(Bloomberg) -- The dollar is on pace for its biggest drop in almost two months as Treasury yields extended a slump and traders pared bets on further Federal Reserve interest-rate hikes.

The Bloomberg Dollar Spot Index was down 0.5% at around midday Thursday in New York, on track for its steepest decline since Sept. 11. The greenback sank against nearly all of its Group-of-10 peers, with the New Zealand dollar leading gains.

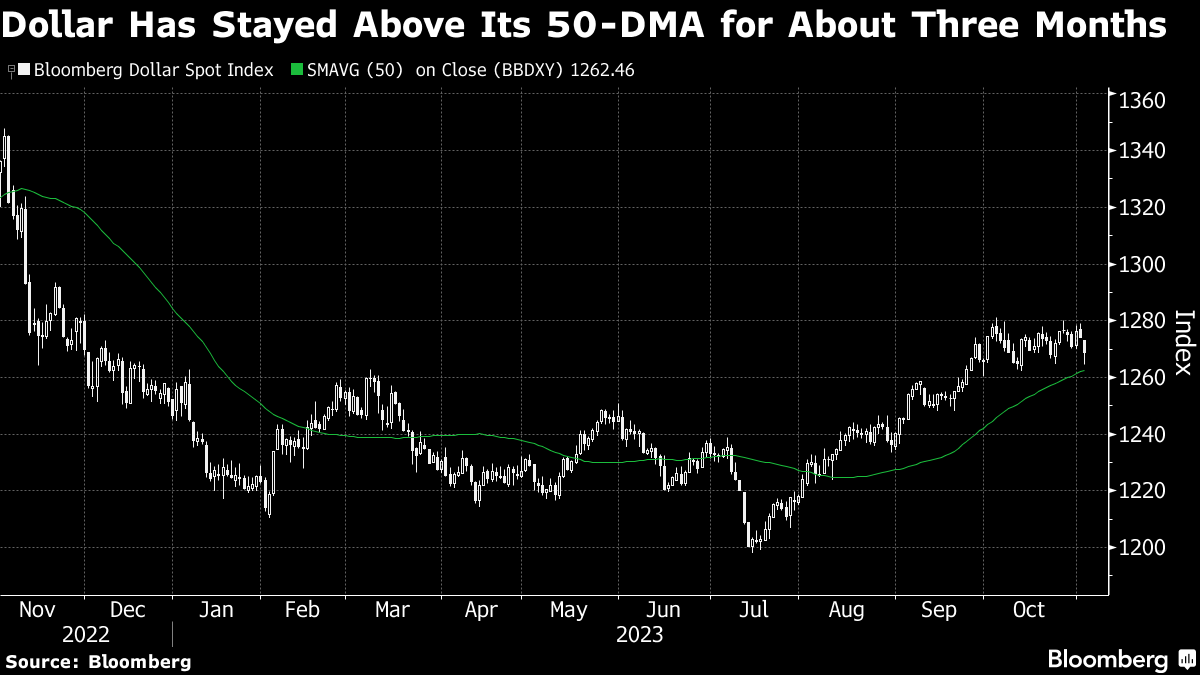

The dollar is still up almost 2% in 2023, after advancing the past three months as the Fed held its benchmark rate at the highest in more than two decades. But with investors interpreting Wednesday's Fed decision as signaling the central bank may be done hiking, that's adding to the sense in the market that the US currency is at a near-term peak.

“The market is running with the dovish Fed narrative and pushing back on the crowded long dollar trade,” said Erik Nelson, a strategist at Wells Fargo. Friday's release of monthly US payrolls figures “will be crucial in determining whether the dollar sell-off has further to run,” he said.

Fed Chair Jerome Powell said Wednesday that additional evidence of strength in the labor market and above-trend economic growth could trigger further tightening.

However, the median forecast in a Bloomberg survey is that job growth slowed sharply last month from the September pace.

With a weak report, “you can kiss the chance of one more Fed rate hike this cycle goodbye,” said Edward Moya, senior market analyst at Oanda Corp. “Continued momentum behind these moves — weaker dollar and a bond-market rally — could last a while longer given how the market was positioned.”

--With assistance from George Lei.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.