This article explains a recent Notification dated June 8, 2017, issued by the central government notifying the rules for withholding tax on rent payment exceeding Rs 50,000 to a resident by an individual or Hindu Undivided Family (HUF).

Prior to the amendment by the Finance Act 2017, the Indian tax laws required any person liable to pay rent to residents for use of any land/building exceeding an annual amount of Rs 1,80,000 to withhold tax at the rate of 10 percent. However, individuals and HUF not liable to tax audit under the tax laws, were excluded from the obligation of withholding tax.

In order to widen the scope of withholding tax, Finance Act 2017 has introduced a new provision in the tax laws to provide that individuals or HUF (other than those liable for tax audit under the tax laws) responsible for paying to a resident, on or after June 1, 2017, any income by way of rent exceeding Rs 50,000 for a month or part of month during the tax year, shall deduct an amount equal to 5 percent of such income as income tax thereon.

In order to reduce the compliance burden, Finance Act 2017 provides that the deductor is not required to obtain a Tax Deduction Account Number (TAN) and is liable to deduct tax only once in a tax year. The tax should be deducted at the time of credit or payment (whichever is earlier) of rent for the last month of the tax year or last month of the tenancy if the property is vacated during the year, as applicable.

Additionally, where the tax is required to be deducted at a higher rate in the absence of the Permanent Account Number (PAN) of the payee, such deduction is not to exceed the amount of rent payable for the last month of the tax year or the last month of the tenancy, as the case may be.

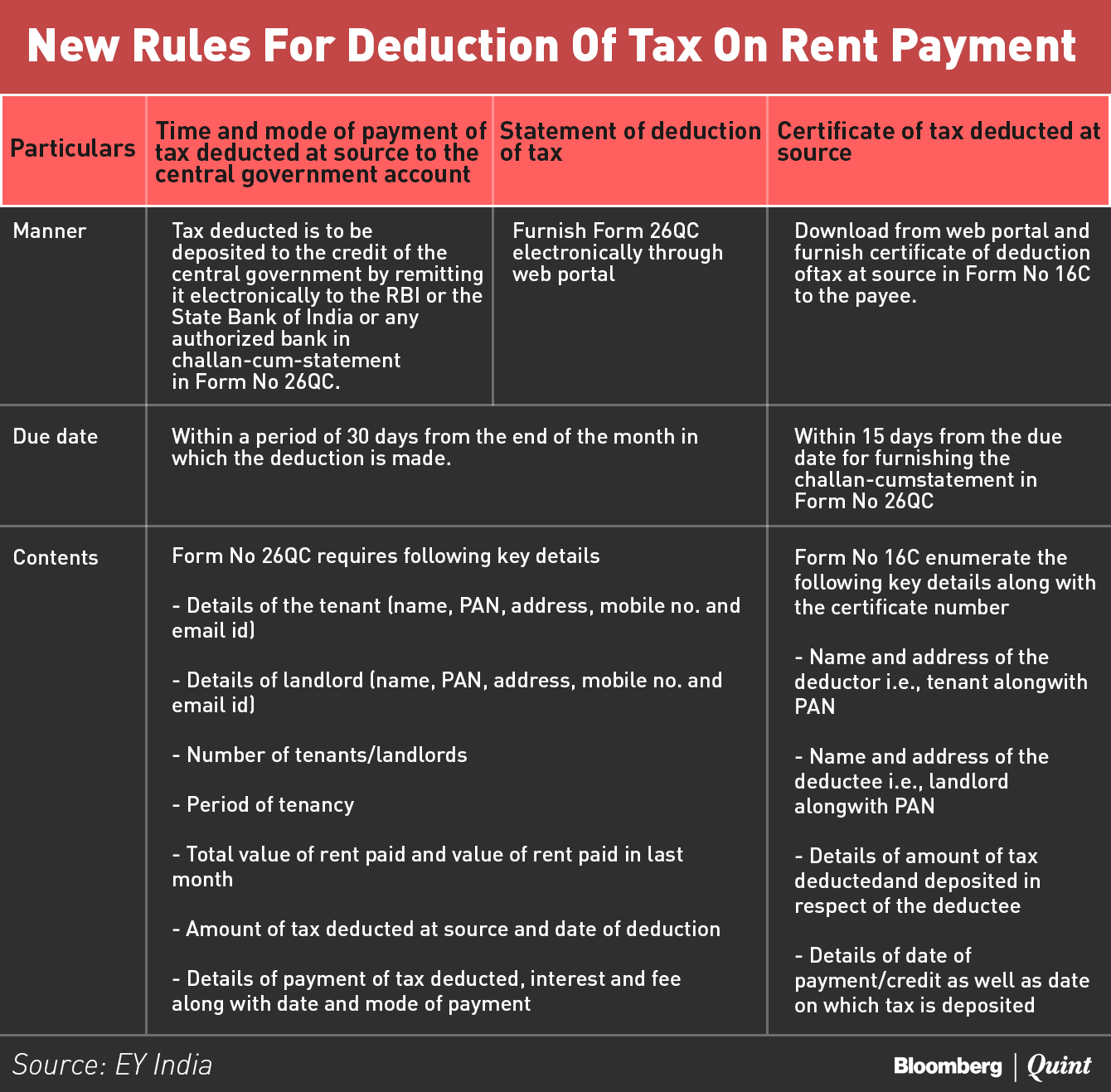

In order to harmonize the new provision with the existing rules, the Central Board of Direct Taxes (CBDT) has amended the existing rules to provide for the time and mode of payment of tax deducted at source to the central government account as well as the manner in which the certificate of tax deducted at source and the statement of deduction of tax are to be furnished by the payer.

The new provision which cast a tax deduction obligation on individual and HUF who are not liable for a tax audit, under the provisions of the tax laws, has come with effect from June 1, 2017. Such payers will need to ensure withholding tax compliance on payment of rent to residents in excess of Rs 50,000 per month within the timelines and in the form prescribed under the new rules to avoid any adverse consequences by way of additional fees, interest, penalty or prosecution.

This article was first published on the EY Tax Alert Bulletin.

EY India is amongst the top 4 professional business consulting and management consulting firms in India.

The views expressed here are those of the author's and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.