UltraTech Cement Ltd. delivered a strong fourth-quarter performance, beating Jefferies' estimates and signalling a sharp turnaround after three consecutive quarters of Ebitda decline, stated a recent note by the brokerage. Jefferies reiterated its 'buy' rating on UltraTech and raised its price target to Rs 14,000.

The company also completed the full integration of its Kesoram and India Cement operations during the quarter, restating historical financials accordingly. The management outlined an ambitious roadmap to strengthen profitability at Kesoram and ICEM. Improvement levers include higher capacity utilisation, better pricing, cost efficiencies, and overhead optimisation, as per the note.

Consolidated Ebitda rose 12% year-on-year to Rs 4,620 crore, ahead of the brokerage's forecast of Rs 4,360 crore, driven by better-than-expected cost efficiencies.

On the cost front, UltraTech reiterated its goal of achieving Rs 300 per tonne in cost savings, of which Rs 86 per tonne has already been realised in fiscal 2025, as per the note.

Meanwhile, UltraTech's building materials division continues to gain traction, as per the note. The number of UBS outlets rose to 4,615 in the final quarter of fiscal 2025, contributing over 20% to domestic grey cement sales volumes. The division, currently clocking an annual revenue run rate of around Rs 1,000 crore, is expected to triple to Rs 3,000 crore over the next three years.

Looking ahead, Jefferies noted that the recent uptick in pricing should benefit UltraTech's profitability in the first quarter of this fiscal, even though industry demand could be subdued due to heatwave conditions.

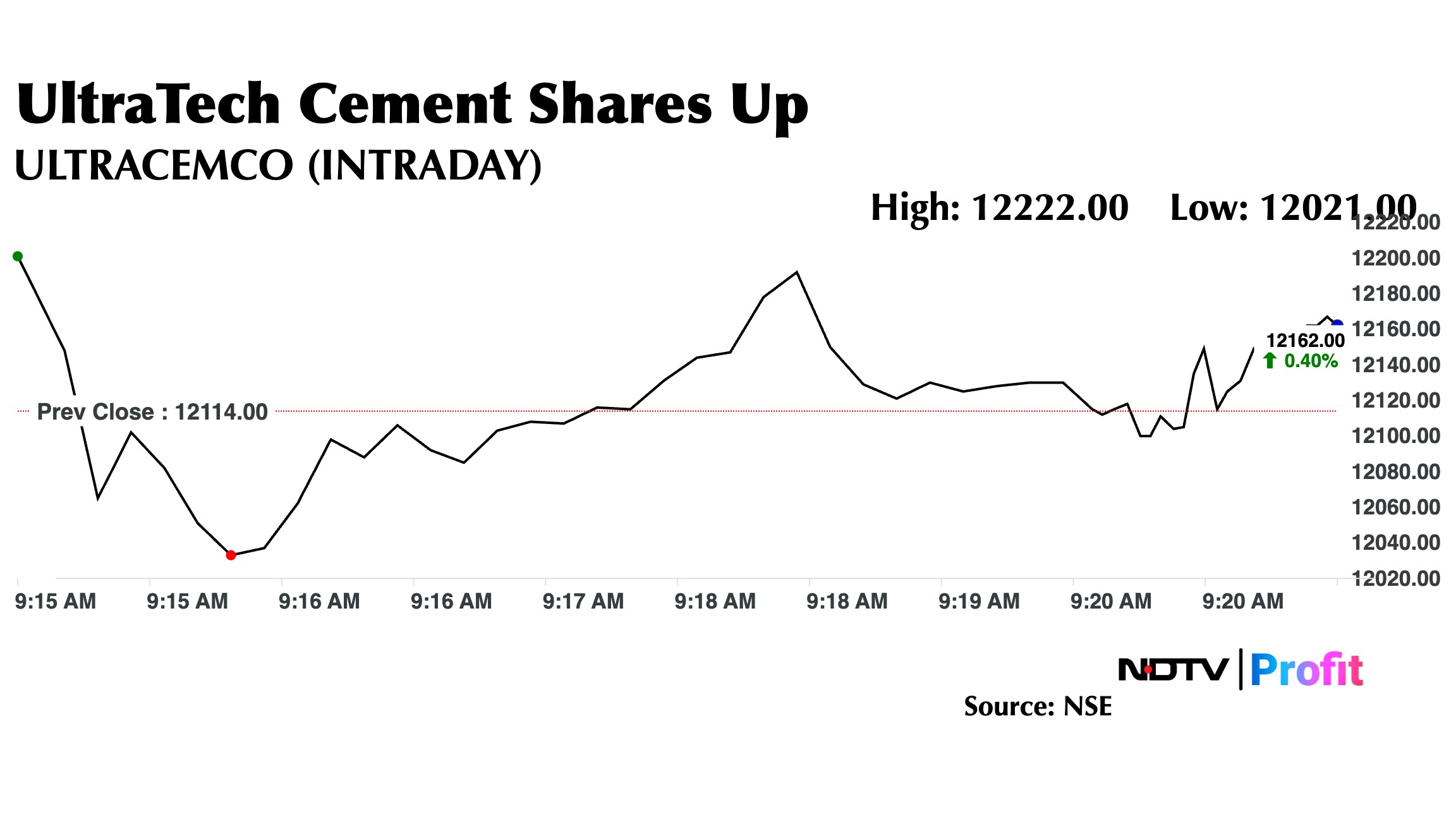

UltraTech Cement Share Price Today

The scrip rose as much as 0.89% to Rs 12,222 apiece. It pared gains to trade 0.08% higher at Rs 12,124 apiece, as of 09:19 a.m. This compares to a 0.45% advance in the NSE Nifty 50 Index.

It has risen 6.03% on a year-to-date basis and 21.58% in the last 12 months. Total traded volume so far in the day stood at 0.07 times its 30-day average. The relative strength index was at 43.51.

Out of 44 analysts tracking the company, 36 maintain a 'buy' rating, four recommend a 'hold', and four suggest 'sell', according to Bloomberg data. The average 12-month consensus price target implies an upside of 4.3%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.