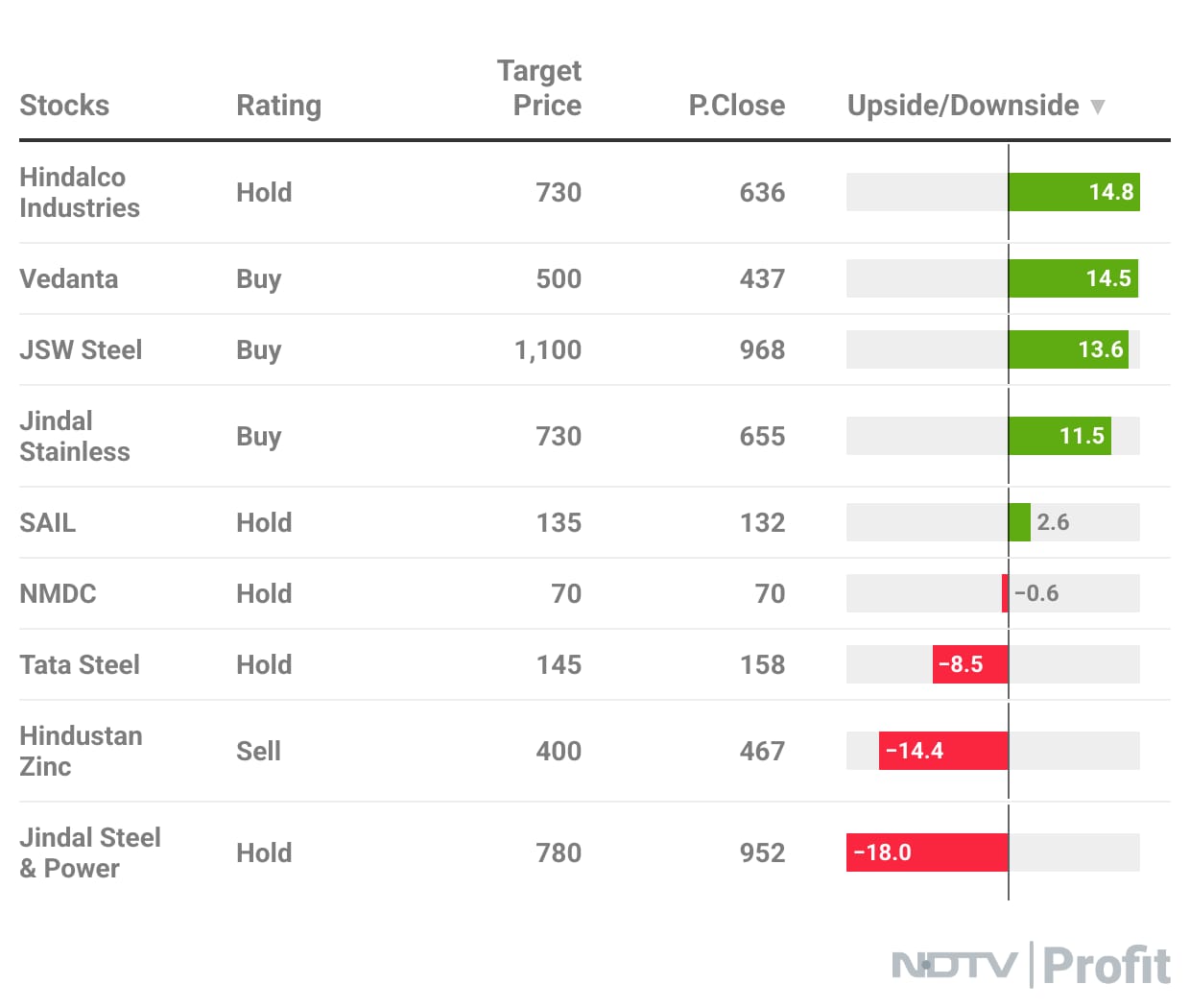

Investec reiterated its preference for JSW Steel Ltd. in ferrous, and Vedanta Ltd. in non-ferrous space. The brokerage downgraded Hindalco Industries Ltd. to 'hold'. For ferrous, Investec expects cost tailwinds to continue in the fourth quarter, and in the non-ferrous segment it's likely to be a mixed-bag growth.

There is low probability of liquidation of Bhushan Power & Steel, according to Investec. Even if liquidation takes place, there will be limited impact as JSW Steel's review petition has been accepted.

The Supreme Court overturned JSW Steel's Rs 19,700-crore resolution plan for Bhushan Power & Steel, Investec said in the report.

JSW Steel Ltd. and NMDC Ltd. are key beneficiaries of royalties and regulatory changes, Investec said. The Government of India placed 12% safeguard duty for 200 days. In case imports increase further, the brokerage is not ruling out the probability of safeguards being increased to 24%.

JSW Steel may benefit Rs 914 per ton which may translate to Rs 85 per share on the target price. For NMDC, the cost gains is of Rs 308 per tonn, translating to favourable target price impact of Rs 9 per share, Investec said.

Mills reported expansion in fourth quarter because of higher steel prices and lower coking coal prices. More of these factors will likely continue in the first quarter of financial year 2026, Investec said.

In the non-ferrous segment, Investec is factoring in a mixed-bag growth from here on. Vedanta Ltd. is offering multiple triggers. Pay-out, demerger, cost per volume tailwinds are some of these triggers.

Hindalco Industries is expected to see capital expenditure bump and no cost per volume tailwinds. On LME-Scrap spreads, the full impact of tariffs will likely be on Novelis. Hence, Vedanta appears to be well-placed, however, the brokerage suggested to keep an eye on evolving Guniea bauxite licenses per output and alumina pricing.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.