(Bloomberg) -- The US service sector expanded in October at the weakest pace in five months as business activity softened and employers scaled back hiring.

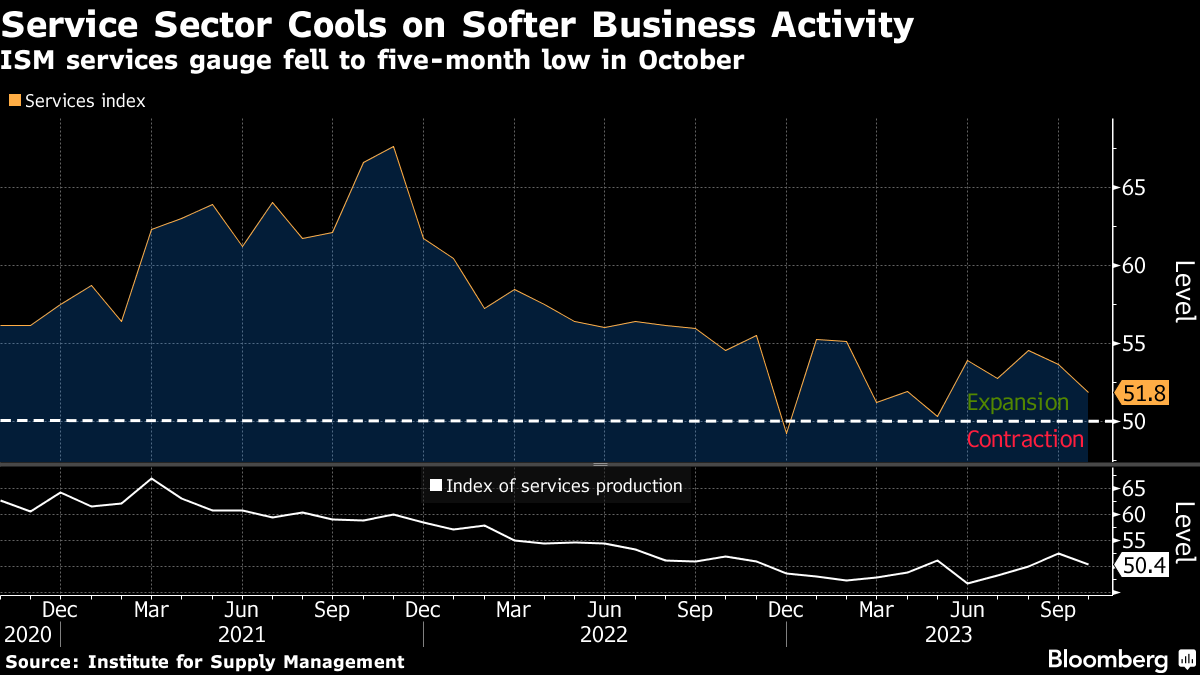

The Institute for Supply Management's overall gauge of services decreased 1.8 points, the most since March, to 51.8 last month. The index has been fluctuating on a month-to-month basis for the past year though it has remained above the 50 level that indicates expansion.

The median estimate in a Bloomberg survey of economists called for an October reading of 53.

The report issued Friday showed the business activity index, which parallels ISM's factory output gauge, posted its largest monthly decline this year. That helps explain why the services employment gauge retreated by the most since April 2022 to the lowest level in five months.

The survey suggests the economy is settling back in the fourth quarter after expanding in the previous three months by the most in nearly two years. While demand for services is holding up, a sustained slowdown would underscore a bigger impact from stiffer financial headwinds.

Twelve services industries reported growth in October, led by entertainment and recreation, retail trade and construction. Real estate, agriculture and mining were among the five industries that reported decreasing activity.

Soaring borrowing costs, wages that are no longer beating inflation and the resumption of student-loan payments all risk weighing on household demand in coming months.

At the same time, the ISM's gauge of orders placed with service providers rose 3.7 points after a sizable decline in the prior month, offering some hope that business activity will pick up.

Read More: US Jobs Data Show Broad Cooling After Run of Surprise Strength

While strength in the labor market has so far supported consumer spending, the government's monthly jobs report showed a broad cooling in October. Payrolls rose less than forecast and the unemployment rate unexpectedly increased to an almost two-year high of 3.9%.

Select ISM Industry Comments

“Strength in certain construction sectors is leading to continued optimism. Construction equipment and materials are at generally at lower prices and with faster deliveries. However, this is not the case for all materials or equipment.” — Construction

“Labor pressures continue, particularly in areas that are hard to recruit. Filling front-line and lower-skill labor positions has gotten very expensive because of competition from large companies and logistics providers.” — Health Care & Social Assistance

“We are taking a cautious approach due to the increase in crude oil prices. Capital projects have been slowed or postponed until oil prices stabilize. We expect this approach to continue through fiscal year 2024.” — Management of Companies

“The general outlook for our organization is less positive than anticipated from the beginning of the year.” — Transportation & Warehousing

“Due to the Israel-Hamas war, communications with clients in the Middle East are pretty much shut down.” — Professional, Scientific & Technical Services

“Business conditions have become murky as of late, but still going strong.” — Utilities

The ISM measure of prices paid retreated but remained at a level that shows costs are still rising at a stubborn pace.

The gauge of inventories at service providers shrank in October for the first time since April. An index of sentiment about the level of unsold goods eased somewhat but still showed companies see stockpiles as too elevated.

--With assistance from Kristy Scheuble.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.