A rebound of beaten-down tech giants lifted the stock market after a mixed jobs report, with traders now gearing up for Federal Reserve Chair Jerome Powell's remarks for more clues on the rates outlook.

Equities wiped out losses, with Nvidia Corp. leading gains in megacaps. Broadcom Inc. jumped after the chip supplier for Apple Inc. and other big tech companies gave an upbeat forecast, reassuring investors that spending on artificial intelligence computing remains healthy. Bonds rose as data underscored a labor market that continues to moderate.

US job growth steadied last month while the unemployment rate rose — a mixed snapshot of a market hanging on the balance of quickly changing government policy. Nonfarm payrolls increased 151,000 in February after a downward revision to the prior month. The unemployment rate rose to 4.1%.

Traders continue to anticipate three quarter-point Fed rate cuts over the seven remaining policy meetings this year. The contracts assign slightly less than even odds that the first one comes in May.

Wall Street's Reaction

Charlie Ripley at Allianz Investment Management: Today's employment report highlighted the obvious in that the US economy is indeed slowing on the margin, but more importantly, we are not seeing the economy fall off a cliff. Overall, this report is a sigh of relief for the Fed as they can continue to sit on the sidelines for the next couple meetings as they assess the potential inflation impacts resulting from US tariff policy over the coming months.

Scott Wren at Wells Fargo Investment Institute: This report does not change our view that the labor market is likely to gradually decelerate in coming month/quarters and continue to look for the unemployment rate to move higher by the end of this year.This report tells the Fed that they still need to be careful as sticky housing/shelter/wage data shows it won't be easy to engineer meaningfully lower inflation from current levels in the near term.Expect the near-term financial market volatility to continue with many unknowns out there.

Josh Jamner at ClearBridge Investments: The solid February jobs report shows that the economy remains healthy, but fears of what could come next are likely to overshadow the positive news from today's release. Investors are likely to temper their reactions to this morning's data due to the perception of it being “already stale” given the rapid policy shifts coming from DC.

Gina Bolvin at Bolvin Wealth Management Group: We were expecting the unemployment rate to tick up this year. The markets should breathe a sigh of relief that there wasn't a shock in either direction and the report was a mixed bag. The takeaway is that wage data declined which is disinflationary.

Bryce Doty at Sit Invest: Essentially this report provides zero clarity for bond investors. You can argue the Fed will keep rates high or you could say this report means they may need to cut sooner than previously expected.

Jack McIntyre at Brandywine Global: The best way to describe the February US employment report was that it was one of those rare Goldilocks-type of economic reports. There's something for everyone. There is a fair chance that the February report is one of the strongest of the year. The report supports our investment theme that 2025 will indeed be the year of a weak dollar, and non-USD assets will continue to outperform.

Bret Kenwell at eToro: Given the headlines around federal employment and worries about the economy, today's jobs report was a huge focus for investors. It didn't beat economists' expectations, but there's a wonder if a better-than-worst-case outcome will be enough to trigger a relief rally on Wall Street. While the rallies have been short-lived in recent trading, investors are wondering if stocks can string together a few positive sessions in the form of a relief rally. But until there's more clarity around the current trade war and reassurance around the economy, a “risk-off” mood can linger on Wall Street.

Glen Smith at GDS Wealth Management: Investors are starting to worry about a noticeable deceleration in first quarter GDP, which is set to be released at the end of April, and that is contributing to the past few weeks of stock market volatility.Friday's jobs report may change the calculus for the Federal Reserve's plans on interest rates this year, and it's possible that we see the next rate cut come as soon as June. Federal Reserve Chair Jerome Powell is speaking on Friday afternoon, and investors will be looking for his reaction to the recent round of economic data and the market's broader tariff fears.The stock market is moving in lockstep with tariff headlines, and that is likely to keep volatility very elevated for the foreseeable future, as the market does not like uncertainty. While we expect the market to find its footing and recover from the tariff-driven selloff, investors should brace for continued choppiness until these uncertainties clear.

Byron Anderson at Laffer Tengler Investments: We are not putting much stock in the jobs report at the moment. Today's data was mixed at best, but we still have no clarity on the economy moving forward. Markets, businesses, and consumers do not like uncertainty and that means increased volatility.

David Russell at TradeStation: The jobs data shows moderating growth and wage pressures. That would normally be welcome as dovish news. However, investors see clouds on the horizon. This could be the calm before the storm of much weaker employment. Tariffs threaten jobs because they threaten supply chains and profits. Uncertainty is in a bull market.

Michael Kantrowitz at Piper Sandler & Co.: This is a perfect report for stocks today. It provides reason for a short-term bounce in that it wasn't weak, and the unemployment rate rose with a lower participation rate, which opens the door a bit more for the Fed to get incrementally more dovish. Good news all around and a short-term catalyst for stocks. It doesn't solve the primary issue but provides relief, for now. Consensus seems to want to fade every rally, so let's hope this can hold.

George Mateyo at Key Wealth: No news is… no news. And while investors may justly be inclined to breathe a sigh of relief following today's jobs report, they shouldn't exhale for too long as the real news may soon be known.After a period of head-spinning volatility, today's employment report was very much an “in-line” report, as several key metrics matched (or closely matched) forecasts. This should provide some much-needed calm to the markets.

Florian Ielpo at Lombard Odier Investment Managers: Markets largely treated the news as a non-event. The numbers, slightly below expectations especially considering the revisions, were not the significant mishap Wall Street feared. It's important to remember that this report is consistent with the narrative of slower economic growth in the US, but not indicative of a recession at this point. This allows the current rotation in the markets to continue and should help cap the recent rise in yields.

Jamie Cox at Harris Financial Group: This is one way to get the Fed to cut rates. The transition from a reliance on government propping up the economy to allowing the market to stand on its own feet will be a little bumpy. While strong, the jobs market will slow considerably with government in cutting mode.

Seema Shah at Principal Asset Management: After the headlines of recent days, there were fears that today's jobs report would reveal some deeply unsettling news around the health of the labor market. If anything, the report is reassuringly in line with expectations, showing payrolls growth only modestly weaker than in recent months. Yet, while the worst fears were not met, the report does confirm that the labor market is cooling and that it may require some assistance from the Fed in the coming months. Furthermore, with no shortage of headwinds confronting the U.S. economy, the softening trend is likely to persist and may potentially deepen given the toxic combination of federal government layoffs, public spending cuts, and tariff uncertainty related inertia.

Chris Zaccarelli at Northlight Asset Management: Markets breathed a sigh of relief this morning that the jobs data wasn't worse than expected. It was largely in line and although the unemployment rate ticked up slightly from 4.0% to 4.1%, that's still a low number from a historical perspective.In the day-to-day barrage of headlines – such as tariffs repeatedly being imposed and then removed – it's easy to get lost in them and forget what ultimately matters. The market cares about employment, productivity, and profits. Inflation can become an issue for profits and if consumers reduce their purchasing, goods' unit sales drop, and layoffs begin then it can create a downward spiral for the economy, but so far that hasn't happened.We've felt whipsawed by the on-again off-again tariff news, but we've largely held the same course as we began 2025 with: very cautious, risk-off and concerned about valuations and concentration. We've been counseling clients since the end of last year that 2025 was likely to be a volatile year because of policy uncertainty and so far, that's exactly what we've seen.

Richard Flynn at Charles Schwab UK: This disappointing news comes at a time when the market is in need of a pick-me-up. With investors already concerned about a growth slow down, we will likely see greater sensitivity to economic data in the coming days and weeks. As a result, this report could further weigh on the market after a forlorn February.

Asian stocks followed US equities lower as continual shifts in US President Donald Trump's approach to tariffs on trade partners whipped up market uncertainty and dented confidence in the economic outlook.

Shares in Australia and Japan tumbled more than 1.5% each while a gauge of Chinese stocks in Hong Kong gained to the highest level since November 2021. An index of the dollar fell for a fifth session, its longest losing streak in almost a year. Bitcoin fell as details of a US strategic reserve underwhelmed.

Traders pointed to uncertainty over Trump's tariffs. US stocks failed to stage a rebound even after a decision by Trump to delay levies on Mexican and Canadian goods covered by the North American trade deal, underscoring the fragile appetite for risk. Financial markets have whipsawed this week as investors deal with geopolitical uncertainty and conflicting signals from the US about the levies.

“Confusion reigns around the Trump Administration policy agenda,” said Chris Weston, head of research for Pepperstone Group. “While there are few signs of panic, funds and fast-money accounts cut equity risk.”

Wall Street strategists have been debating whether the Trump administration would be swayed on its tariff plans by a decline in equities. The thinking being that Trump will ditch policies if the stock market — which he touts as a report card — drops and rattles investors. Various firms even mapped out how much pain Trump could tolerate in the S&P 500 Index before retreating. That index level became known as “the Trump put,” in reference to a put option.

So far, Trump has given little indication he'll change course. The president downplayed the reaction to the latest developments, saying “I'm not even looking at the market.” That followed his comments to Congress earlier this week that levies will cause “a little disturbance, but we're OK with that. It won't be much.”

On Thursday, Trump delayed levies on goods covered by the North American trade deal from the two countries until April 2. Later comments from Treasury Secretary Scott Bessent all but confirmed tariffs will be coming. Bessent rejected the idea that tariff hikes will ignite a new wave of inflation, and suggested that the Federal Reserve ought to view them as having a one-time impact.

European stocks have advanced almost 10% this year, as rate cuts and Germany's plan to raise defense spending boost the market. Meanwhile, a gauge of Chinese stocks listed in Hong Kong has surged almost 23% so far this year on optimism over the nation's artificial-intelligence adoption drive and expected stimulus from Beijing.

Bitcoin fell after details of a US cryptocurrency reserve emerged and indicated the government will use digital assets forfeited as part of criminal or civil proceedings.

US equity-index futures rose Friday after US chipmaker Broadcom Inc.'s upbeat revenue forecast reassured investors that spending on artificial-intelligence computing remained ongoing, pushing its shares around 13% higher in after-market trading.

The post-hours rally spread to tech companies that were among the hardest hit on Thursday. Nvidia Corp. and Marvell Technology Inc., which plunged during the main session as its outlook disappointed investors, rose after the closing bell.

Treasuries were slightly higher Friday after a muted session on Thursday. The Mexican peso and the Canadian dollar rose on news of the potential tariff reprieve. Australian and New Zealand yields fell early Friday.

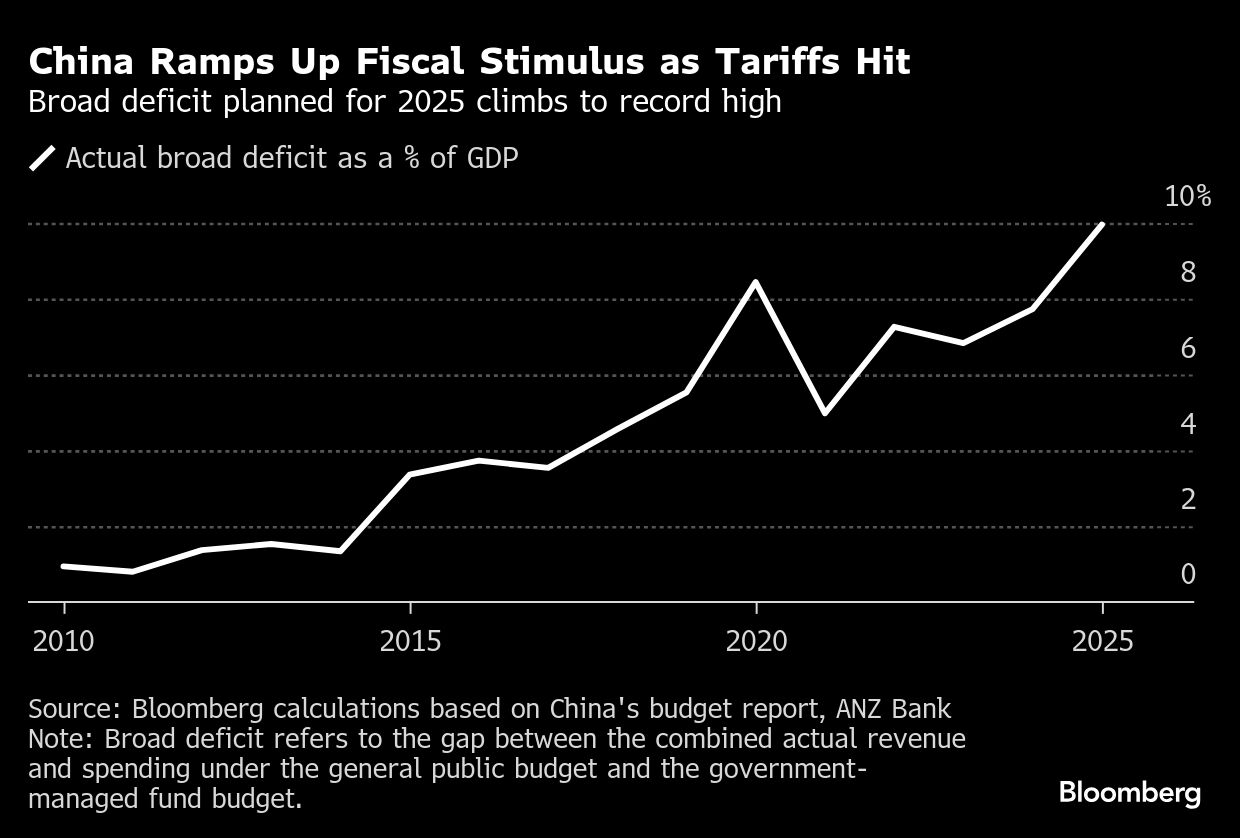

In Asia, China's central government has ample fiscal policy tools and space to respond to possible domestic and external challenges, Finance Minister Lan Fo'an said Thursday on the sidelines of the annual legislative session. The People's Bank of China will implement a moderately loose monetary policy, Governor Pan Gongsheng said, repeating an earlier pledge to cut interest rates and lower the reserve requirement ratio for lenders at “an appropriate time.”

China's exports reached a record so far this year as higher US tariffs, and the threat of more to come, drove frontloading of shipments.

Upcoming US nonfarm payrolls data on Friday may help traders identify the path ahead for interest rates, as they grapple with the impact of rocky geopolitics, the impact of tariffs on global growth and the outlook for inflation.

Friday's report from the Bureau of Labor Statistics will provide an update for Fed officials about momentum in the labor market that's been the key support — at least until January — of household spending and the economy.

Fed Chair Jerome Powell is slated to speak at a monetary policy forum Friday afternoon. Policymakers next meet March 18-19 and they're expected to hold interest rates steady as they gauge the labor market and inflation trends as well as recent government policy shifts.

Meanwhile, Fed Reserve Governor Christopher Waller said he wouldn't support lowering interest rates in March, but sees room to cut two, or possibly three, times this year.

“If the labor market, everything, seems to be holding, then you can just kind of keep an eye on inflation,” Waller said Thursday at the Wall Street Journal CFO Network Summit. “If you think it's moving back towards target, you can start lowering rates. I wouldn't say at the next meeting, but could certainly see going forward.”

In commodities, oil was on track for the biggest weekly decline since October while gold was on track for a gain as traders sought havens.

Key events this week:

Eurozone GDP, Friday

US jobs report, Friday

Fed Chair Jerome Powell gives keynote speech at an event in New York hosted by University of Chicago Booth School of Business, Friday

Fed's John Williams, Michelle Bowman and Adriana Kugler speak, Friday

Some of the main moves in markets:

Stocks

The S&P 500 rose 0.4% as of 9:48 a.m. New York time

The Nasdaq 100 rose 0.5%

The Dow Jones Industrial Average rose 0.3%

The Stoxx Europe 600 fell 0.5%

The MSCI World Index rose 0.1%

Currencies

The Bloomberg Dollar Spot Index fell 0.2%

The euro rose 0.7% to $1.0856

The British pound rose 0.3% to $1.2922

The Japanese yen rose 0.3% to 147.57 per dollar

Cryptocurrencies

Bitcoin rose 1.2% to $90,960.82

Ether rose 1.9% to $2,255.8

Bonds

The yield on 10-year Treasuries declined two basis points to 4.26%

Germany's 10-year yield declined two basis points to 2.81%

Britain's 10-year yield declined two basis points to 4.64%

Commodities

West Texas Intermediate crude rose 2.4% to $67.96 a barrel

Spot gold rose 0.3% to $2,920.68 an ounce

This story was produced with the assistance of Bloomberg Automation. © 2025 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.