(Bloomberg) -- Wall Street traders shrugged off a mixed inflation report, with stocks and bonds edging higher as traders waded through remarks from Federal Reserve Chair Jerome Powell.

Just 24 hours before the release of the consumer price index, a gauge of producer inflation rose more than forecast. Looking beneath the surface, though, its details offered some relief as key categories that feed into the central bank's preferred inflation measure were more muted.

*POWELL: US ECONOMY HAS BEEN PERFORMING VERY WELL LATELY

“Sticky inflation looked downright stuck this morning after a much hotter-than-expected inflation reading,” said Chris Larkin at E*Trade from Morgan Stanley. “But with last month's numbers revised lower, this report may not have been as much of an upside shock as it first appeared to be.”

The S&P 500 hovered near 5,230, adding to an advance that's sending the measure close to all-time highs. Meme-stock traders again piled into shares of GameStop Corp. and AMC Entertainment Holdings Inc., a day after both soared in a revival of the retail frenzy. Two-year yields fell three basis points to 4.83%.

The producer price index for final demand increased 0.5% from a month earlier, driven largely by services and following a downwardly revised 0.1% drop in March. Compared with a year ago, the PPI rose by the most since April 2023. Several categories in the PPI report that are used to calculate the personal consumption expenditures price index — eased.

“A more granular look suggests the components that feed into PCE inflation sent mixed signals,” said Krishna Guha at Evercore. “This means that the burden largely remains on CPI – which will be released Wednesday.”

Underlying US inflation probably moderated in April for the first time in six months, offering a ray of hope that price pressures will start to ease again after a string of upside surprises. The core consumer price index, which excludes food and fuel, is seen rising 0.3% from a month earlier after 0.4% advances throughout the first quarter. Compared with April 2023, the core CPI is projected to rise 3.6%.

“The most important data release is tomorrow's CPI print because the Fed's dual mandate is based on CPI and unemployment, with the former being what the Fed is solely focused on right now,” said Chris Zaccarelli at Independent Advisor Alliance.

Zaccarelli says he belives the stock market will move higher throughout the year on strong corporate profits and consumer spending, but volatility is likely to spike in the meantime, because the inflation data is going to keep the Fed on edge.

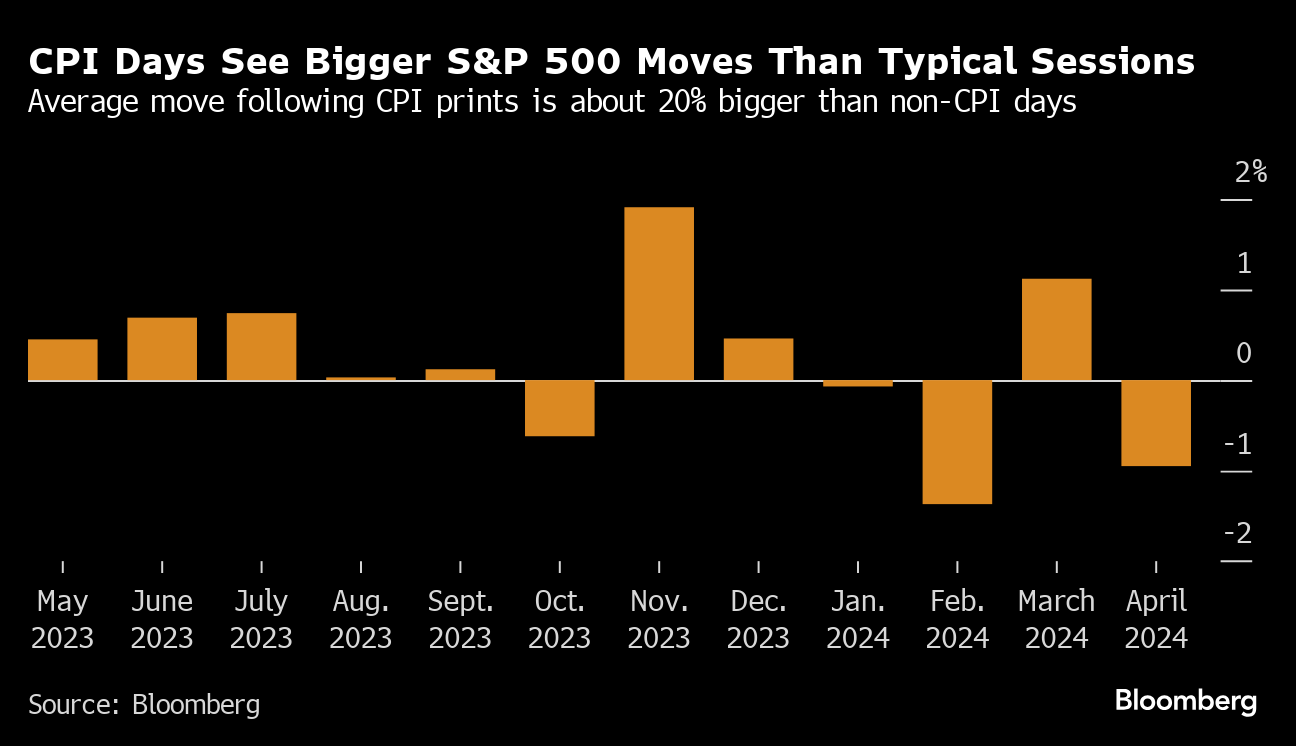

Investors who have positioned for big stock swings on macro event days have been rewarded this year.

Buying a one-day S&P 500 straddle — composed of owning a put and a call option with the same strike price — for days with large data releases or economic catalysts have generated an average 21% since the fourth quarter of last year.

That's according to an analysis from Susquehanna International Group that looked at returns on sessions aligned with events like Fed meetings, inflation figures, and nonfarm payrolls reports.

More Comments on PPI:

- Quincy Krosby at LPL Financial:

Moreover, this report underscores Fed concerns that the path of disinflation has stalled, requiring a higher-for-longer policy stance to combat seemingly entrenched inflation.

An overriding question — and potential dilemma — hovering over markets is whether the broader economic landscape is softening at the same time inflation inches higher, making the Fed's job increasingly difficult.

- Bill Adams at Comerica Bank:

Between an upside surprise and downward revisions to prior data, the trend in total PPI was slightly higher than expected in April.

The PPI report suggests upside risk to the April CPI report, which will come out tomorrow.

At the margin the Fed will see the PPI report as another reason to slow-roll interest rate cuts.

- Paul Ashworth at Capital Economics:

These days we mostly care about what the PPI means for the Fed's preferred PCE deflator measure of core consumer price inflation.

In that respect, April's news was mixed but, on balance, encouraging. The bad news is that PPI portfolio management prices increased by 3.9% m/m. But that was more than outweighed by the good news. We'll know more after the release of April's CPI tomorrow.

- Scott Helfstein at Global X:

Inflation and the Fed are less important than growth, and companies have adjusted to the new reality of higher prices and continue to look for technology solutions to manage for profit.

The last mile on inflation was always going to be the hardest, but we should be comfortable with these numbers.

Wagers on interest rate cuts have sent investor optimism to a two-and-a-half-year high, but stocks will suffer if evidence of “stagflation” materializes, according to Bank of America Corp. strategist Michael Hartnett.

According to BofA's global poll, a majority of fund managers see the Fed cutting rates in the second half of 2024. That has lifted sentiment — derived from a combination of cash levels, equity allocation and economic growth expectations — to the highest since November 2021. Within that mix, however, the outlook for economic growth and corporate profits has deteriorated for the first time this year, the survey showed.

Corporate Highlights:

- Home Depot Inc.'s string of negative sales extended into a sixth straight quarter as the big-box retailer struggles to overcome a weak housing market and lower demand for big-ticket items.

- Tencent Holdings Ltd. reported a far better-than-projected 62% surge in earnings while rival Alibaba Group Holding Ltd.'s profit plunged, highlighting the growing divergence between China's twin internet powerhouses during a rocky post-Covid recovery.

- Comcast Corp. will offer customers a streaming bundle that includes Apple TV+, Netflix and its own Peacock service as it tries to reduce subscriber churn, Chief Executive Officer Brian Roberts said Tuesday at an investor conference.

- Hydrogen producer Plug Power Inc. surged after the Biden administration offered the US company a conditional commitment for $1.66 billion in loan guarantees to build up to six facilities.

- Verizon Communications Inc. is interested in buying back US Cellular Corp.'s stake in its Los Angeles business if the companies can agree on a reasonable price, the chief of Verizon's consumer division said.

- The top US auto-safety regulator opened an investigation into Waymo, the autonomous-vehicle subsidiary of subsidiary of Alphabet Inc., after 22 incidents in which the company's cars were involved in collisions or may have violated traffic laws.

- Stellantis NV will start selling cars made by Chinese partner Leapmotor in Europe as part of a global expansion as the automaker fights to lower the cost of electric vehicles.

Key events this week:

- China rate decision, Wednesday

- Eurozone industrial production, GDP, Wednesday

- US CPI, retail sales, business inventories, empire manufacturing, Wednesday

- Minneapolis Fed President Neel Kashkari speaks, Wednesday

- Japan GDP, industrial production, Thursday

- US housing starts, initial jobless claims, industrial production, Thursday

- Philadelphia Fed President Patrick Harker speaks, Thursday

- Cleveland Fed President Loretta Mester speaks, Thursday

- Atlanta Fed President Raphael Bostic speaks, Thursday

- China property prices, retail sales, industrial production, Friday

- Eurozone CPI, Friday

- US Conf. Board leading index, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 was little changed as of 10:06 a.m. New York time

- The Nasdaq 100 was little changed

- The Dow Jones Industrial Average rose 0.2%

- The Stoxx Europe 600 was little changed

- The MSCI World index rose 0.2%

Currencies

- The Bloomberg Dollar Spot Index fell 0.1%

- The euro rose 0.3% to $1.0818

- The British pound rose 0.2% to $1.2580

- The Japanese yen was little changed at 156.35 per dollar

Cryptocurrencies

- Bitcoin fell 2.3% to $61,622.88

- Ether fell 2% to $2,895.05

Bonds

- The yield on 10-year Treasuries declined three basis points to 4.46%

- Germany's 10-year yield advanced one basis point to 2.52%

- Britain's 10-year yield declined two basis points to 4.15%

Commodities

- West Texas Intermediate crude fell 0.5% to $78.72 a barrel

- Spot gold rose 0.7% to $2,353.62 an ounce

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Carly Wanna.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.