Scan to Download

Buyers and sellers were not immediately known

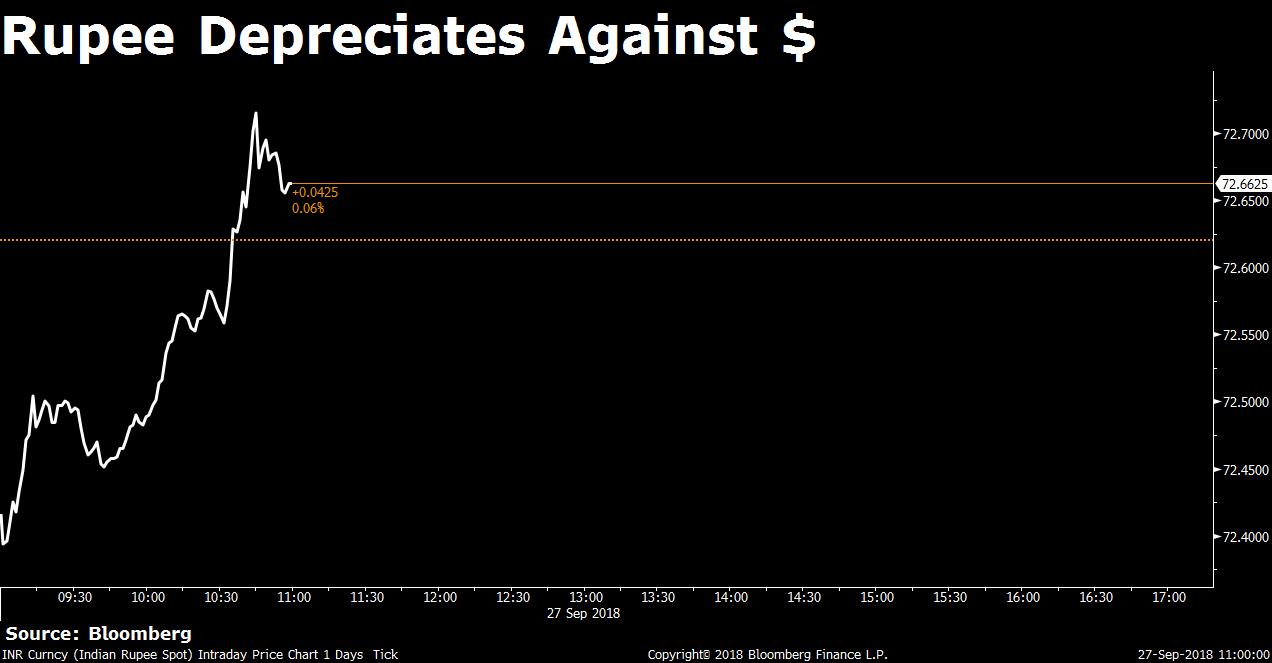

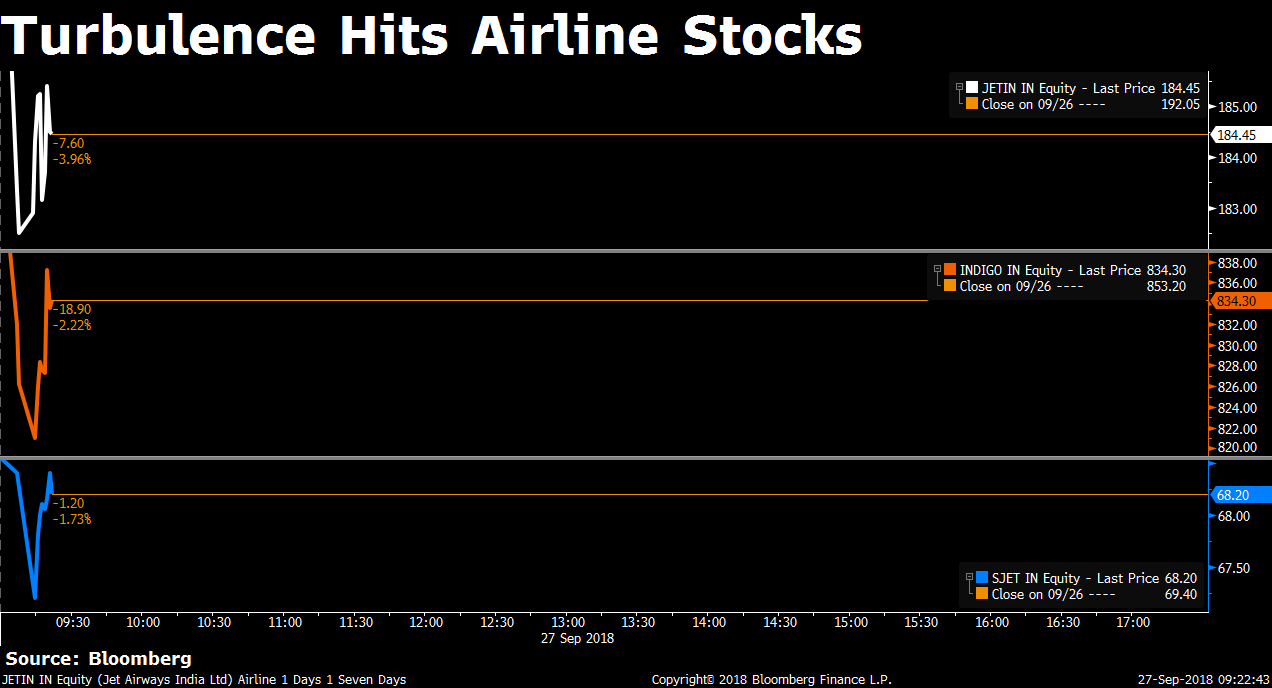

Source: Bloomberg

Shares of the Delhi-based automotive air-conditioning systems maker slumped after its board approved issuing 52.47 lakh equity shares to Denso Corporation, Japan on preferential basis.

Indian equity benchmarks extended decline led by losses in financials and private sector lenders on the F&O expiry day.

The Sensex fell 0.5 percent or 185 points to 36,356 and the Nifty 50 Index declined 0.6 percent or 68 points to 10,987.

Sixteen of 19 sector gauges compiled by BSE were trading lower led by the S&P BSE Finance Index's 1.55 percent decline.

Top Five Nifty Losers

Top Five Nifty Gainers

Click here for more stock market statistics

Shares of non-banking finance companies plunged led by losses in Can Fin Homes and Indiabulls Housing Finance.

Click here to see the complete options chain

Shares of footwear makers advanced after the government hiked import duty on shoes from 20 percent to 25 percent.

Shares of the air conditioner, washing machine and refrigerator makers fell after the government hiked import duty on a range of products including air conditioners, refrigerators, compressors and washing machines.

Hike in duties on compressor by 2.5 percent is a negative since most of the compressors are bought from China with little domestic manufacturing, Motilal Oswal said in a note.

Indian equity benchmarks swung between gains and losses ahead of the derivative expiry for the month of September.

The S&P BSE Sensex rose 31 points to 36,572 and the NSE Nifty 50 Index advanced 12 points or 0.1 percent to 11,067.

Fifteen of 19 sector gauges compiled by BSE were trading higher led by the S&P BSE Utilities Index's 0.8 percent gain. On the other hand, the S&P BSE Telecom Index was top loser, down 0.3 percent.

CLSA

Goldman Sachs

Morgan Stanley

BofAML

Credit Suisse on Consumer Staples

Morgan Stanley on Havells India

Goldman Sachs on Asian Paints

HSBC on SpiceJet

Apollo Hospitals Enterprise

Also Read: State-Run Shipbuilder Garden Reach’s IPO Fails To Attract Investors

Also Read: Aavas Financiers’ IPO: Here’s All You Need To Know

Government Hikes Basic Customs Duty On 19 Items To Curb Imports

Petrol/diesel prices hiked across major cities. ⛽️ pic.twitter.com/ixSh8xUmZW

— BloombergQuint (@BloombergQuint) September 27, 2018

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.