(Bloomberg) -- China's local government financing vehicles are increasingly offering to redeem their bonds before maturity, tapping Beijing's support to lower financing costs while seeking to sustain investors' interest.

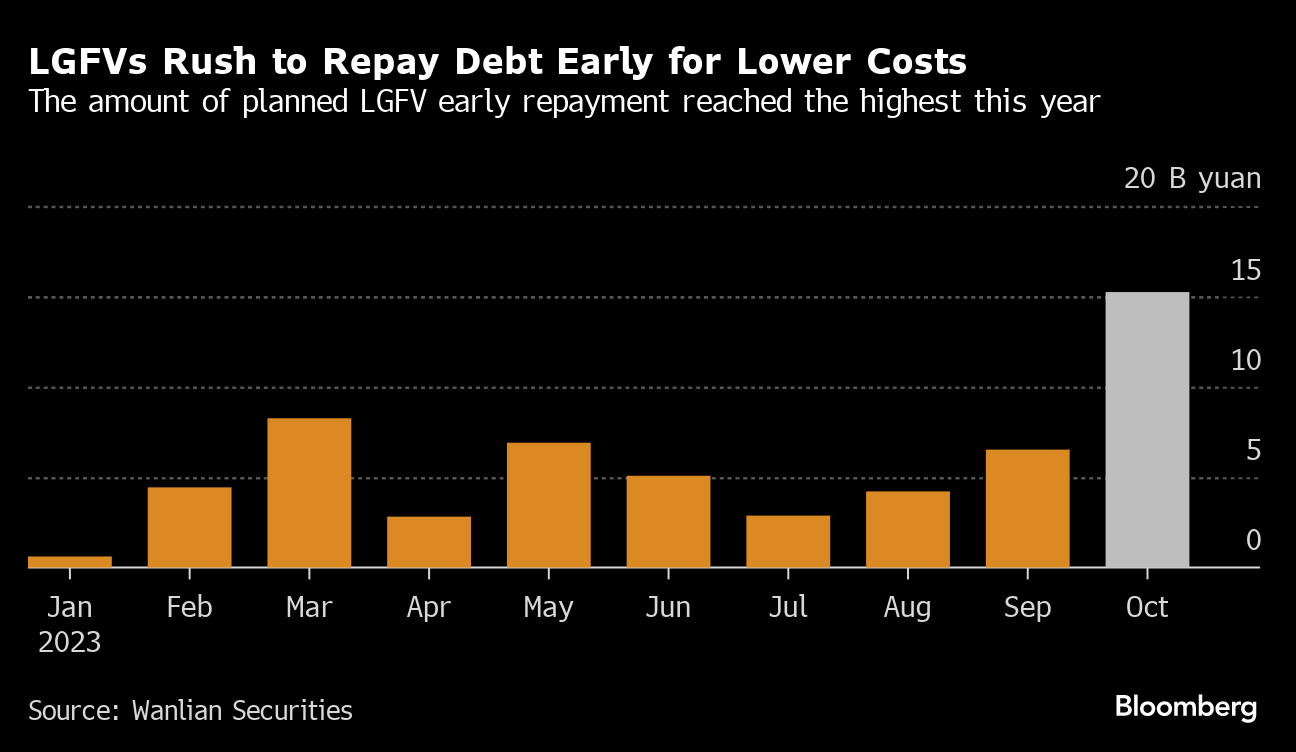

As of Oct. 27, there were 33 LGFV bonds, worth about 15 billion yuan, that had been planned for early payment, according to data from Wanlian Securities Co. It was the highest monthly total for the year and up from 25 in September and 19 in August.

LGFVs — used by provinces and cities for public infrastructure projects, like roads and ports — have been emboldened by a central government program, reported by Bloomberg News in August, that allows local governments to issue about 1 trillion yuan of bonds to repay LGFV debt and other off-balance sheet issuers.

LGFVs' early redemptions and a surge in special refinancing bonds are “correlated,” said Li Yong, chief fixed-income analyst at Soochow Securities Co.

Early payments will likely soothe investors who are concerned about their returns amid China's economic downturn and property market troubles. But even with lower financing costs for LGFVs, the refinancing mechanism will likely raise more questions about whether the quest to reform the heavily indebted sector is being addressed with lasting solutions.

Special refinancing bonds aren't new. But their popularity is surging after Beijing's new bond program and other support measures announced earlier in the year to address mounting local debt.

As of Oct. 27, there were 24 provinces in China that disclosed a total of more than 1.04 trillion yuan of planned special refinancing bonds, according to a report by Tianfeng Securities Co.

Even financially struggling regions, like Guizhou, are partaking in the trend. Guizhou Water Investment Group Co., an LGFV, said it plans to fully repay early a 1 billion yuan bond, due to mature in 2025.

A hike in special refinancing bond issues often is followed by large-scale early redeeming of LGFV bonds, Li said, citing a similar trend that unfolded in 2021.

LGFVs' early repayments are hardly a reflection of their financial soundness. They on average recorded a loss of 58 million yuan for the first half, the most since 2014, according to a CICC report.

Other signs of stress are also emerging. While there has been no public default by an LGFV, some have struggled to make last-minute payments. The average LGFV bond maturity has declined by half a year from the beginning of the year as they increasingly sell debt maturing in a year or less, indicating that investors remain concerned about their long-term financial health.

But the refinancing bonds likely will reinforce Chinese investors' conviction that the Chinese government will always come to LGFVs' rescue when they are in trouble.

The special refinancing bonds are to “recharge faith in LGFVs,” said Zhao Guojun, credit analysis director at Wanlian Securities.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.