Scan to Download

Posted By Sajeet

The government has reduced the divestment target for FY22 to Rs 78,000 crore compared to Rs 1.75 lakh crore. The target for FY23 is pegged at Rs 65,000 crore. The government is classifying the divestment receipts now under Misc. Capital Receipts.

So far, the divestment proceeds for this year are around Rs 12,000 crore. The dividends received from public sector enterprises stood at Rs 40,201.47 crore.

The government is unlikely to sell 10% in LIC this fiscal. The divestment would be around 5% in the current fiscal. But not sure the government has factored in LIC proceeds for next fiscal.

Post By Ira

In a continuation of Niraj's post, bond yields are now up 17 basis points. Bloomberg reports that gross borrowing for the year will be at Rs 14.95 lakh crore. That's only for the centre and that's huge. There will be larger than expected state borrowings too.

This is also a year when the RBI will not be able to do a huge amount to support government borrowing. Tough year for the rates markets.

Posted By Niraj

Fiscal Deficit at 6.4% is much higher than market expectation, and if one adds the state deficit, it is likely a shock to the bond market of some basis points. Compare that to the equity markets, which are probably going to like the big push to capex, as it is the need of the hour.

Posted by Menaka

FM says any income from transfer of any virtual digital asset to be taxed at 30%. Interesting wording. No mention of 'capital gains tax' here, just 'income'. But the way she said - could it apply to all crypto transactions?

Also a 1% TDS on transfer of virtual digital assets.

PS: Good that the 15% lower tax rate for new manufacturing units extended to 2024. Wish she had included service sector here.

Posted By Ira

The government's fiscal deficit for FY22 settled at 6.9%. They have announced consolidation of 0.5 percentage points, which takes the FY23 fiscal deficit to 6.4%.

Consolidation but at a measured pace.

For states, a fiscal deficit of 4% is being permitted again. This is also useful since state spending is critical in the next year. The government also plans to provide assistance of Rs 1 lakh crore over and above that.

All-in-all, the fiscal management has been prudent going by these pronouncements.

PS: We have taken note of the plan to introduce the digital rupee this year. We await details.

Posted By Ira

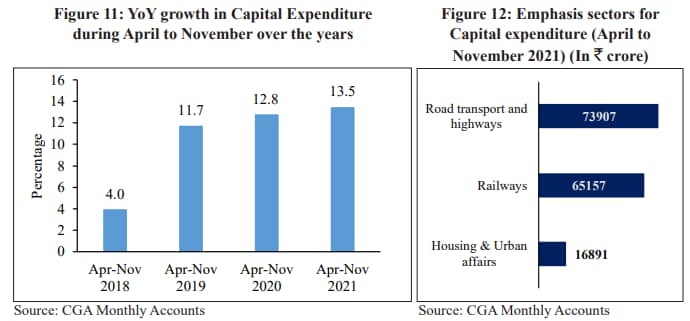

As expected, the government has upped its commitment to capital expenditure. On-budget expenditure has been raised to Rs 7.5 lakh crore, up 35.4% over last year's budget estimate of Rs 5.5 lakh crore.

This is encouraging, much needed but it still needs to be implemented.

Beyond capex, here are my top announcements from the first hour of the speech:

*India at 100 -- the government is taking a long view.

*Expanded loan guarantee -- useful but tread with caution.

*SEZ rethink -- good timing given that we need strong export growth to support the economy.

*Urban rethink - About time we do this. This space can contribute to investments too.

*Reducing corporate exit time - About time, again. Remember this was discussed as an issue with former chief economic advisor Arvind Subramanian in the Economic Survey of 2016.

Post By Ira

The government has announced that it will bring all post offices branches into the core banking system network. This could lay the roadmap towards bringing postal deposits into the mainstream financial system and make it easier to offer a wider suite of services to post office depositors. Reminder -- these deposits currently sit outside the financial sector. That's one reason the idea of a postal bank hasn't really picked up in India.

Posted By Ira

The government is expanding the emergency loan guarantee (ECLGS) announced against the background of the Covid crisis.

The scheme will be extended till March 2023 and its guarantee cover will be expanded by Rs 50,000 crore to total cover worth Rs 5 lakh crore, said Finance Minister Sitharaman.

The scheme has provided immediate relief to small enterprises but there is still no clarity on the quality of these loans. The government must tread with caution -- it is after all a contingent liability on the government's books.

Posted By Ira

Finance Minsister Nirmala Sitharaman begins by saying that this budget will set the stage for 'India At 100'. Goals include inclusive development, energy transition and financing of investment.

This year's budget also builds on budget of 2021-22. Like we said ahead of the budget -- stay the course.

Posted By Sajeet

India's largest insurer is all set to file its draft red herring prospectus for its initial public offer. The success of the IPO depends on foreign portfolio investors' appetite. The FPIs have withdrawn over Rs 1.10 lakh crore in the last four months. It is important that the budget should have policy to bring FPI back given the pipeline of IPOs expected in 2022.

With over 2.5 crore demat accounts added in the market, the budget needs to push for larger investors' participation in the primary market. It needs to bring in some incentive for retail participants to be long-term investors in the market.

Posted by Menaka

Nomura says it well in its post Economic Survey, pre-Union Budget note.

"...we expect a Budget that provides fiscal consolidation ‘in spirit’, but focuses on growth ‘in intent’."

Posted By Ira

The best thing the government can do in this year’s budget is stay the course.

2021-22 was the year the government tried to provide a springboard for an investment cycle — higher share of capex, a development finance institution, cleaner bank balance sheets. This year, it needs to see some of this through.

Public capex should remain high as we wait for a private investment cycle to kick off. Alongside, a renewed effort to improve the efficiency of government capital expenditure is needed.

In 2022-23, strong central government capex will also be important because of uncertainty around state finances (states account for two-thirds of general government capex). As Pinaki Chakraborty, director of NIPFP, pointed out in a recent interview, there are two uncertainties on the horizon for states next year — returning to a fiscal deficit of 3% after wider deficits were permitted during the pandemic and the planned end of GST compensation in June 2022. It may be for these reasons that states are holding on to large cash balances and not spending as much as they could this year. The central government will have to keep its spending taps open and do its bit to provide as much predictability to states transfers as possible. We won’t get into the GST compensation debate here.

Beyond capex, there is a case for extended food transfers, a well-funded MGNREGA and perhaps additional pockets of social security if there is space. We don’t think there has been enough design thinking to launch an urban jobs guarantee scheme yet, at least at a large scale. Hold off on that.

BofA Securities sees scope for some demand stimulus via tax rationalisation for lower income segments. Should the government attempt that? Sure. But again, if there is space.

What is ‘space’ the government has? The government should target fiscal consolidation of about 0.5 percentage points, bringing it close to 6-6.3%. Even at that level, a gross borrowing of about Rs 12 lakh crore will be tough for the bond market to absorb.

It is possible that the government tries to resolve the pending tax issues to enable a global bond listing in the budget. If they do, there may be some relief on bond yields on the expectation of a new source of demand for government securities. But given how long this global bond index listing story has stretched out, we’ll believe it when we see it.

Stay tuned.

Made Sunday lunch:-peerkan kai curry, inji thugaial, murugai illai mor kuzhambu.Finished off with thayir(not in pic) pic.twitter.com/FYEevPVDLS

— Nirmala Sitharaman (@nsitharaman) July 31, 2016

Indian Economy Contracted Less Than Projected In FY21

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.