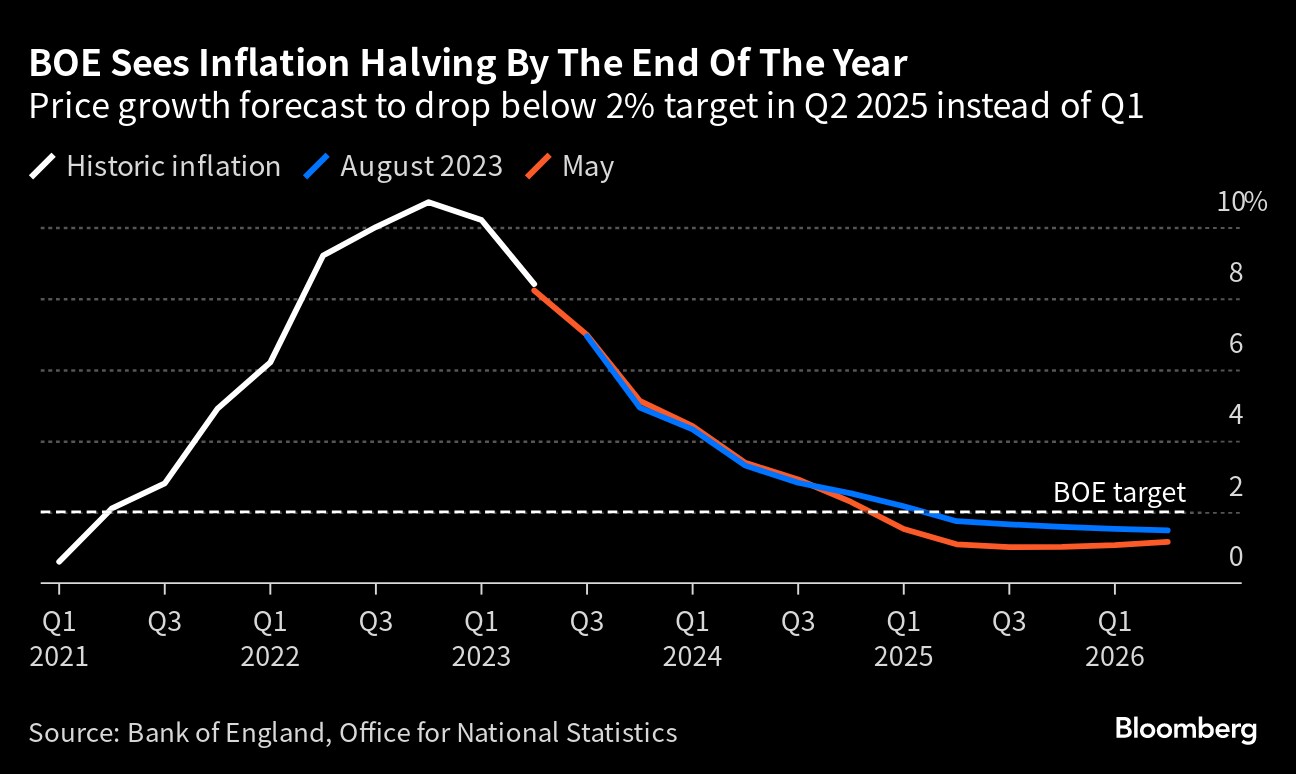

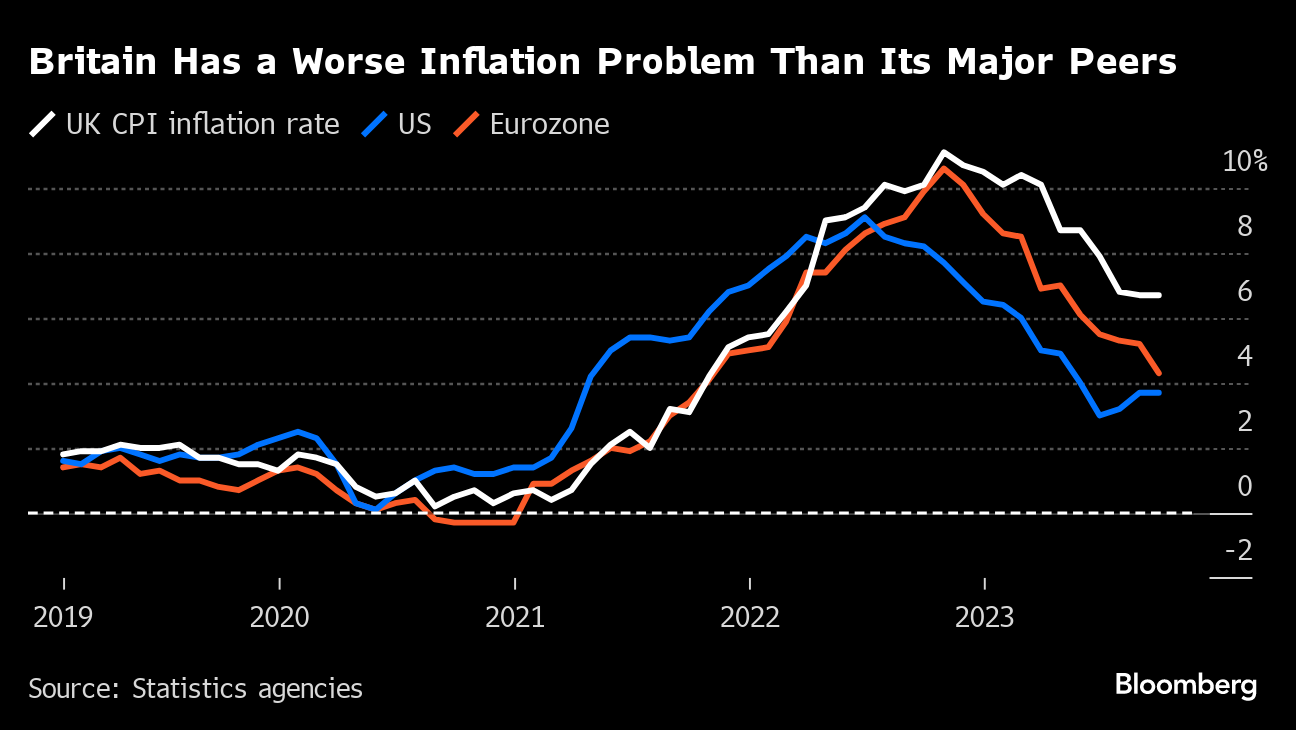

There may be better news on inflation. UK consumer prices rose 6.7% in September, slightly lower than the 6.9% the BOE expected in August. Citigroup sees the figure dropping to 4.7% when October's figures are released on Nov. 15.

“We expect the BOE to cut near-term growth and inflation forecasts, mirroring the weaker data flow,” said Robert Wood, UK economist at Bank of America. “We expect the Bank to raise growth and inflation forecasts at the two- and three-year horizons, reflecting lower interest rates and lower sterling.”

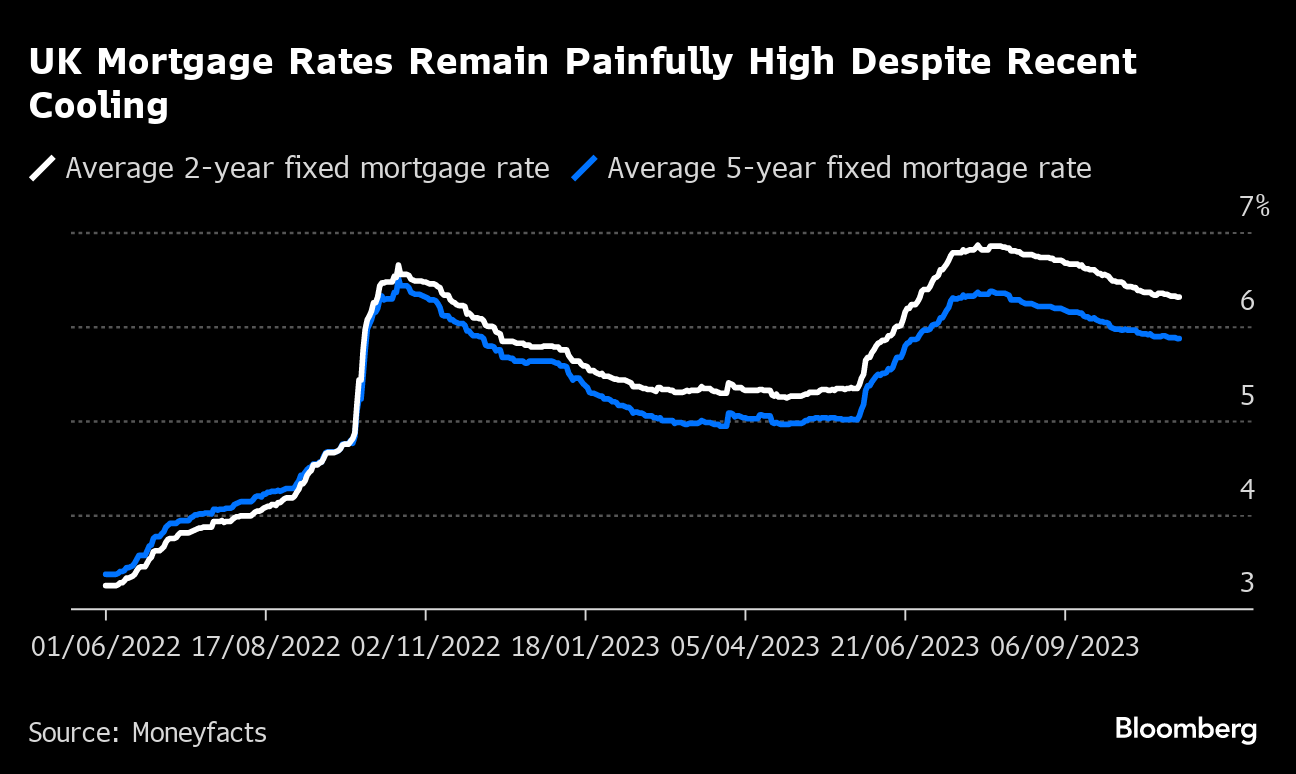

Mortgage Rates

Mortgage rates have eased since surging in the summer but remain stubbornly high, putting a dampener on activity in the housing market.

Even with the BOE halting its rate rises in September, the recent unwinding has only put a small dent in the rise in borrowing costs for homeowners after the most aggressive rate hiking cycle in generations. The average two-year fixed mortgage rate is still well above 6%, a near tripling since the start of 2022, Moneyfacts data shows.

The rise in Bank rate since the end of 2021 from 0.1% to 5.25% has added an average of £540 to monthly repayments for those on tracker mortgages, according to UK Finance.

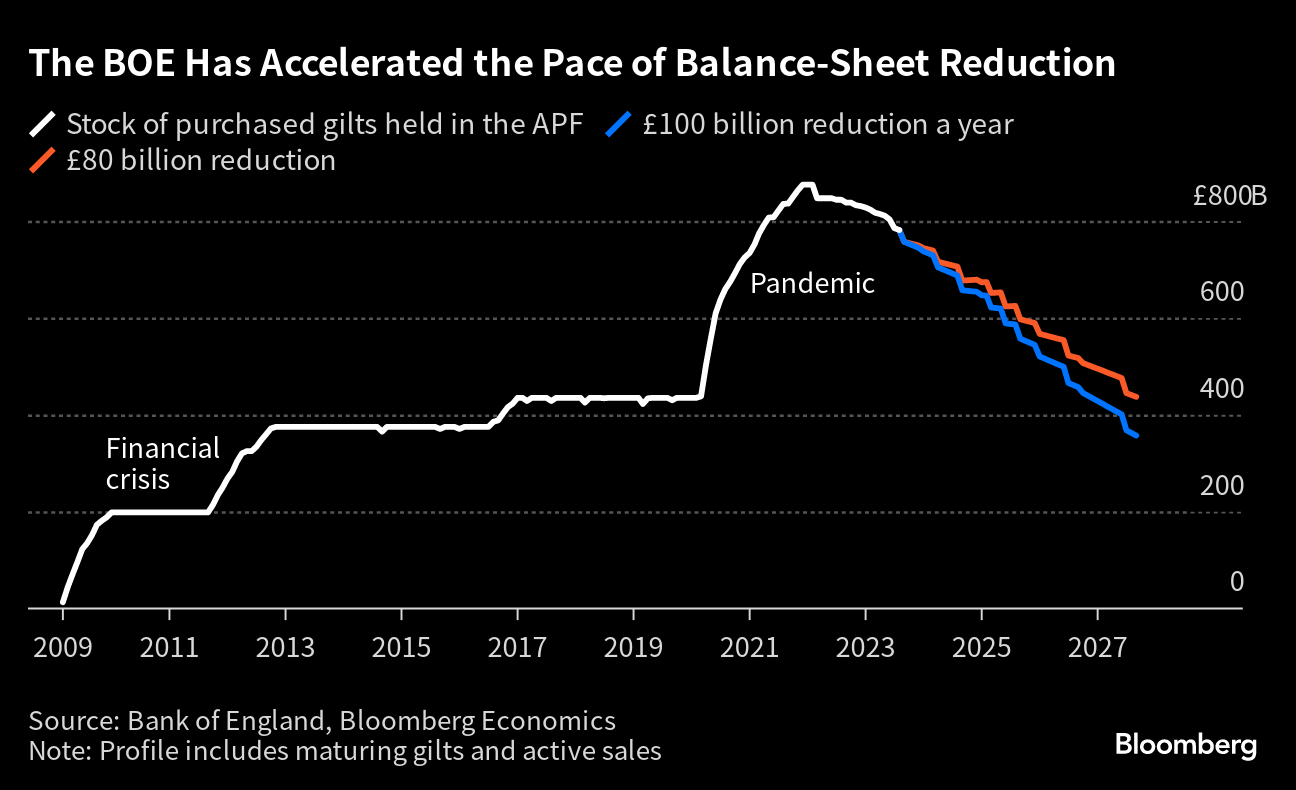

Quantitative Tightening

The BOE stepped up the pace it is unwinding its balance sheet of bonds after starting the second year of its quantitative tightening program in October.

It announced in September that it will run off £100 billion ($121 billion) of bonds in the second year through sales and allowing debt to mature, up from £80 billion in the first year.

The BOE judges that the unwinding of the vast bond purchases after the financial crisis and pandemic has had little impact on the economy and bond yields. However, there are concerns over QT's impact amid bouts of volatility on global bond markets in recent months with UK borrowing costs close to their highest level since 2008.

--With assistance from Greg Ritchie, Zoe Schneeweiss and Philip Aldrick.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.