Rising crude prices have made Oil and Natural Gas Corporation Ltd. the best bet among oil explorers in Asia.

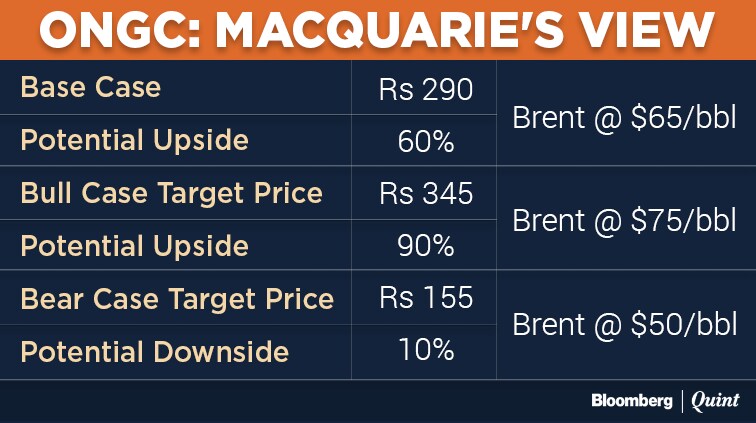

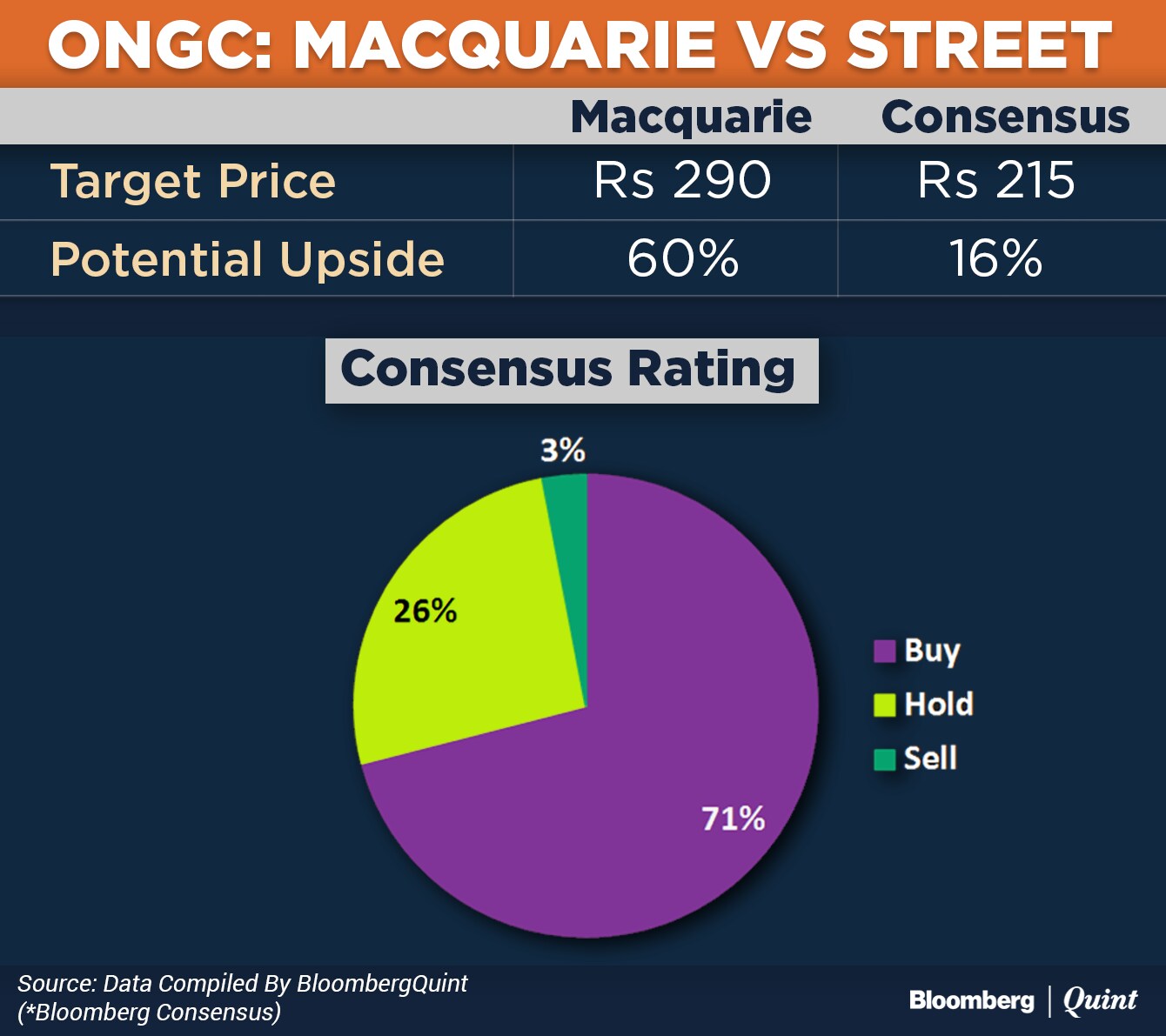

That's Macquarie Research's forecast for India's largest energy company. It set a target price of Rs 290 for ONGC—the most bullish estimate in the street. The brokerage also has a bull case target price of Rs 345 apiece if oil prices go as high as $75 a barrel.

ONGC is the most preferred stock among peers with only one of the 38 analysts tracked by Bloomberg having a ‘Sell' rating.

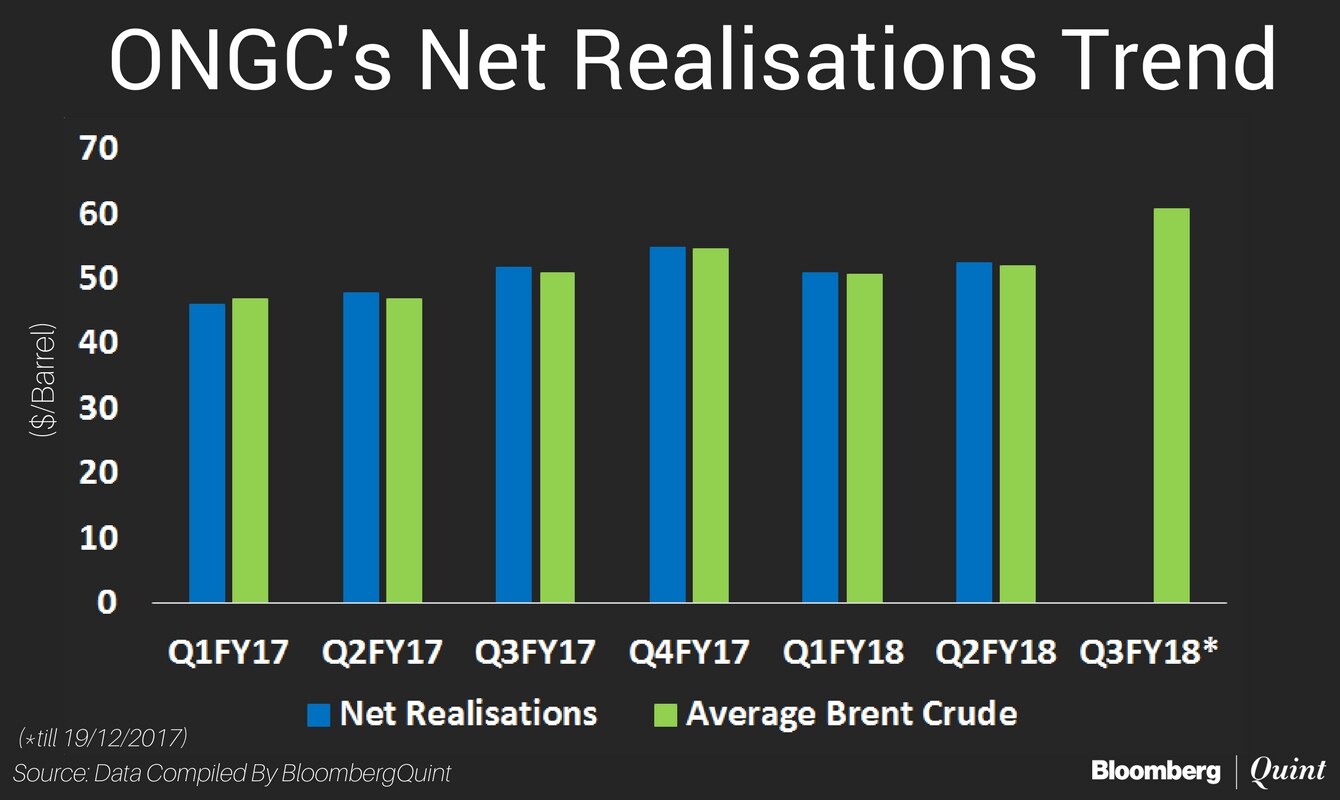

Macquarie expects the explorer to benefit from the surge in Brent, predicting the long-term oil price at $65 a barrel. Brent rose nearly 39 percent in the last six months compared to a 12 percent rise in ONGC shares. The current stock price reflects oil at $52 a barrel, the brokerage said. Costlier oil improves realisations and margins for the company, it said.

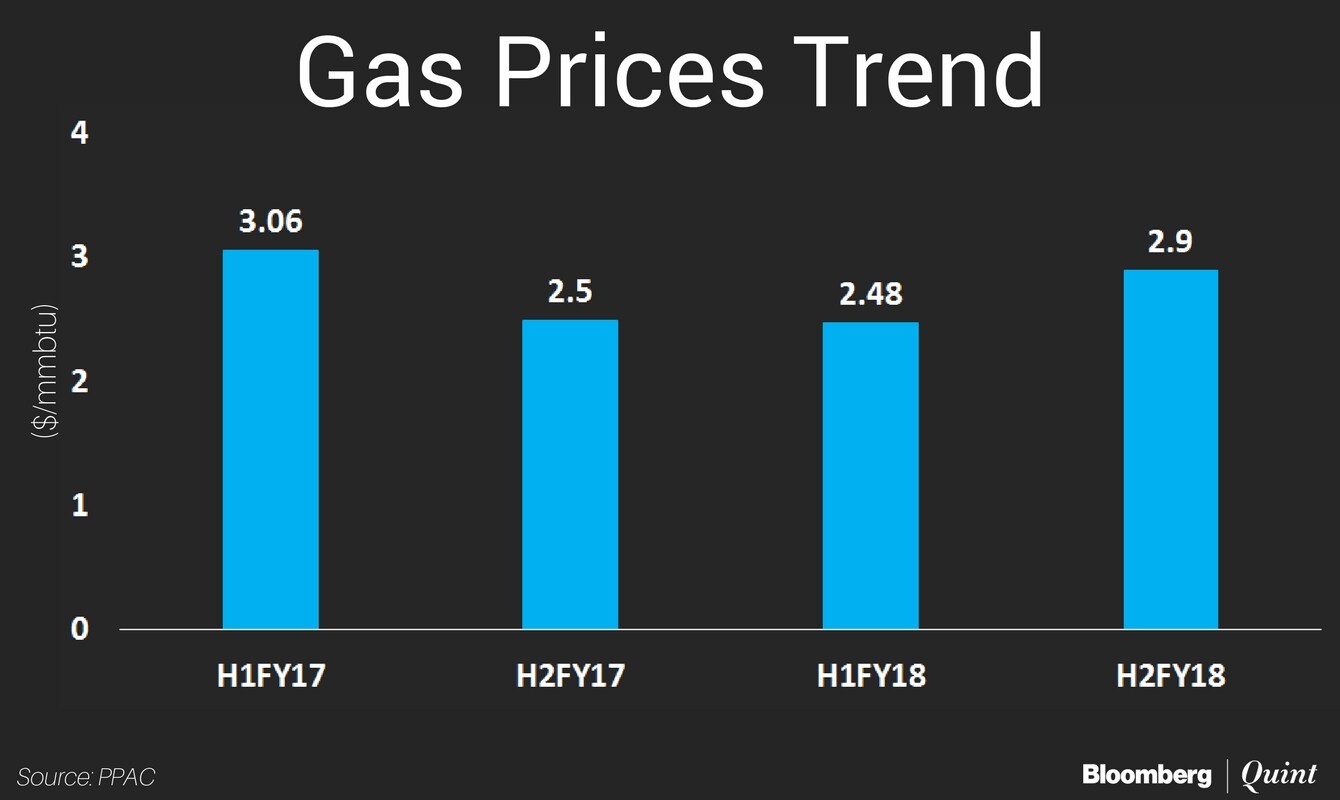

Macquarie also expects ONGC's gas realisations to rise $4.3 per million British thermal unit on the back of an expected increase in administered prices.

Output Growth

ONGC's oil and gas output is likely to rise after five years of lacklustre performance as 14 new projects with final investment plans are commissioned, Macquarie wrote. Its production is expected to grow at an annualised rate of 6 percent—from 47 million tonne of oil equivalent to 63 million—in five years to March 2022. The proportion of gas is expected to rise from 45 percent to 58 percent during the period, according to the brokerage.

HPCL Overhang

ONGC's shares have underperformed partly because of lack of clarity in the acquisition price of government's stake in oil refiner Hindustan Petroleum Corporation Ltd. ONGC's balance sheet can easily absorb HPCL, Macquarie said. The deal would add to the explorer's profit growth even if it pays a 50 percent premium to the market price, the brokerage said.

Other Highlights

- Expect 5 percent free cash flow yield over financial year 2017-18 to 2019-20.

- Beyond the year ending March 2020, free cash flow yield to rise to 14 percent on completion of planned projects.

- Expect favourable dividend yield of 6 percent in five years to March 2022.

Also Read: Oil And Gas PSU Mergers Exempt From CCI Approval For Five Years

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.