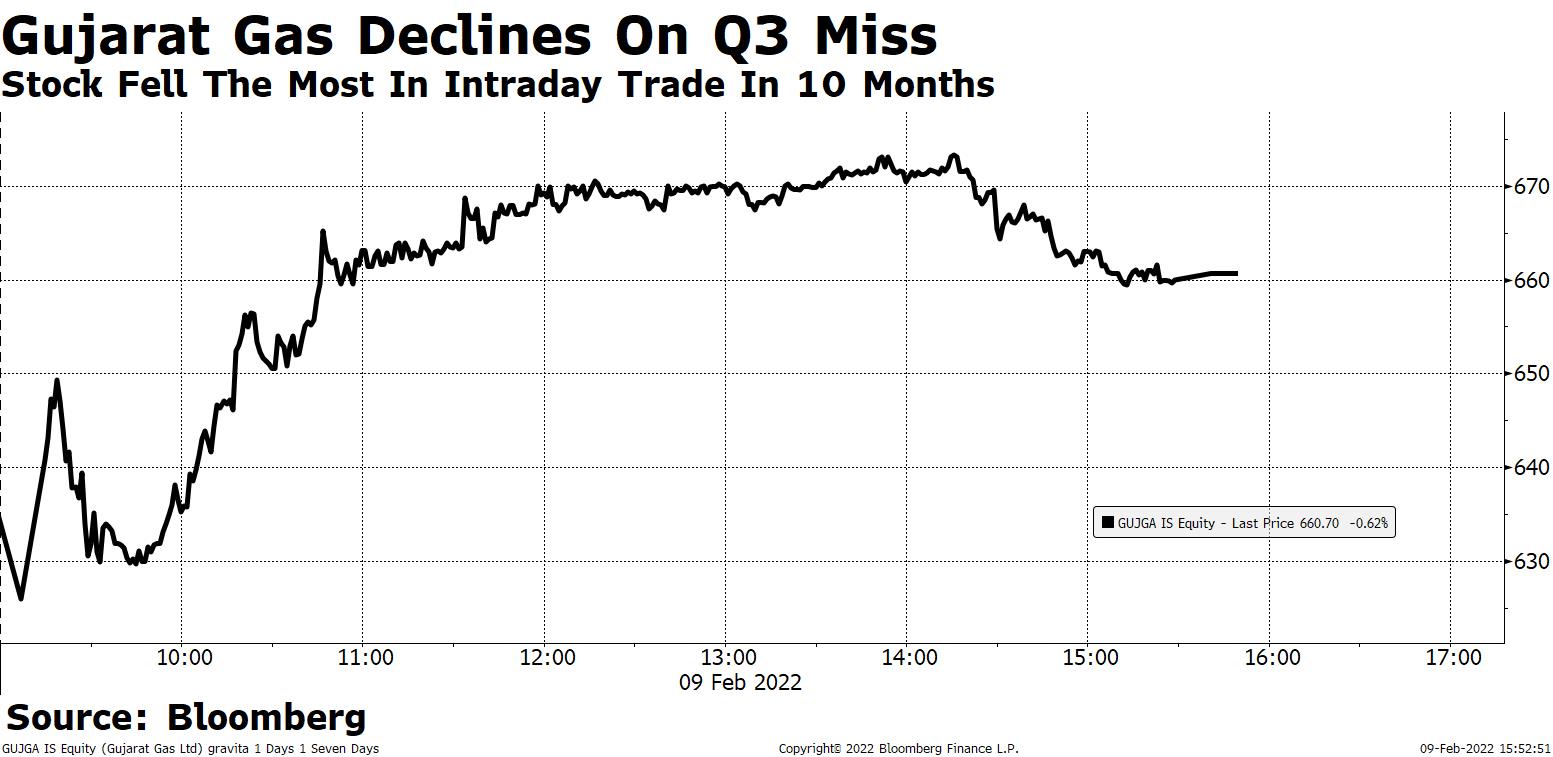

Shares of Gujarat Gas Ltd. fell the most in 10 months in intraday trade as analysts see a surge in spot LNG prices and dependence on the Morbi industrial cluster as short-term risks for the city gas distributor.

Analysts turned cautious as the supplier of piped gas missed profit estimates in the quarter ended December and saw its margin contract.

Q3 FY22 Highlights (Consolidated, YoY)

Revenue up 81% at Rs 5,241.16 crore, against the Bloomberg consensus estimate of Rs 3,830 crore.

Net profit down 69% at Rs 122.94 crore compared with the estimated Rs 168 crore.

Ebitda down 61% at Rs 237.49 crore.

Margin stood at 4.6% against 21.7%.

The volume growth prospects of Gujarat Gas, however, remain robust, analysts said.

Shares of the company dropped as much as 6% in intraday trade and closed with 0.62% losses on Wednesday. The stock also slipped below the 200-day moving average in intraday trade on high trading volume. Its trading volume was nearly five times the 30-day average at this time when markets closed.

Of the 31 analysts tracking Gujarat Gas, 19 recommend a 'buy' and six each suggest a 'hold' and a 'sell', according to Bloomberg data. The 12-month consensus price target implies an upside of 5.3%.

Here's what analysts have to say about Gujarat Gas...

Nirmal Bang

Downgrades to 'sell' from 'accumulate', cuts target price to Rs 544 from Rs 587—still an implied return of 14.83%.

Downgrade based on cloudy outlook for industrial PNG growth/margins based on buoyancy in global spot LNG prices and regulatory risk in PNG business.

Dependence on single industrial cluster like Morbi is a cause for concern.

LNG rally poses the highest risk to Gujarat Gas

Motilal Oswal

Maintains 'buy' with a target price of Rs 800—an implied return of 26.53%.

Abnormally high LNG price volatility impact margin.

Volume growth prospects remain robust with the addition of over 60 new industrial units.

Any underperformance in terms of Ebitda/standard cubic metre or volume growth could pose major risk for the company.

Constant rise in spot LNG pries resulted in 100 units shutting down in Morbi in January 2022.

Prabhudas Lilladher

Maintains 'buy' with a target price at Rs 764—an implied return of 14.91%.

Q3 results were impacted by a sharp jump in spot gas prices.

Expects margins to recover from Q3 lows, as spot LNG prices ease.

Sharp jump in spot LNG prices remains a near-term worry.

Any resolution in Ukraine crisis will ease gas prices which will support margins.

Jefferies

Maintains 'buy' but cuts target price to Rs 830 from Rs 860—still an implied return of 31.75%.

Sharp miss on Ebitda margin led by higher realised spot LNG cost.

The company still remains the preferred pick within India city gas distributors given higher longer-term growth potential, less mature area portfolio than peers, strong upside optionality in volumes, higher scalability and much lower risk from electric vehicle disruption than peers.

Spike in spot LNG could be near-term overhang, but the pricing power added to comfort on the margin front.

Underlying volume drivers remains intact.

Cuts FY22E, FY23E and FY24 EPS estimates by 10%, 5%, 5%, respectively.

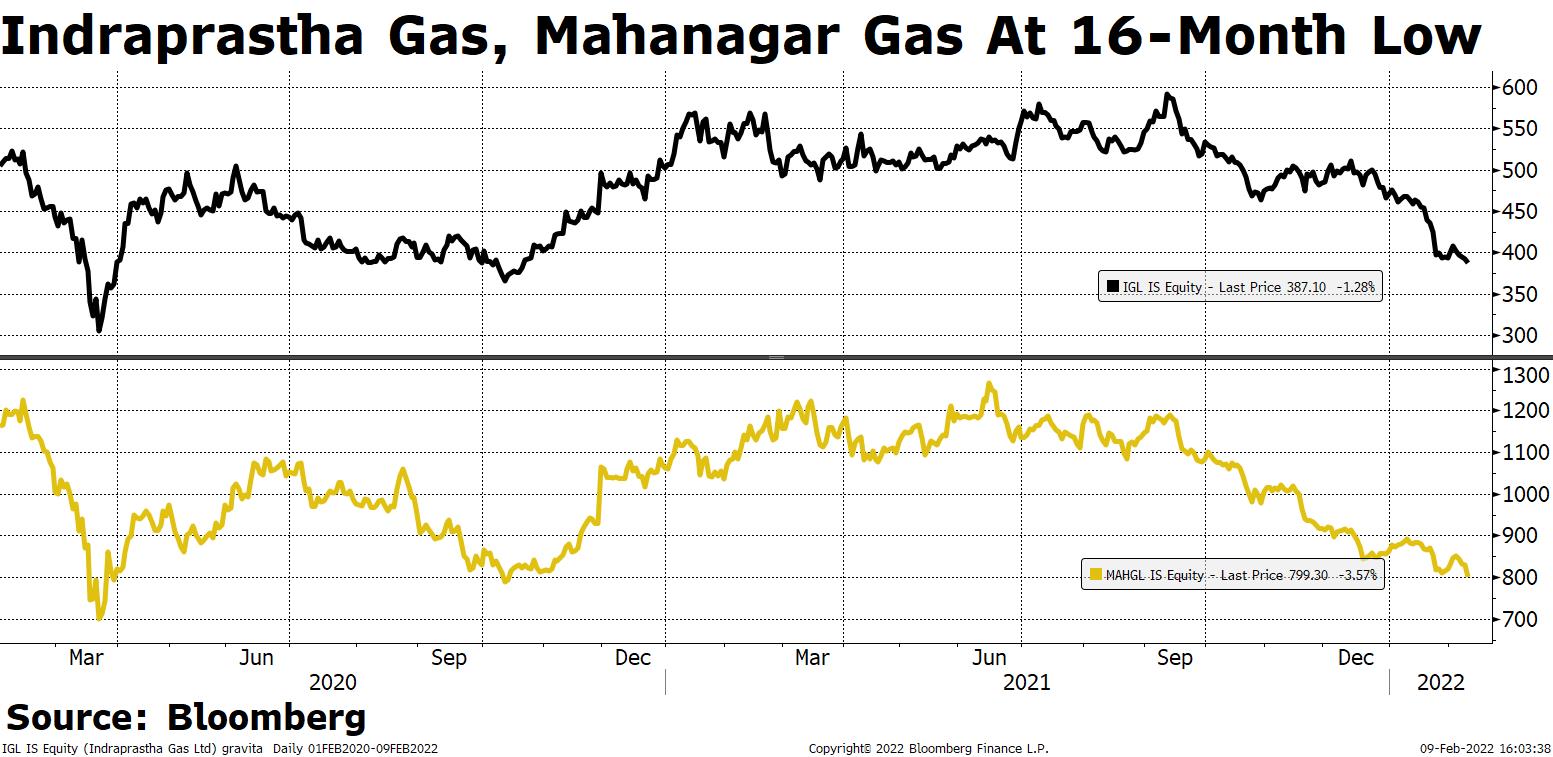

Peers Indraprastha Gas Ltd. and Mahanagar Gas Ltd., too, saw selling pressure after the third-quarter results. The stocks slumped to their 52-week lows.

Mahanagar Gas' net income missed estimates. Analysts cited volume growth as a key concern due to limited scope for CNG station additions in Mumbai. But they expect its margin to recover in the medium term.

Indraprastha Gas' net profit beat estimates. Analysts flagged long-term margin risk due to CNG vehicle addition on EV thrust and risk of volatility in earnings because of LNG price.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.