Q2 Results Live Updates: Earnings In Focus

We come to an end of the first day of September quarter earnings, kicked off by IT giant TCS. Results in focus on Friday include Elecon Engineering Company, Waaree Renewable Technologies and more.

See you tomorrow!

(This live blog has ended).

Q2 Business Updates Live: Gujarat Pipavav Container Cargo Down, Liquid Cargo Up

Gujarat Pipavav Q2 Business Update (YoY)

Containers cargo volume handled down 8% at 1.64 lakh TEUs

Dry bulk cargo volume at 1.05 MMT

Liquid cargo volume handled up 15% at 0.38 MMT

Source: Exchange filing

Q2 Business Updates Live: Mahindra & Mahindra Export Volume Up 44%

Mahindra & Mahindra Q2 Business Update (YoY)

Total Production Volume up 24.4% at 99,758 units

Total Sales Volume up 14% at 97,744 units

Total Export Volume up 44% at 4,458 units

Source: Exchange filing

TCS Q2 Results Live Updates: On H-1B Visas

Localisation efforts continue in the US, with only about 500 associates currently working there on H1B visas

TCS said its business model remains adaptable to potential changes in US immigration policy

TCS Q2 Results Live Updates: Project Deferrals Reduced

Project deferral in Q2 have reduced over Q1

Capex for data centre will be from co & partners

Co to have uniformed capex for data centres

Recovery has taken place for cyber security issue & co expects projects to ramp up in coming months

Investment in data centre aligns and forms group synergies for Tata group

Source: Con Call

TCS Q2 Results Live Updates: Significant Demand For AI In BFSI

Gen AI & Agentic AI are power full tool to deal with tech debts

Significant demand for AI seen in BFSI

FY26 growth in international business to be better than FY25

Wage hike implication on margins were for one month in Q2

Q3 to have higher impact on margins

Source: Con Call

TCS Q2 Results Live Updates: Confident Of H2 Performance

Chief Human Resources Officer Sudeep Kunnumal:

Expects to achieve 1 GW in 5-7 years

Investment in GW capacity will be a combination of equity & debt

Co hoping to sell it to deep tech cos and other players

Macros have not changed much

Co confident to do better in H2 than H1

Source: Con Call

TCS Q2 Results Live Updates: Wage Hike For 80% Employees

Chief Human Resources Officer Sudeep Kunnumal:

Wage hike for 80% employees in Q2

Co has released 1% of middle level employees

Over 500 associates have travelled to US on H1B visa

Severance package better than industry standard

Source: Con Call

TCS Q2 Results Live Updates: Aims To Become Largest AI Company

Chief Operating Officer Aarthi Subramanian:

Co wants to become world's largest AI company

Co continue to focus on internal transformation

Cyber sec update: Co working closely with clients, no compromises in TCS system

Source: Con Call

TCS Q2 Results Live Updates: Focus On AI Infrastructure

Deal wins were a mix of client consolidation and mega deals

Focus on making AI real for clients

Focus on AI infrastructure continues

Source: Con Call

TCS Q2 Results Live Updates: Deal Pipeline Remains Strong

BFSI total contract value at $3.2 billion

Deal pipeline continues to remain strong

FY26 to be better than FY25

Company sees tight control over client spends

Source: Con Call

TCS Q2 Results Live Updates: Consumer Business Only Sectotal Laggard

India continues to show strong growth

All sectors have done well apart from consumer business

Source: Con Call

TCS Q2 Results Live Updates: Geographical Growth Highlights

The Indian market contracted by 33.3% YoY. However, on a sequential basis, it grew by 4% The Middle East and African market grew by 5.9% QoQ and 12.7% YoY. The North American market reported a mild growth of 0.8% QoQ, but shrank 0.1% YoY in CC terms.

Latin America, grew 0.3% QoQ and 1.8% YoY. In Europe, the UK market shrank by 1.4% QoQ and 1.9% YoY. The continental Europe market reported a growth of 1.4% QoQ in the Sept. quarter but shrank 3% YoY.

TCS Q2 Results Live Updates: Attrition Not Revealed

In an unusual move, the information technology services giant did not announce its quarterly attrition rate and total headcount figures in its Q2 results.

TCS Q2 Results Live Updates: Five Key Highlights

From an interim dividend of Rs 11 to a rise in total contract value, click the link below to dive into highlights from the IT major's September quarter earnings.

Q2 Business Update Live: ICICI Prudential New Business Premium Rises

ICICI Prudential Q2 Business Update (YoY)

New business premium up 6.1% at Rs 1,761 crore

Annualised premium equivalent down 1.1% at Rs 871 crore

Source: Exchange Filing

Tata Elxsi Q2 Results Live Updates: Catch All Updates

Dive deeper into Tata Elxsi's Q2 financial performance here.

Q2 Results Live Updates: Tata Elxsi Profit Meets Estimates

Tata Elxsi Q2 Results Key Highlights (Consolidated, QoQ)

Revenue up 2.9% to Rs 918.10 crore versus Rs 892.09 crore

Net Profit up 7% to Rs 154.81 crore versus Rs 144.36 crore

Ebit up 5% to Rs 169.87 crore versus Rs 162.43 crore

Margin at 18.5% versus 18.2%

TCS Q2 Results Live Updates: To Establish AI Data Centres

TCS approves incorporation of wholly-owned arm in India to establish multiple AI and sovereign data centres, after posting its Q2 results.

Source: Exchange filing

TCS Q2 Results Live Updates: Declares Rs 11 Dividend

Tata Consultancy Services announced its second interim dividend of Rs 11.

The dividend will have a face value of Rs 1. It will be paid to the shareholders on Nov. 4. The record date for determining those who will be eligible for the dividend payouts is Oct. 15, the filing said.

TCS Q2 Results Live Updates: Press Conference Cancelled On Clash With Ratan Tata's Death Anniversary

The company has confirmed that the cancellation was due to the date coinciding with the death anniversary of Ratan Tata, the former Chairman of Tata Sons and a towering figure in the Tata Group. While the press event has been scrapped, the company's analyst call, where the financial performance and management commentary are shared is set to proceed as planned.

TCS Q2 Results Live Updates: Dive Deeper

Take a deeper look at the financial performance of the IT giant in the second quarter by clicking the link below.

TCS Q2 Results Live Updates: Key Highlights

Large deal TCV at $10 billion

On a journey to become the world's largest AI-led tech services company

Achieved good growth momentum across all verticals in Q2

International revenue grows 0.6% in constant currency terms (QoQ)

Board approves acquisition of ListEngage with deep capabilities in salesforce

Source: Press release

TCS Q2 Results Live Updates: Profit Beats Estimates

TCS Q2 Results Key Highlights (Consolidated, QoQ)

Revenue seen 3.7% higher at Rs 65,799.00 crore versus Rs 63,437 crore (Bloomberg Estimate: Rs 65,206 crore).

Profit seen 5% lower at Rs 12,075.00 crore versus Rs 12,760 crore (Bloomberg Estimate: Rs 12,568 crore).

EBIT seen 7% higher at 16,565 crore versus Rs 15,514 crore (Bloomberg Estimate: Rs 15,998 crore).

EBIT margin expanded at 25.2% versus 24.45% (Bloomberg Estimate: 24.53%).

TCS Q2 Results Live Updates: Nomura Price Target At Rs 3,300

Revenue is expected to decline 0.5% sequentially in constant currency, mainly due to a smaller contribution from BSNL.

Developed markets are expected to see modest growth.

EBIT margin is expected to remain largely flat, partly offset by the effect of salary hikes.

Deal wins are projected between $7 billion and $9 billion, excluding mega deals.

Analysts are monitoring restructuring impact, discretionary spending, and cost takeout projects.

TCS Q2 Results Live Updates: InCred Price Target At Rs 3,818

Constant-currency revenue could remain flat sequentially, supported by growth in energy, utilities, hi-tech and financial services.

Margin benefits from FX and restructuring may be offset by lower utilisation due to JLR project delays.

Key monitorables: deal pipeline conversion, performance in financial services, retail, and manufacturing verticals, and large deal ramp-ups.

TCS Q2 Results Live Updates: Jefferies Price Target At Rs 3,230

Revenue is expected to grow 0.4% QoQ in constant currency, led by international markets, partly offset by the BSNL ramp-down.

Margin seen improving slightly, supported by BSNL normalisation and rupee depreciation, partly offset by the wage hike.

Deal wins are expected between $7 billion and $9 billion.

Key focus areas: BFSI demand, restructuring impact, BSNL phase-two ramp-up, H1-B visa fee hike, AI adoption and JLR cyberattack implications.

TCS Q2 Results Live Updates: Goldman Sachs Target Price At Rs 3,310

Margin expected to remain largely stable quarter-on-quarter, aided by FX gains and top-line growth, partly offset by the September wage hike.

Commentary on H1-B visa policy and headcount will be closely watched.

Q2 growth is expected to be better than Q1 as BSNL ramp-down impact is now fully reflected in the base.

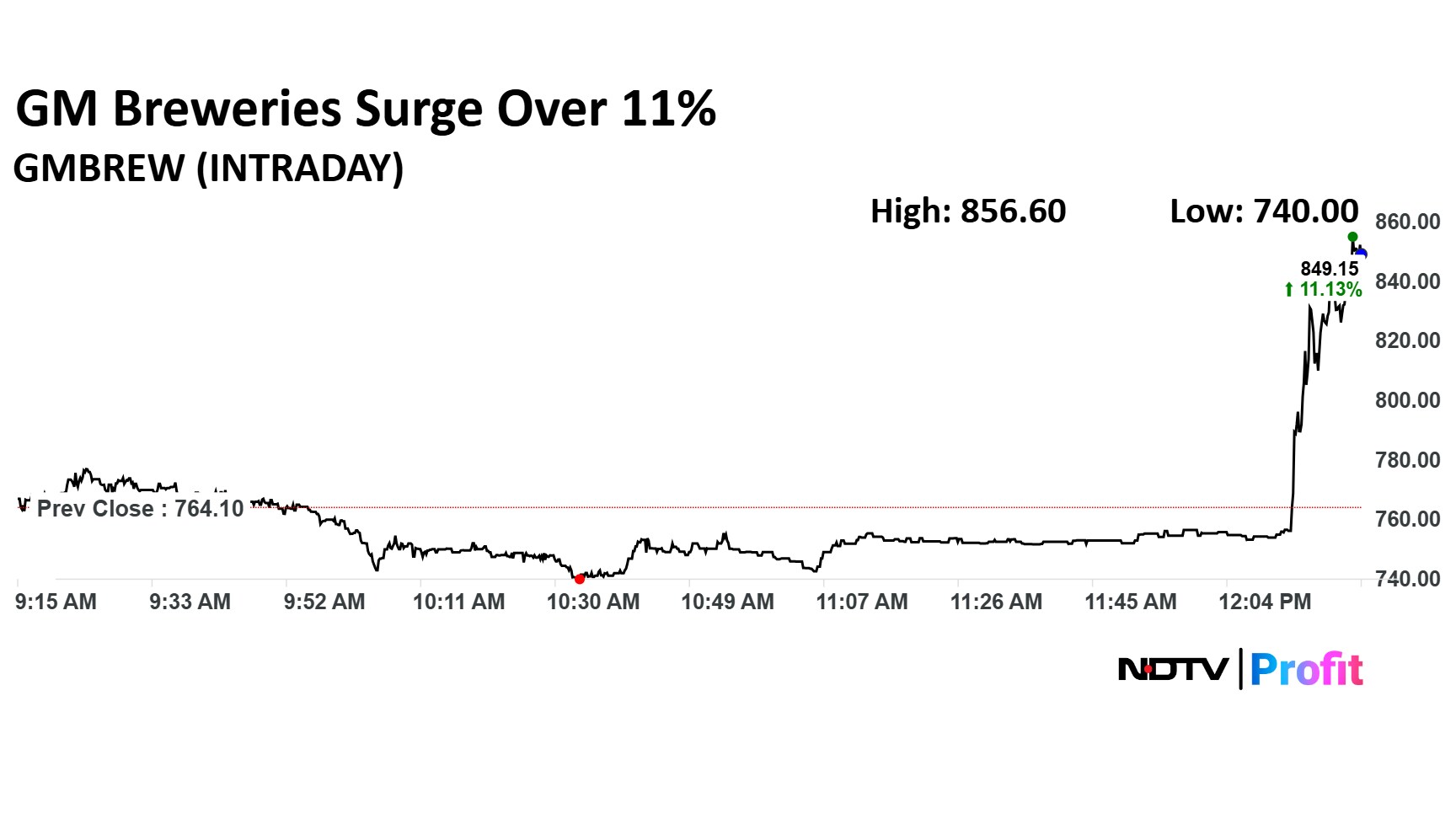

Q2 Results Live: GM Breweries Stock Surges 11%

The shares of GM Breweries surged over 11% after the company posted second quarter results. The scrip was trading at Rs 864 apiece on the NSE.

The shares of GM Breweries surged over 11% after the company posted second quarter results. The scrip was trading at Rs 864 apiece on the NSE.

Q2 Results Live: GM Breweries Net Profit Rises 61%

GM Breweries Q2 Highlights (YoY)

Revenue up 20.5% to Rs 181 crore versus Rs 149 crore

Net Profit up 61% to Rs 34.8 crore versus Rs 21.6 crore

Ebitda up 62% to Rs 45 crore versus Rs 27.78 crore

Margin at 24.9% versus 18.6%

Q2 Results Live Updates: Tata Elxsi Estimates (QoQ)

Revenue seen 3% higher at Rs 65,206 crore versus Rs 63,437 crore.

Profit seen 1% lower at Rs 12,568 crore versus Rs 12,760 crore.

EBIT seen 3% higher at 15,998 crore versus Rs 15,514 crore.

EBIT margin seen at 24.53% versus 24.45%.

In the Tier-2 basket, performance is expected to be uneven. While demand headwinds persist, margin resilience and BFSI recovery offer some optimism for the sector. With the rupee weakness providing near-term support, much of the Street’s attention this quarter will be on management commentary, especially around client budgets, pricing environment, and the pace of deal closures as the industry looks to set the tone for the second half of FY26.

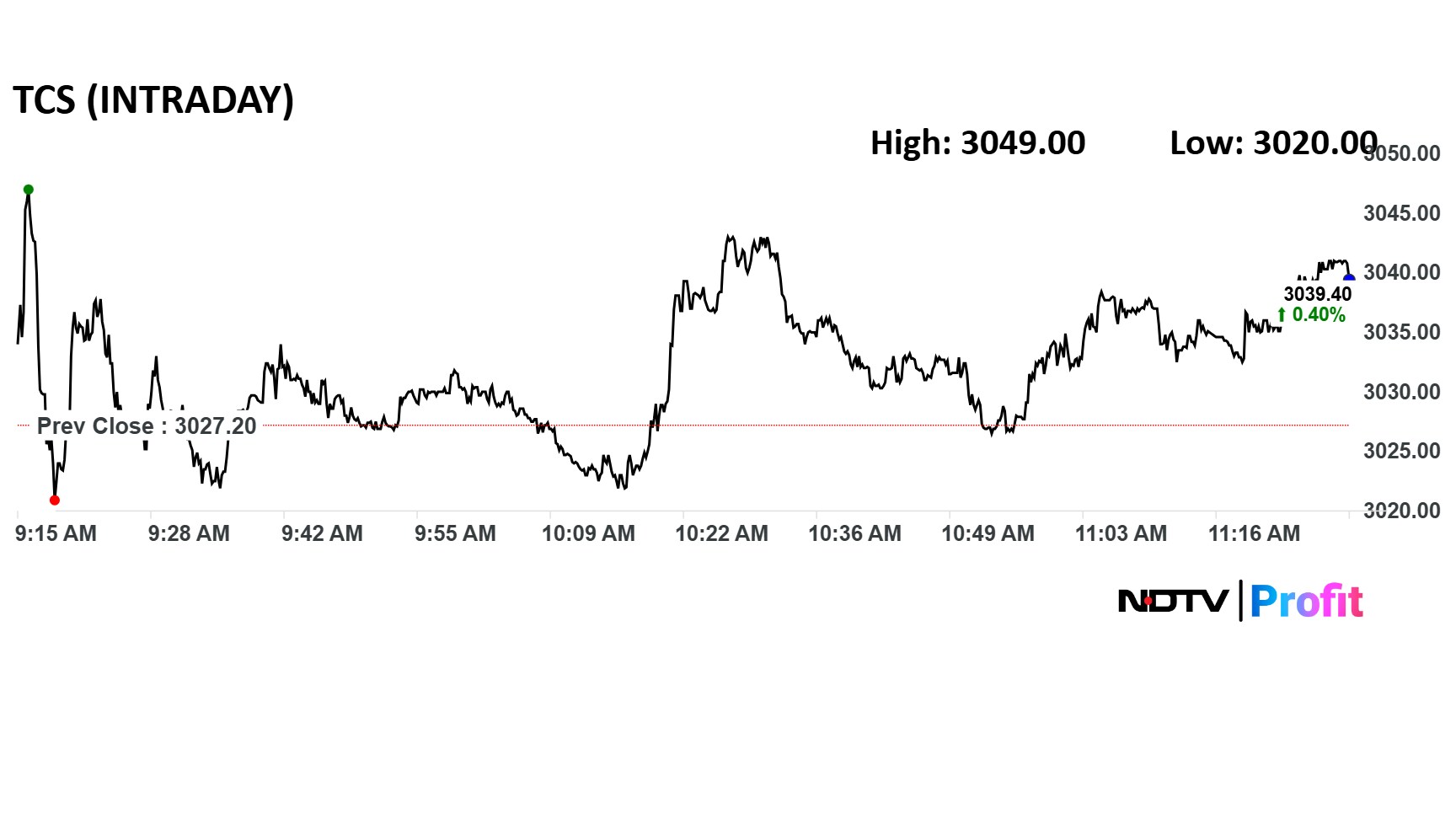

TCS Q2 Results Live Updates: Share Price Movement

Tata Consultancy Services Ltd. share price was steady during trade on Thursday, ahead of the second-quarter financial results. The stock rose as much as 0.7% intraday.

The Q2 results will be announced after market hours. The company has cancelled its scheduled press conference as the day coincides with the death anniversary of Ratan Tata, the former Chairman of Tata Sons and a towering figure in the Tata Group.

While the press event has been scrapped, the company's analyst call, where the financial performance and management commentary are shared, is set to proceed as planned.

Tata Consultancy Services Ltd. share price was steady during trade on Thursday, ahead of the second-quarter financial results. The stock rose as much as 0.7% intraday.

The Q2 results will be announced after market hours. The company has cancelled its scheduled press conference as the day coincides with the death anniversary of Ratan Tata, the former Chairman of Tata Sons and a towering figure in the Tata Group.

While the press event has been scrapped, the company's analyst call, where the financial performance and management commentary are shared, is set to proceed as planned.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.