Scan to Download

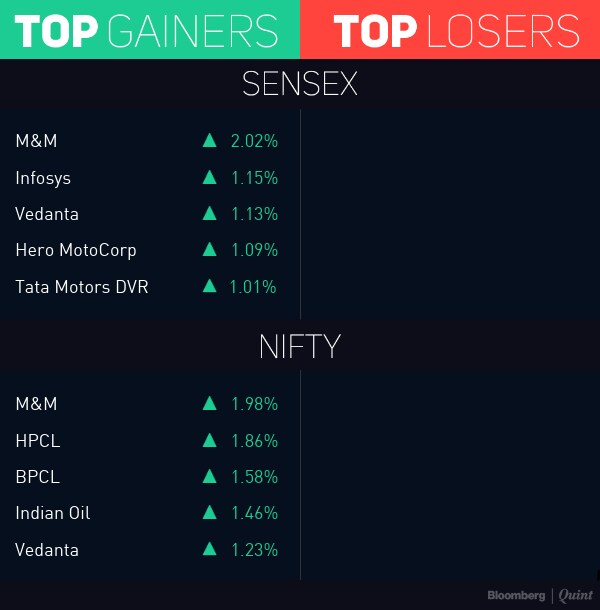

The e-commerce website operator was the top gainer in the Nifty 500 Index. The stock rose as much as 21 percent, the most in over a month, to Rs 53.

Midcaps continue to remain at disadvantage at this point of time and I would advise to stick to large caps, Ajay Srivastava of Dimensions Corporate Finance told BloombergQuint.

Key highlights of the conversation:

Markets are adjusting to lower level of fund flows and correction is done for markets and economy is set to grow, Raamdeo Agrawal of Motilal Oswal told BloombergQuint in an interview.

Key highlights of the conversation:

(As Reported on Nov. 6)

Aditya Birla Capital (Consolidated Q2 YoY)

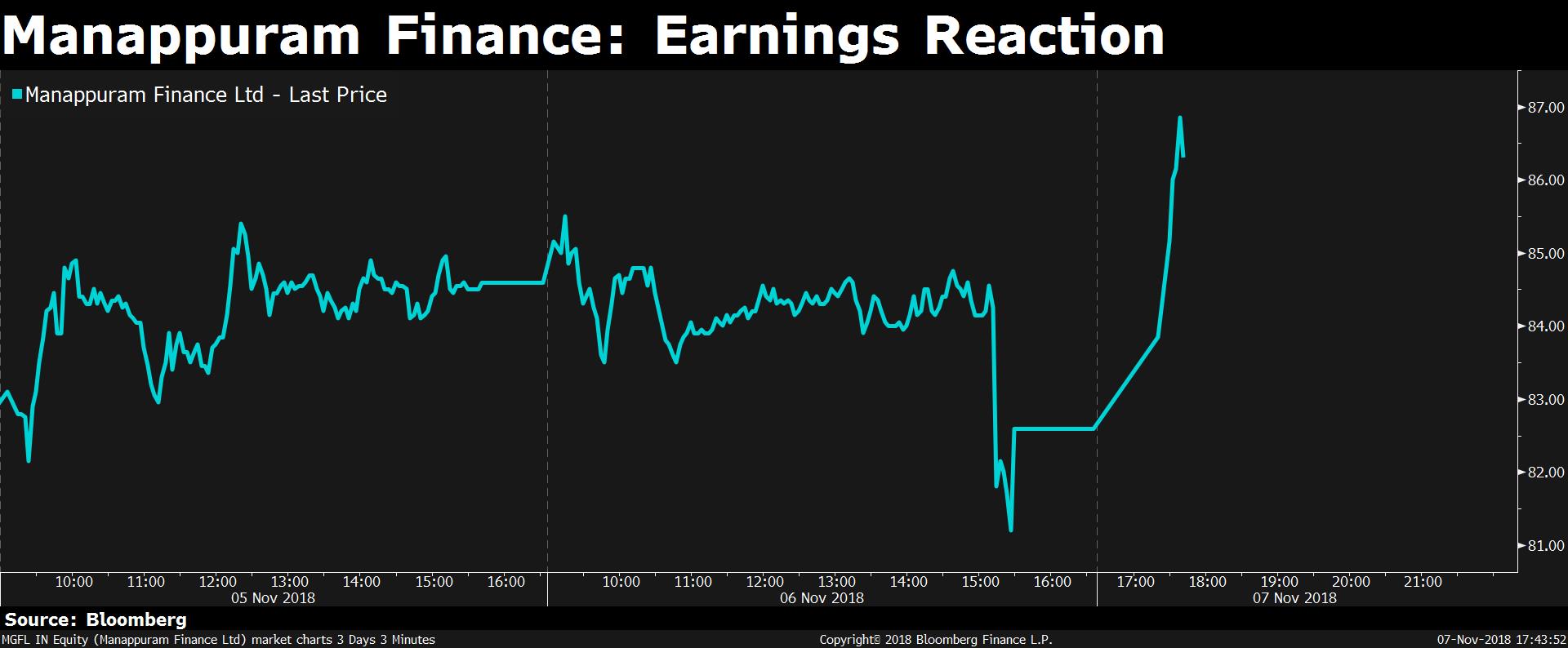

Mannapuram Finance (Consolidated Q2 YoY)

Camlin Fine Sciences (Consolidated Q2 YoY)

The dollar retreated, U.S. equity futures jumped and Treasuries climbed as investors mulled the fallout from American midterm elections. European stocks rallied and Asian shares were mixed.

With Democrats winning the House of Representatives majority and Republicans clinching control of the Senate, President Donald Trump’s party loses full control of Congress. The results dim chances for any major fiscal initiative from the administration that might have pushed yields higher and strengthened the greenback.

Moves

Stock Prices Are Set For Cheer In The New Year, Says Morgan Stanley’s Ridham Desai

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.