Lending to large corporate customers and existing retail clients is easy. Corporate customers have well documented credit profiles. Existing retail clients, too, have a history that banks can track. But expanding the client base by bringing in new customers and ensuring those clients meet the lending criteria is tedious.

So what if someone did that job for the banks? Found clients, assessed their credit worthiness and underwrote the initial risk?

That's the thinking on which IndiaLends was founded in 2014. The company functions as an online credit underwriting platform that is attempting to widen the ambit of formal credit. They do this by using proprietary algorithms to score potential borrowers and then connect these individuals to banks and non-banking finance companies (NBFC).

We're trying to help more people get access to formal credit by finding data points that are relevant to underwrite them and on that basis provide them credit from banks and regulated entities like NBFCs.Gaurav Chopra, Co-Founder, IndiaLends

Underwriting a loan essentially means bearing the risk of default. A company underwrites a loan for a fee, generally paid by the borrower. In the event of a default, the company has to compensate the creditor.

An external underwriting platform may come in handy for banks at a time when most are focusing on retail loans due to the lack of demand for large corporate credit. Despite this increased focus on retail lending, the conversion rate (that is the conversion of loan applications into actual loan disbursal) has remained in single digits. The reason for this, according to Chopra, is that a large number of potential borrowers do not have a good enough credit score to qualify them for a loan.

“So that was the problem we were trying to solve. And the way we are solving it is by being consumer facing, providing them (customers) with products such as a loan, a pre-credit report, a personal finance manager and a credit education for that matter,” said Chopra.

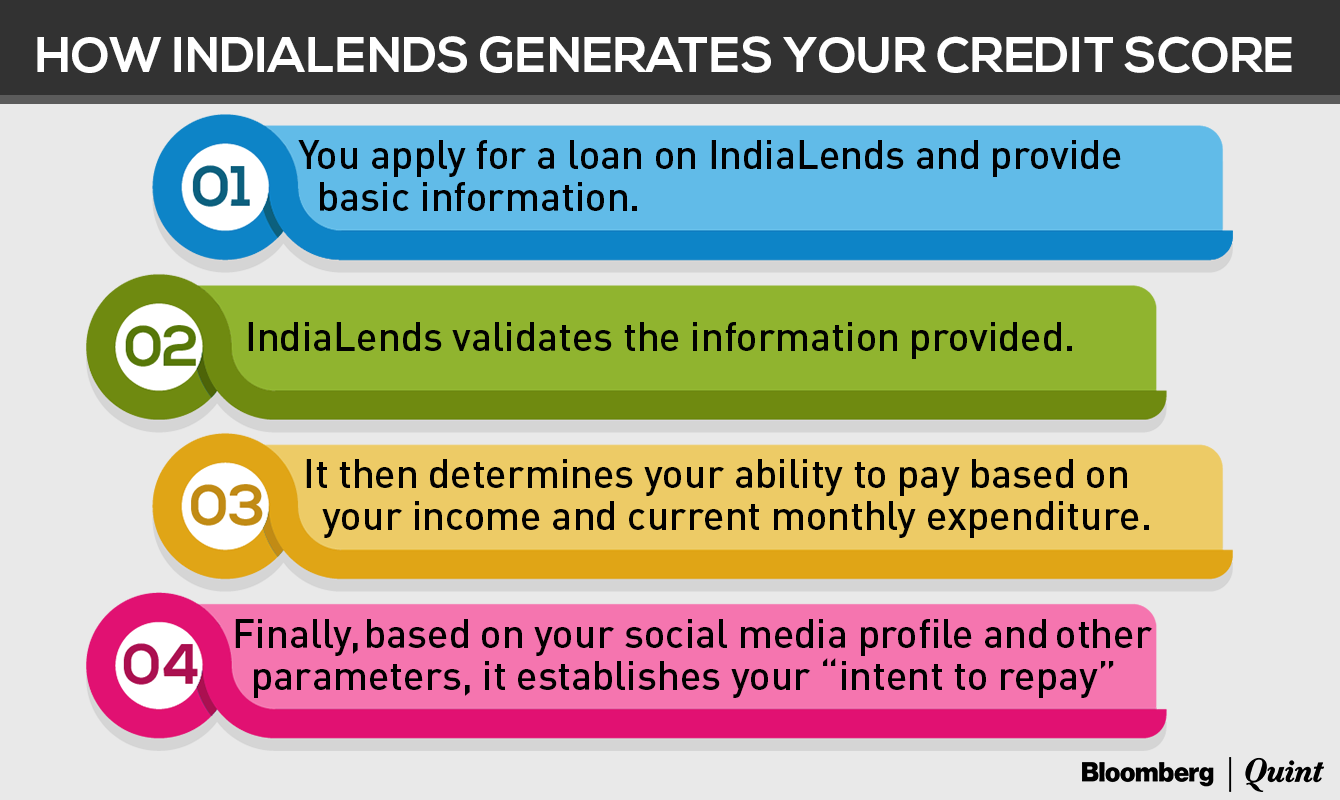

How The Platform Works

IndiaLends first validates whether the basic information provided by a potential borrower is accurate. This would include information like educational qualifications, place of work, and residence.

As a second step, the company determines the ability of a potential borrower to repay a loan. This is determined based on income, regular expenditure and current debt if any.

The final step, and one that is perhaps the toughest, is to determine the “intent” of the potential borrower.

“I'm not taking any guarantee or collateral. So what is the guarantee that you have the value systems to pay it back,” said Chopra.

The inputs can be a variety of things, such as your education background, your work history, how much you're earning, your existing debt, your friend circle, your social circle, your behaviour on e-commerce, your behaviour with other payments, utilities, and your mobile phone behaviour. So all these things come in, which then forms what you call a score card or a credit score.Gaurav Chopra, Co-Founder, IndiaLends

Based on the score that is generated, one of the company's banking or NBFC partners decides to provide credit. Currently, IndiaLends has 40 such partners, including HDFC Bank, ICICI Bank, Bajaj Finserv, and Capital First.

The company continues to track the performance of a borrower after a loan is disbursed, and additional data is used to strengthen the overall assessment. IndiaLends currently has a database of over 2 lakh customers.

How Does IndiaLends Make Its Money?

The company charges a fee on every loan that is generated, which is added to the interest rate that is levied by the bank or NBFC. Depending on the borrower, this ranges between 1-4 percent, said Chopra.

Since inception, IndiaLends has originated loans worth over Rs 100 crore and has a monthly run rate of over Rs 15 crore currently. The volumes have been doubling every quarter since inception, according to information provided by the company. BloombergQuint could not independently verify these figures.

At present, IndiaLends gets between 25,000 and 30,000 applications for loans ranging from Rs 25,000 to Rs 25 lakh, said Chopra. He claims the company's conversion rate is higher than that of the banking industry, which is below 10 percent.

At the current rate of growth, the company aims to break even within the next two and a half years.

I think we are looking at variable cost breakeven happening in the next 12-16 months and overall breakeven should happen in the next 24-30 months (give or take three to six months). This is in line with what we had initially anticipated.Gaurav Chopra, Co-Founder, IndiaLends

IndiaLends was initially bootstrapped by the co-founders Mayank Kachhwaha and Gaurav Chopra between September 2014 and June 2015. In July 2015, the company closed its first round of funding, in which it raised $300,000 (worth Rs 2 crore at the current exchange rate).

The investors included DLG Consumer Partners, Siddharth Parekh, a partner at Paragon Partners and Gautam Radhakrishnan, a partner at the Tata Opportunities Fund.

“This (round of funding) was essentially supposed to last us one year, but very soon after raising this money, we started scaling rapidly, which resulted in us doing a round of funding in October 2015,” said Chopra. In this round, the company raised $1 million (currently worth Rs 6.7 crore), from the same investors.

The final round of funding came not too long back, in November, and was led by American Express Ventures. “We saw participation from all existing investors. Plus, we had a Chinese investor come in and another Indian fund come in. So this was $4.5 million (Rs 30 crore),” he said.

Does IndiaLends Stand Apart?

According to Chopra, IndiaLends cannot be compared with other companies in India, because it performs a combination of functions. In the first place, the company is a market place for loans, along the lines of Paisabazaar and BankBazaar.

The second function is risk analytics, which a number of institutions, including credit bureaus and other identity verification companies like Singapore-based Lenddo perform.

The third function, Chopra said is the technology platform. The website, he said, attempts to make the user experience easier for both the borrower and creditor.

“The fact that we combine all these three, means that there is no direct competitor that I can name that is doing all three things together,” he said.

Rajnish Kumar, managing director at State Bank of India (SBI), the country's largest lender, admits that data analytics broadens the scope of formal credit. However, Kumar believes the bank's own data analytics gleaned from information on its 30 crore customers is more than sufficient.

He adds that despite the underwriting service provided by IndiaLends, the larger banks are unlikely to enter what he calls the “sub-prime” category.

“For SBI, the loans that are taken are generally low to medium risk and the pricing is moderate. It is a question of strategy,” he said. “In the informal sector, the rates charged are as high as 30 percent. But if SBI started charging 20 percent, questions would be raised about the bank's strategy.”

Kumar said that a bank with the size and scale of SBI has the wherewithal to create its own data analytics. Smaller institutions, however, may prefer to tie up with institutions like IndiaLends, he admitted.

IndiaLends, which started in three cities–Delhi, Mumbai, and Bengaluru–is now present in 12 large cities. These include some Tier-II cities like Jaipur, Chandigarh, and Ludhiana. In the next stage of expansion, the company will expand into more Tier-II cities. By the end of the year, IndiaLends wants to be present in 35 cities.

In terms of volume growth, Chopra believes there is no plateau in sight.

“Expecting even a million applications a month is doable. But, it is more that the growth that we are anticipating needs to be structured growth, which means that we should not fall flat because of the volumes coming in. At the same time, we do want to maintain at least a 100 percent (growth in volumes) quarter on quarter,” he said.

This report is part of a series profiling fintech firms changing the way financial services operates in the India. The series will play out every weekend on Bloombergquint.com

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.